Week in Regulation

April 12, 2021

The Lull Continues

Similar to the couple of weeks before it, last week was a fairly quiet one in terms of rulemaking activity. There were only nine actions with some quantifiable economic impact. The highest cost estimate among those was roughly $7 million. Across all rulemakings, agencies published $10.8 million in total net costs and added 668 annual paperwork burden hours.

REGULATORY TOPLINES

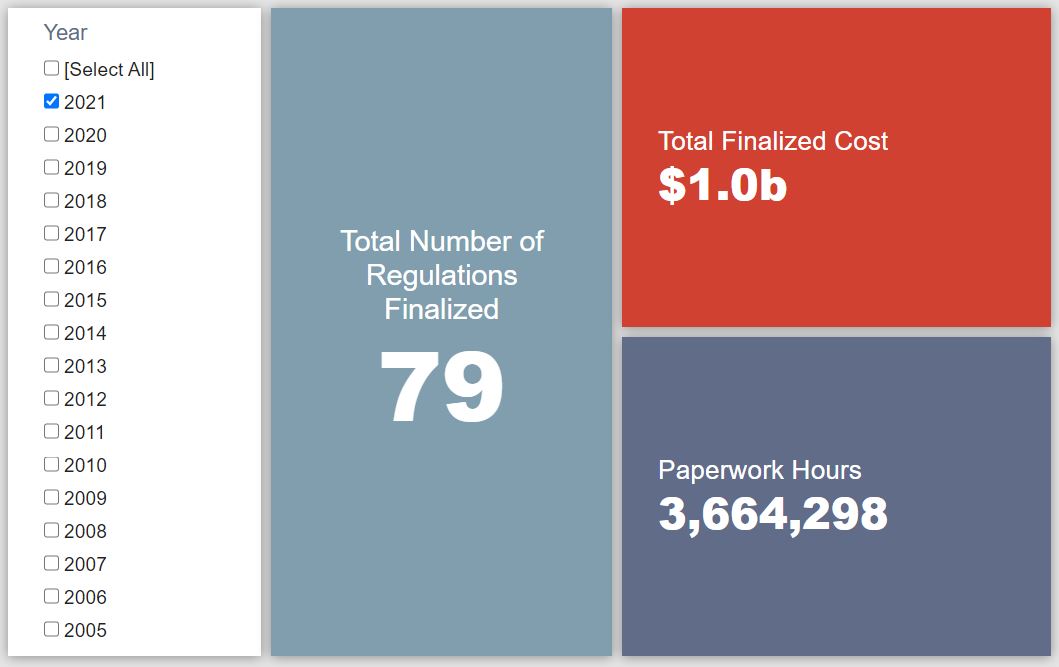

- Proposed Rules: 38

- Final Rules: 68

- 2021 Total Pages: 18,849

- 2021 Final Rule Costs: $1 Billion

- 2021 Proposed Rule Costs: -$8.3 billion

NOTABLE REGULATORY ACTIONS

As noted above, there were no especially significant rulemakings last week. For the second consecutive week, an airworthiness directive (with $7.3 million in costs) led the way. Perhaps the most consequential regulatory news of the week was President Biden’s announcement of forthcoming administrative actions to address gun violence. Actual rulemakings implementing these policies will presumably come within the next couple of months, and they will likely be among the most politically contentious regulatory actions of the current administration thus far.

CONGRESSIONAL REVIEW ACT UPDATE

On March 23, the first joint resolution of disapproval under the Congressional Review Act (CRA) of this term was introduced. CRA resolutions essentially seek to wholly rescind specific final rules within a set timeframe. The significance of these resolutions is discussed further here. In the interest of providing a public accounting of the potential economic impact of these actions should they pass, the American Action Forum (AAF) will provide a weekly update of the rules being targeted and any measurable economic effects included in their original analyses.

| Agency | Rule | House Res? | Senate Res? | Original Costs/Savings ($ Million) |

| EEOC | Update of Commission’s Conciliation Procedures | X | X | |

| EPA | Oil and Natural Gas Sector: Emission Standards for New, Reconstructed, and Modified Sources Review | X | X | -31

|

| OCC | National Banks and Federal Savings Associations as Lenders | X | X | |

| SEC | Procedural Requirements and Resubmission Thresholds Under Exchange Act Rule 14a-8 | X | X | -10.5 |

| HHS | Securing Updated and Necessary Statutory Evaluations Timely | X | 104.5 | |

| SSA | Hearings Held by Administrative Appeals Judges of the Appeals Council | X |

TRACKING THE ADMINISTRATIONS

As we have already seen from executive orders and memos, the Biden Administration will surely provide plenty of contrasts with the Trump Administration on the regulatory front. And while there is a general expectation that the new administration will seek to broadly restore Obama-esque regulatory actions, there will also be areas where it charts its own course. Since the AAF RegRodeo data extend back to 2005, it is possible to provide weekly updates on how the top-level trends of President Biden’s regulatory record track with those of his two most recent predecessors. The following table provides the cumulative totals of final rules containing some quantified economic impact from each administration through this point in their respective terms.

![]()

This continued stagnation, at least in terms of estimated economic impact, under the Biden Administration is beginning to contrast more and more with the trends seen during either the Trump or Obama administrations. During a similar period under Trump, one of his administration’s first real deregulatory actions (a rule putting the brakes on an Obama-era fiduciary standards rule) hit the books. At the start of April in Obama’s first term, costs began to rise notably due to rules such as these updated energy efficiency standards. One can expect that, given his prodigious issuance of executive orders and memoranda, President Biden’s regulatory record will pick up steam soon, but thus far it has lagged behind recent historical trends.

THIS WEEK’S REGULATORY PICTURE

This week, the Consumer Financial Protection Bureau (CFPB) reverses course on a number of Trump-era policies.

On April 6, the CFPB published seven notices in the Federal Register that changed policies put in place by the Trump Administration to lessen compliance burden stemming from COVID-19 and its effect on the economy.

In general, the CFPB under the Trump Administration adopted policy statements that gave the agency discretion on enforcement if the agency found compliance violations that were likely to have been caused or exacerbated by COVID-19. The statements recognized that staffing and resource issues were likely to occur for companies and institutions during the pandemic.

The policies covered a broad spectrum of enforcement areas, including rules regarding CFPB’s supervisory activities, credit card collections and disclosures, mortgage disclosures, and credit reporting.

In the notices rescinding the Trump-era policies, the CFPB said it believes that the conditions that existed as the pandemic took hold have changed. Specifically, the agency says that affected companies have begun resuming some in-person operations and/or have had time to adapt their operations. As a result, enforcement leniency is no longer necessary.

The recissions represent the most notable reimposition of regulatory requirements that were eased during the pandemic. They represent seven of the 10 actions in AAF’s COVID-19 Regulation Tracker that have reimposed rules or policies.

As more Americans get vaccinated and the economy continues to slowly re-open, the number of actions reimposing rules are likely to climb in the coming months.

TOTAL BURDENS

Since January 1, the federal government has published $7.3 billion in total net cost savings (with $1 billion in new costs from finalized rules) and 7.3 million hours of net annual paperwork burden reductions (with 3.7 million hours in increases from final rules).