Insight

October 22, 2018

Federal Disaster Relief and the Federal Budget

Executive Summary

- The Budget Control Act imposes a restriction on regular funding for disaster relief through a three-part formula that was established in 2018; the limit for funding in fiscal year 2019 is just under $15 billion.

- In practice, Congress and the president typically exempt disaster relief spending from budgetary restrictions after major disasters.

- Since 2012, combined regular and emergency disaster relief funding has totaled just under $195 billion – substantially more than $15 billion a year.

Introduction

The past two years have seen extraordinary need for emergency disaster assistance and related expenditures by the federal government, while Hurricane Michael will likely require tens of billions in new disaster relief in the next year. Disasters are by nature unpredictable, but sound budgetary practice requires attempting to estimate costs for potential contingencies such as storms. The Budget Control Act (BCA) has such a mechanism for attempting to budget for natural disasters—an adjustable cap based on past experience.

In practice, this mechanism is a largely pointless constraint, as Congress typically exempts any disaster spending above this cap from budgetary restrictions. This Insight presents the budgetary treatment of disaster relief and recent historical trends in federal disaster spending.

Budgeting for Disasters

In general, disaster relief is classified as discretionary spending, which is to say Congress funds it when needed through an appropriations act. Under current law, the BCA imposes a cap on annual discretionary spending but provides for certain exceptions to the caps known as cap adjustments, including one for disaster relief. Such an exception makes sense, as disasters and their costs are by definition unpredictable, and imposing a rigid cap on such spending would be nonsensical.

The BCA doesn’t fully exempt disaster aid from budgetary strictures, however; through the Consolidated Appropriations Act of 2018, Congress amended the BCA to include a new formula for determining how much disaster spending can be accommodated under the adjustable spending cap.[1] The cap adjustment, or funding ceiling, for disaster relief is the sum of three separate calculations:

- The 10-year average of previously enacted disaster appropriations, excluding the highest and lowest value.

- 5 percent of the total funding provided on an emergency basis for Stafford Act disasters.[2]

- The cumulative carryover of unused cap adjustment since FY2018.

It is important to note that calculations 2 and 3 are retroactive, meaning that even though Congress appropriated up to (and beyond through emergency designations) the cap adjustment for FY2018, the applicable 5 percent of past emergency funding calculation is applied retroactively for FY2018 and carried forward and added to the total cap adjustment for FY2019.

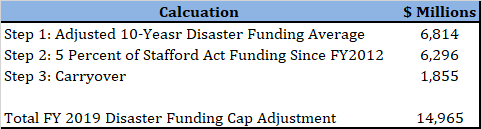

In August, the Office of Management and Budget (OMB) released the cap adjustment estimate for FY2019 pursuant to the new formula. Following the steps, OMB first examined the previous 10 years of regular discretionary disaster spending and found the average, exclusive of the highest and lowest values (see Table 2 below). Excluding the highest ($11.8 billion) and lowest ($2.4 billion), yields an average of $6.8 as the first step in the calculation. Second, OMB determined the value of 5 percent of all emergency Stafford Act spending since 2012. Taking 5 percent of this value gives $6.3 billion as the second step in the calculation. Third, OMB determined whether the carryover from previous years applied; in this instance, the carryover was essentially a determination of what the 5 percent of Stafford Act spending calculation (calculation 2) would have been in FY2018 (see Table 3 below). Stafford Act funding from 2012-2017 totaled $37.101 billion. 5 percent of that figure is $1.855 billion. This amount was essentially retroactively applied to the disaster cap for FY2018 and carried forward.

Table 1: Formula for FY2019 Disaster Funding Cap Adjustment

The sum of these calculations serves as the cap adjustment allowed for disaster funding under the BCA, which is $14.965 billion for FY2019. As noted above, however, this total will likely be insufficient to fund relief efforts for Hurricane Michael and other ongoing needs. Accordingly, Congress can and almost certainly will enact a much larger appropriation above this cap with an emergency designation, which bypasses any restrictions imposed by federal budget laws.

Recent Trends in Disaster Spending

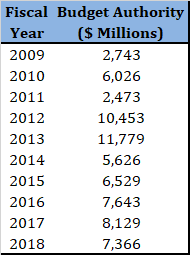

According to OMB, over the period FY2009-2018, regular (non-emergency) appropriations for disasters totaled $68.8 billion.[3]

Table 2: Regular Disaster Funding FY2009-2018

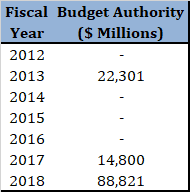

Since 2012, total emergency disaster funding under the Stafford Act has amounted to $125.9 billion.

Table 3: Emergency Stafford Act Disaster Funding FY2012-2018

Combined regular and emergency disaster spending has therefore totaled $194.7 billion since 2012. Congress has already appropriated $1.68 billion in new emergency-designated spending for FY2019, and as noted above, there will likely be tens of billions to follow.[4]

Conclusion

The Budget Control Act imposes a restriction on regular funding for disaster relief through an evolving formula. The current iteration of that formula, a three-part calculation that was established in 2018, would impose a $14.965 billion cap on disaster relief funding in FY2019. In practice, Congress and the president typically exempt disaster relief spending from budgetary restrictions after major disasters, so emergency spending in the coming fiscal year could be significantly higher.

[1] https://www.whitehouse.gov/wp-content/uploads/2018/04/Report_on_Disaster_Relief_Funding_2018.pdf

[2] The Stafford Act provides the statutory authority for most Federal disaster response activities. Emergency funding for these disasters is exempt from any restrictions under the Budget Control Act.

[3] https://www.whitehouse.gov/wp-content/uploads/2018/08/Sequestration_Update_August_2018_House.pdf

[4] https://www.whitehouse.gov/wp-content/uploads/2018/10/Ryan_7-Day_After_Report_10-18-18.pdf