The Daily Dish

August 28, 2023

About That Recession

Friday Federal Reserve Chairman Jerome Powell delivered a firm “stay the course” message in his speech at Jackson Hole. He emphasized that the Fed is committed to a 2 percent target for inflation and that core inflation is still running at more than twice that level. Hence, he emphasized the continued need for slower demand growth: “Turning to the outlook, although further unwinding of pandemic-related distortions should continue to put some downward pressure on inflation, restrictive monetary policy will likely play an increasingly important role. Getting inflation sustainably back down to 2 percent is expected to require a period of below-trend economic growth as well as some softening in labor market conditions.” (Emphasis added.)

That raises the prospect of further tightening of monetary policy to achieve this slower growth, a prospect that dismays some. They look at the 2nd quarter growth of gross domestic product (GDP) at 2.4 percent and inflation that has declined substantially and conclude that nothing needs to change.

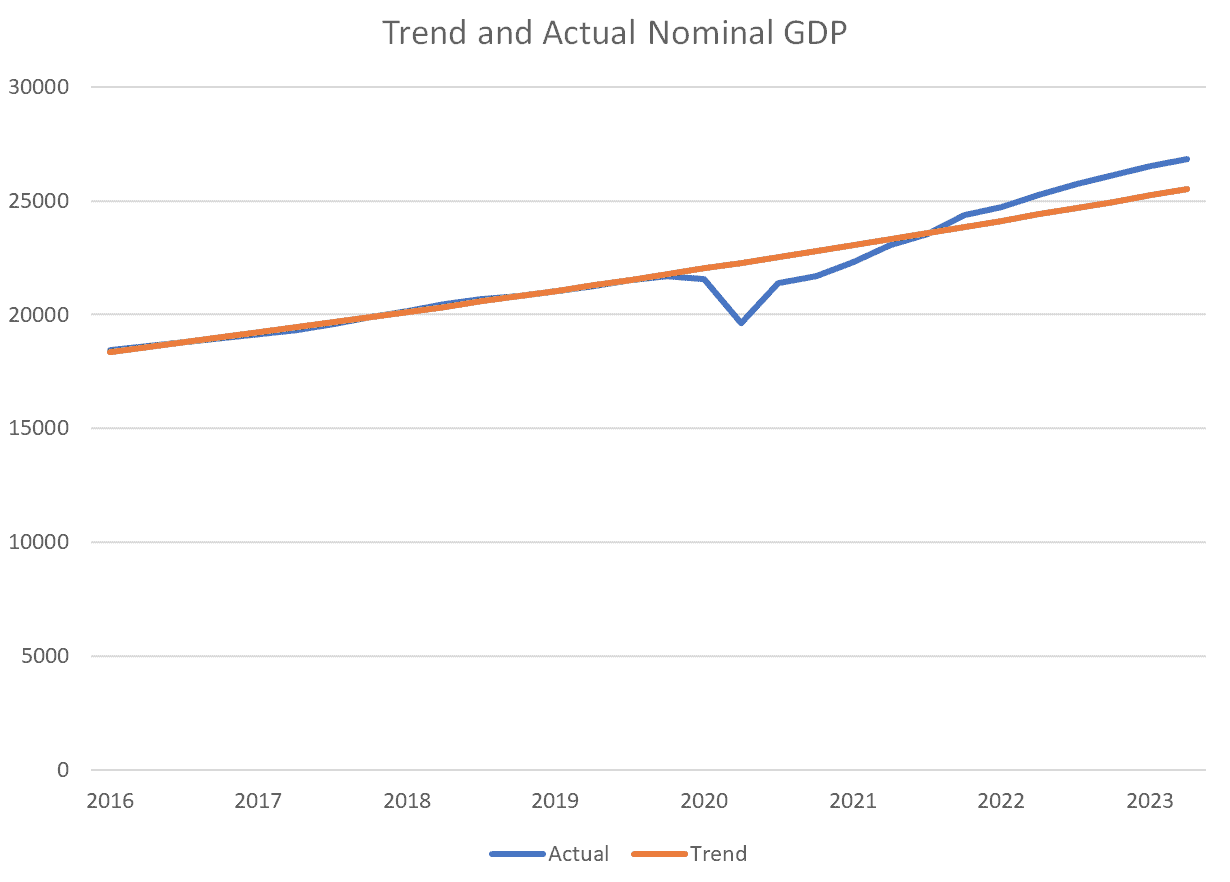

The problem with this argument is shown below. The chart shows actual nominal GDP since 2016 and a measure of trend growth that is created by estimating the trend from 2016 through the final quarter of 2019 (prior to the pandemic downturn). That trend is then extended to the present.

