The Daily Dish

January 30, 2023

A Cautionary Note on Inflation

Friday brought the latest read on inflation, with the Bureau of Economic Analysis (BEA) releasing the December report on the price index for personal consumption expenditures (PCE) – the Federal Reserve’s preferred measure of inflation. The topline was seemingly very good, with inflation clocking in at 5.0 percent year-over-year. This is down from 7.0 percent six months ago.

Most of the coverage was celebratory. The New York Times weighed in: “The Federal Reserve’s preferred inflation index climbed 5 percent in the year through December, a notable slowdown from November and a continuation of a six-month downward trend.

After stripping out food and fuel, the price index climbed 4.4 percent compared with a year earlier, in line with what economists in a Bloomberg survey had expected and a slowdown from 4.7 percent in November. The overall picture is one of moderating inflation — providing some long-awaited relief for consumers — but which remains unusually rapid at more than twice the 2 percent rate the Fed aims for on average over time.”

Progress, certainly. But a closer look reveals a slightly more daunting picture. First, the bulk of the recent volatility in inflation has been due to a sharp uptick in food prices (the poster child being eggs) and the large downdraft from energy prices. It makes sense to focus on core (non-food, non-energy) inflation.

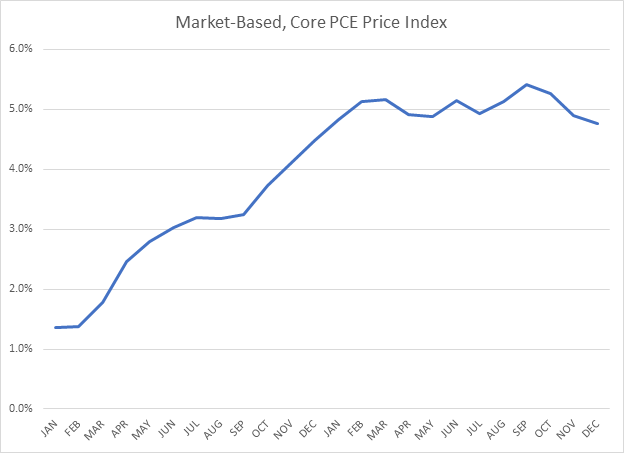

But there is one more adjustment that makes sense at the moment. In some cases, the BEA does not have a direct measure of prices and instead has to impute the price data. The best example of this is the price of owner-occupied housing each month. The ideal measure is what the owner would charge herself to rent the house for the month, but there is no such transaction. The BEA estimates and imputes this price.

To get a cleaner look at price pressures, one can focus on “market-based PCE,” a price index composed solely of prices for actual transactions. Inflation measured by this price index is graphed below. Beginning in January 2021, inflation ramped up steadily even as the Fed began its interest rate hikes. It has plateaued since the spring of 2022, peaked at 5.4 percent, and has fallen only to 4.8 percent in December.

There are other indicators that the excessive demand stimulus and inflation pressures are ebbing. But the graph is a reminder that inflation is stubborn and returning to the 2 percent target is far from a done deal.

Fact of the Day

The Department of Agriculture estimates its rule regarding “National Organic Program; Strengthening Organic Enforcement” would add roughly $216 million in new compliance costs.