The Daily Dish

April 15, 2026

Productivity and Politics

Productivity is normally the dry and esoteric stuff of academic debates. But at present, productivity lies at the root of some of the most contentious political debates. If one reads the newly released Economic Report of the President, one will find that the administration is expecting real gross domestic product (GDP) to grow at an average rate of 3 percent over the next 10 years. GDP growth is the sum of growth in workers and growth in output per worker, or productivity. The administration is anticipating annual productivity growth of 2.9 percent and essentially no growth in the labor force. These are the assumptions underlying the President’s Budget.

At the other end of Pennsylvania Avenue, the Congressional Budget Office (CBO) has GDP growth leveling out at 1.8 percent, with the next two years a bit above that. Of the 1.8 percent, 1.4 percent is labor productivity growth. That is a very different picture of the level and composition of GDP growth than the White House.

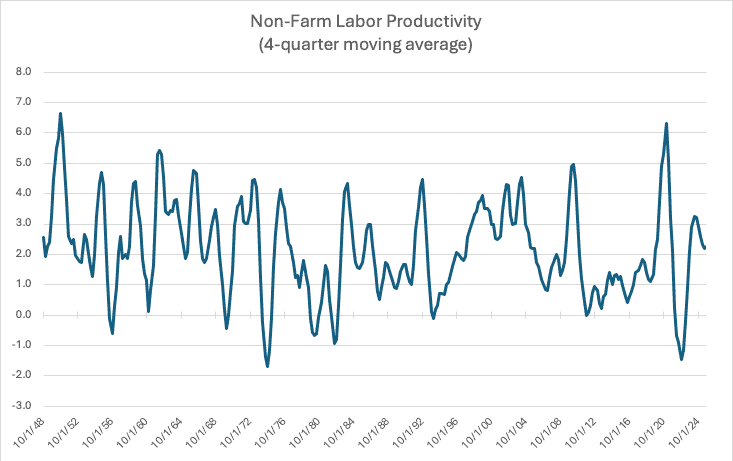

For perspective, graphed below is the postwar history of non-farm labor productivity growth, measured as a 4-quarter moving average of year-over-year productivity growth. Obviously, productivity growth is quite noisy. It has averaged 2.2 percent since 1948 – roughly the rate today – and reached a maximum of 7.2 percent. Note that the longest streak of productivity growth at 3 percent or better is only 12 months. CBO is assuming that productivity will revert to historical norms, or a bit less. The administration is betting on a future that is very different than the past.

Indeed, if one listens to the commentary of National Economic Council Director Kevin Hassett at the one-minute mark of this clip from CNBC yesterday, he describes the economy as being in a productivity “boom” that is putting downward pressure on prices in 2026. In this view, a boom in productivity is giving the Federal Reserve a hand in overcoming inflation driven by tariffs, the impact of global oil price hikes, and the other sources of sticky inflation. And the administration expects it to continue for 10 years. Readers can examine the chart and decide for themselves.

There is one last nuance worth highlighting. One can think of labor productivity going up because the laborer was given a measurable addition to his or her tools – a shovel, backhoe, calculator, computer, etc. Giving workers more or better capital to work with is known as capital deepening. Alternatively, there may be improvements – think a better business model (big box retail or artificial intelligence) that makes everything more productive. This is known as – economists are not legendary for the creativity – total factor productivity (TFP).

CBO puts the growth rate of TFP at 1.1 percent, so it is a big part of the productivity story. The administration does not put any numbers on TFP growth, but it is clearly all-in on AI and highlights its anticipated contributions to TFP growth.

This debate will not be settled for years. But there is no more important issue to track.

Fact of the Day

As of April 8, the Fed’s assets stood at $6.7 trillion, up more than $18 billion from the prior week but down $33 billion from a year ago.