The Daily Dish

February 5, 2018

The Virtues of Productivity Growth

Eakinomics: The Virtues of Productivity Growth

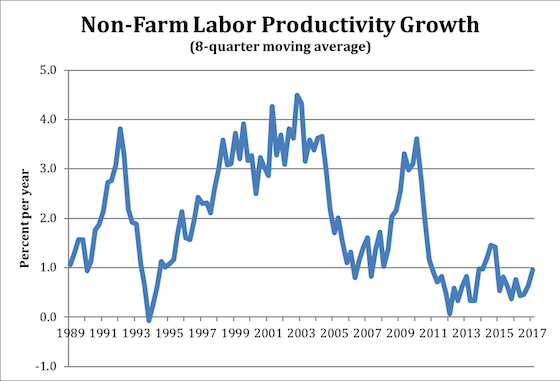

The chart displays the annualized growth rate of labor productivity in the non-farm business sector (measured as an 8-quarter moving average to focus on trends in the noisy quarter-to-quarter changes). Two eras stand out in the recent economic history: the sustained high rates of productivity growth in the late 1990s and early 2000s, and the depressed rate of growth since the recovery from the Great Recession began in 2009.

Poor productivity growth is at the core of the bond market’s reaction to Friday’s employment report. When the job report showed average hourly earnings growing at a year-over-year rate of 2.9 percent, yields on 10-year Treasuries jumped immediately and sharply. Why? Traders equated rising wages with rising cost that would have to be passed along in the form of higher prices. The bond market immediately demands a higher (nominal) return to compensate for the anticipated loss in purchasing power. Further, an uptick in inflation would likely spur the Federal Reserve to raise rates a larger amount, or more quickly, or both.

But suppose that productivity was also rising 2.9 percent per year. Then the increase in wages would be spread across a greater number of units; indeed, the unit wage cost would remain unchanged. Wages could rise without a threat of inflation. For workers, this means the wage increase is a higher standard of living – good for them. For bond traders, the wage increase is not a threat of higher inflation.

The benefits of more rapid productivity growth cannot be overstated. It is these benefits that are the spur controlling regulatory costs, reforms to business taxation, and other elements of a pro-growth agenda. The litmus test for 2018 and beyond is whether or not the new policy approach generates sustained higher productivity growth.

Fact of the Day

The highlight of the January jobs report was a 9 cent, or 2.9 percent year over year, increase in average hourly earnings.