Testimony

March 1, 2022

Testimony on Competition and the Small Business Landscape: Fair Competition and a Level Playing Field

United States House of Representatives Committee on Small Business

* The views expressed here are my own and not those of the American Action Forum. I thank my colleagues Dan Bosch and Thomas Wade for their insights and assistance.

Chairwoman Velázquez, Ranking Member Luetkemeyer, and members of the Committee, thank you for convening this hearing and providing me with the opportunity to appear today and share my views on the regulatory burdens, financial barriers to entry, and macroeconomic headwinds impacting small businesses.

In my testimony I wish to make three main points:

- The recent focus on market concentration and large, publicly traded companies obscures the important fact that small businesses are the lifeblood of the economy and essential to continued recovery from the COVID-19 recession;

- Policies that support the ability of new firms to start-up, enter markets, and innovate are the most reliable route to fair and effective competition across the economy; and

- Firms benefit from a macroeconomic environment characterized by price stability and full employment, in contrast to the damaging inflation and impaired labor markets currently facing small businesses.

Let me consider these in turn.

Small Businesses and the U.S. Economy

The heated public commentary about increasing market concentration, online giants, and new approaches to antitrust policy threatens to convey a misleading portrait of the U.S. economy. The United States is home to 32.5 million small businesses representing 99.9 percent of all businesses. Over 60 million employees constitute 48.6 percent of the total private workforce, and small businesses created 1.6 million new jobs in 2019 – over 80 percent of job creation in that year.

Small businesses contribute across the entire economy (see table below) and most small businesses are in sectors of the economy that also contain larger competitors. This implies that it is very important that policies not tilt the playing field among firm sizes, allowing the competition to continue in a fair fashion.

Small Business and Competition

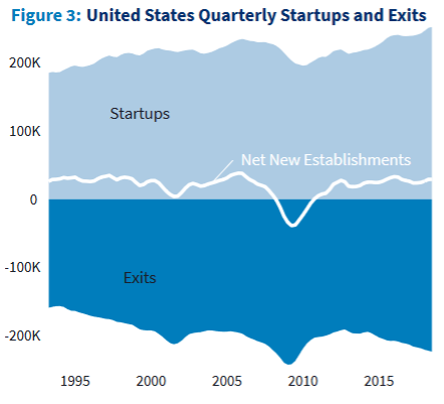

Looking at a single year, as in the table above, misses the dynamism brought to the economy by new businesses. In recent years, roughly 200,000 new businesses start up each year, and a slightly smaller number exit. This reflects competitive markets, and something that policymakers should preserve and enhance. For example, between 1985 and 2011, an average of 183 new banks were chartered annually. However, between 2012 and 2019 that number dropped to just four. This suggests that the policy environment in financial services is precluding sufficient entry to enhance competitive pressures.

Source: Small Business Administration

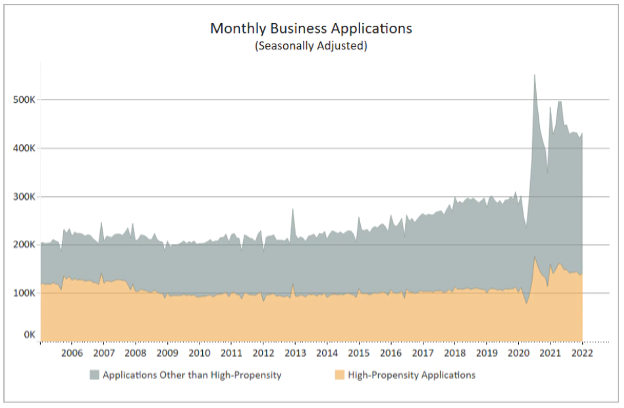

These dynamics are especially visible and important in the recovery from the pandemic recession. There has been an increase in the number of applications to start companies. 2021 saw 5.4 million applications, a 53 percent increase over 2019 pre-pandemic figures. A third of these applications are considered “high propensity,” or likely to themselves have payroll and create further jobs. Even though entrepreneurship is surging, 50 percent of these businesses will fail in the first five years.

Source: census.gov

Regulatory Burdens on Small Businesses

The disproportionate impact of regulatory burdens on existing small businesses, and their importance as a barrier to new entrants, has been well known for decades. This phenomenon is what prompted enactment of the Regulatory Flexibility Act (RFA) in 1980. While the RFA helped direct agencies’ attention to the problem, it has not solved it. A series of studies conducted for the Small Business Administration’s Office of Advocacy through 2010 consistently showed that small businesses bear a heavier burden from regulations than large businesses.[1] During the Obama Administration, when regulatory costs exceeded an average of $100 billion per year, the National Federation of Independent Business reported that “government regulation” was consistently a top-three answer in its Small Business Economic Trends survey when respondents were asked to identify their single biggest problem.

Early results from the current administration indicate that costly regulation will likely go beyond that of the Obama Administration. The American Action Forum has tracked the cost of final rules published in the Federal Register since 2005.[2] Last year was the second-costliest year on record, behind only 2012. And the costs in the first year of the administration, $201 billion, are the highest first-year total over that period.