What does it tell us? It shows that the level of demand remains substantially above trend, which is the source of sustained inflation pressure. It also reveals the need for slower growth in demand to get the level back down to trend and eliminate the inflation pressure.

That is the Fed’s game plan.

The only real issue is whether this takes the form of a slower growth rate of demand to slowly close the gap with trend – a soft landing – or a more rapid decline that includes negative growth for a short period – a recession. The jury is still out.

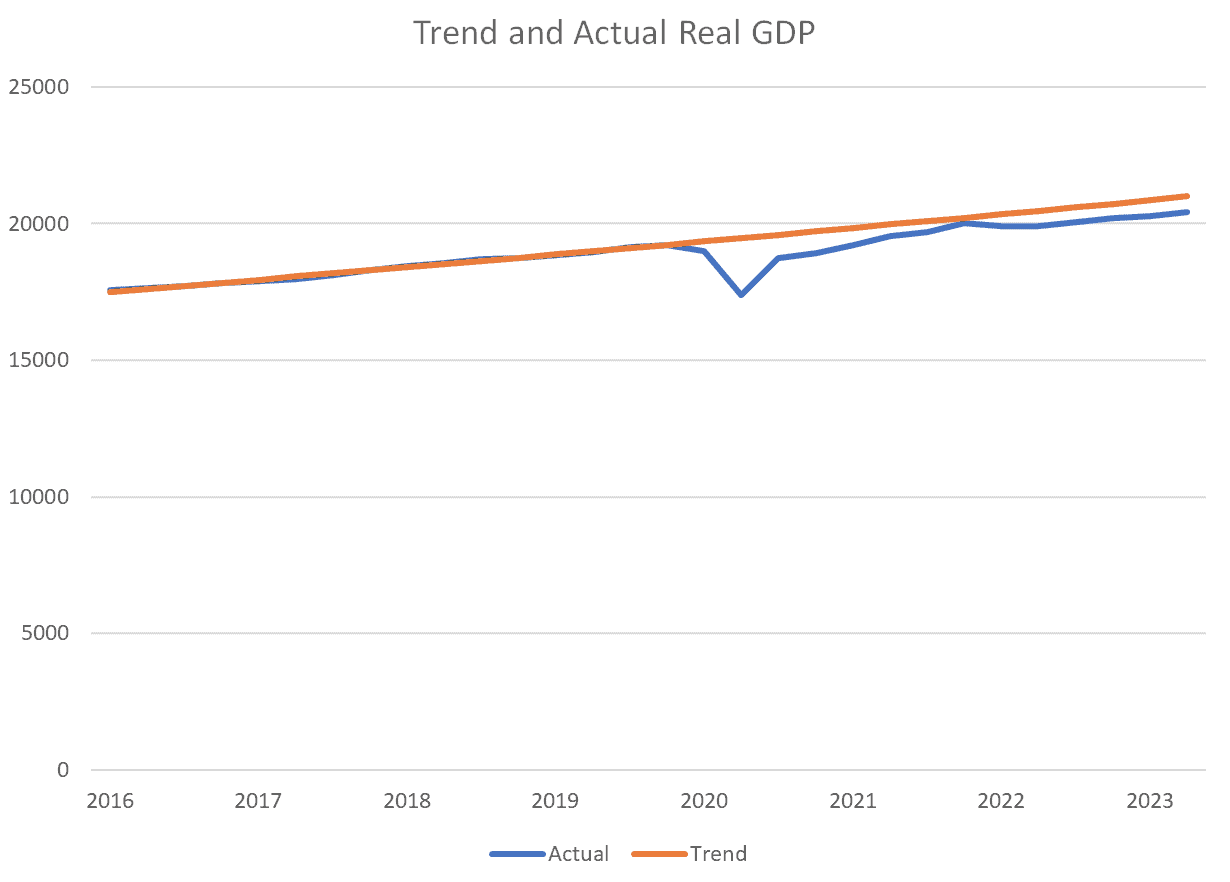

For completeness, it is useful to repeat the exercise for real GDP. This is shown below. Here the lesson matches experience as well. GDP has not quite recovered its pre-pandemic potential – some supply issues remain. If growth takes the form of greater supply, it will provide growth without inflation pressure.

Powell’s message on Friday was similar to his speech last year. The final lesson of these simple charts is that there is a good reason for this: The current situation looks a lot like the one the Fed faced last year.

Fact of the Day

According to the Congressional Budget Office, debt held by the public will reach 181 percent of gross domestic product in 2053.