These extraordinary regulatory costs will impose a disproportionate burden on small businesses, which often lack in-house compliance experts to handle mountains of paperwork and complicated technical requirements. In addition, overly burdensome regulations can erode the already small margins that many small companies operate on. Reducing these regulations can help improve the competitiveness of small businesses.

Congress should consider enacting regulatory reform legislation that requires agencies to better assess and take into consideration regulatory costs and benefits. Options include reforming the 76-year-old Administrative Procedure Act, which was not designed for some of today’s massively expensive rules; reforming the RFA to require agencies to consider clearly foreseeable indirect costs and get feedback on possible regulatory options from small entities before a rule is ever proposed; codifying a regulatory budget similar to the one that worked to limit regulatory costs during the Trump Administration; and requiring agencies to identify at the time they publish rules how they will measure the success of those rules.

Tilting the Playing Field

An example of tilting the market playing field is the America Creating Opportunities for Manufacturing, Pre-Eminence in Technology, and Economic Strength (America COMPETES) Act. (Similar legislation, the United States Innovation and Competition Act (USICA), was passed by the Senate.) The stated intent of the bill is to raise the United States’ domestic and global competitiveness, especially in relation to China. In doing so, however, the bill engages in industrial policy that would place a heavy federal hand in private industry. This raises two concerns. First, it introduces a bias toward current firms (with no provision for future entrants). Second, it interferes with competitive forces and could waste billions of taxpayer dollars.

The Macroeconomic Environment

Firms benefit from a macroeconomic environment of price stability and full employment. At present, this is hardly the situation. The January report on the Consumer Price Index (CPI) showed year-over-year inflation of 7.5 percent, up from 1.4 percent in January 2021. Even worse, the year-over-year composite inflation for food, energy, and shelter – over 50 percent of the typical family’s budget – is up from 1.4 to 8.1 percent.

The 6.1 percentage point 12-month jump in CPI inflation has been rivaled only twice in the postwar era: In 1951, it jumped as much as 10.6 percentage points and in 1974, it rose 6.1 percentage points. Both episodes are instructive.

The 1951 episode is a cautionary tale about overstimulating the economy. In this case, year-over-year growth in gross domestic product entered the year in double-digit territory, and Korean War-related defense production layered on year-over-year growth in government spending that peaked at 49 percent in the third quarter. The lesson is that excessive government spending in a hot economy can quickly fuel inflation.

In contrast, the 1974 episode demonstrates the exact opposite of demand stimulus. Instead, it features a huge supply cost shock – the quadrupling of oil prices due to the OPEC oil embargo. Lesson: Cost increases borne by supply problems can quickly be passed along to consumers, even if the economy is moving toward recession.

The inflation of 2021 reflects a combination of these forces. The COVID-19 pandemic has wreaked havoc on labor markets worldwide, and the resulting disruptions in supply chains and goods production have been well-documented. The tangled supply chains in the United States and elsewhere reduced the effective aggregate supply, an impact similar to the 1974 experience. Given “normal” demand conditions (for a pandemic, that is), this might produce some inflation. Indeed, this was essentially the administration’s argument for months: “We didn’t do it. It just happened.”

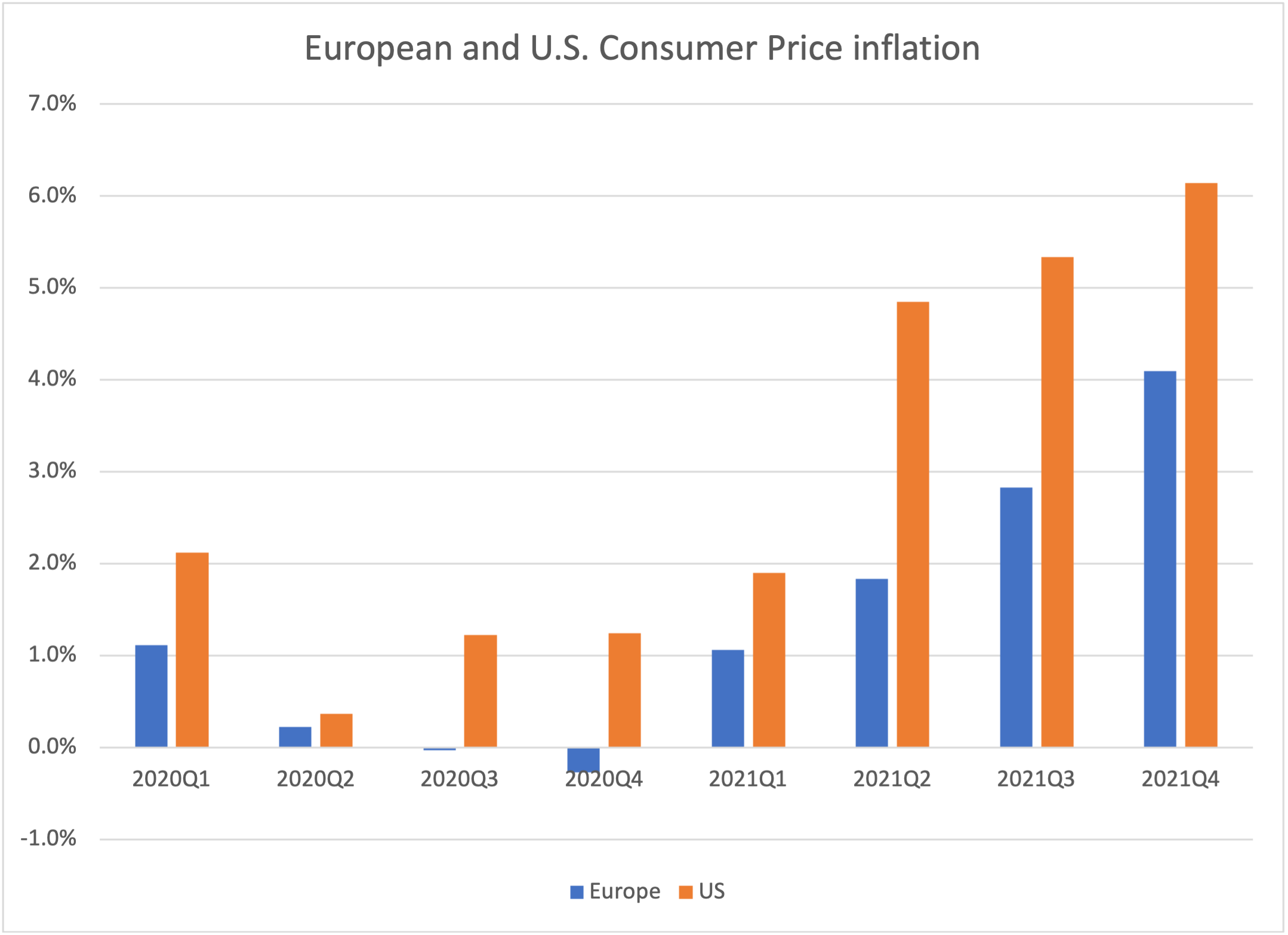

If that were true, then the pick-up in inflation would be the same across the globe. As shown in the chart below, consumer price inflation did pick up in Europe (and a similar chart exists for Asia, etc.). Inflation was about 1 percent in the 1st quarter of 2021, and then rose about one percentage point each quarter to close at 4 percent in the 4th quarter. (Data for only the first two months of the 4th quarter were available for this graph.) The United States looks very different, however, so something else must be going on. Rather than a smooth rise, inflation jumped from 1.9 percent in Q1 to 4.8 percent in Q2, before accelerating more smoothly and slowly the remainder of the year.

These supply constraints increased costs and generated higher inflation across the globe. European consumer price inflation, for example, increased about one percentage point each quarter and ended 2021 at 4 percent. Part of the U.S. experience is driven by supply chain issues, as well.

But there are also elements of the 1951 episode. Fiscal policy added fuel to the fire in the form of the $1.9 trillion, deficit-financed American Rescue Plan (ARP) stimulus in March 2021. At the time of its signing, the U.S. economy was growing at a red-hot 6.5 percent; additional stimulus was neither needed nor desirable. Inflation responded immediately to the policy error, jumping from 1.9 percent in the first quarter to 4.8 percent in the second quarter – nearly three times the increase of Europe’s supply-driven inflation. The fiscal stimulus was reinforced by an aggressively accommodative monetary policy that featured zero-percent interest rates and large, continuous monetary infusions. Inflation continued to rise as the year went on.

What should policymakers do?

To diagnose the roots of this inflation is to identify the appropriate policy response. Ultimately, the supply chain issues boil down to the impact of the coronavirus. This is best offset with a more effective public health policy. Both administrations have botched the response to COVID-19 with reliance on vaccines as a silver bullet. It is not surprising that, as The New York Times reported, six former Biden transition advisers called on the president “to adopt an entirely new domestic pandemic strategy geared to the ‘new normal’ of living with the virus indefinitely, not to wiping it out.”

Such a strategy would be composed of a greater range of responses to the pandemic, with more emphasis on testing and therapeutics, and less on mandates for lockdowns, vaccines, and masks.

There are, of course, traditional tools of economic policy available to slow the excess stimulus that is contributing to inflation. It is highly unlikely, however, that policymakers will soon embark on structural deficit reduction via higher taxes and lower spending. Perhaps the best we can hope from policymakers is that they stop adding to the problem with massive new spending bills such as the Build Back Better Act.

Most of the focus is thus on the Federal Reserve, which must take its foot off the monetary accelerator and begin tapping the brakes with higher interest rates and withdrawals of the massive monetary infusion undertaken during the pandemic. If it taps too lightly, inflation will persist and become more entrenched. If it becomes too aggressive—as has habitually been the case in its postwar response to sharp rises in inflation—growth will stall, and a recession could ensue.

Thank you. I look forward to your questions.

[1] Crain, Nicole V. and Crain, W. Mark. The Impact of Regulatory Costs on Small Firms. Conducted for the SBA Office of Advocacy. Release Date: September 2010.

[2] Regulatory Rodeo. www.regrodeo.com.