The Daily Dish

June 23, 2026

Productivity and the Fed

Fed watchers will be focused this week on Thursday’s release of the May personal consumption expenditures measure of inflation. A hot inflation number – it was 3.8 percent in April – will highlight the disconnect between the new chairman’s desire for rate cuts and the inflation environment in the aftermath of the decision to attack Iran.

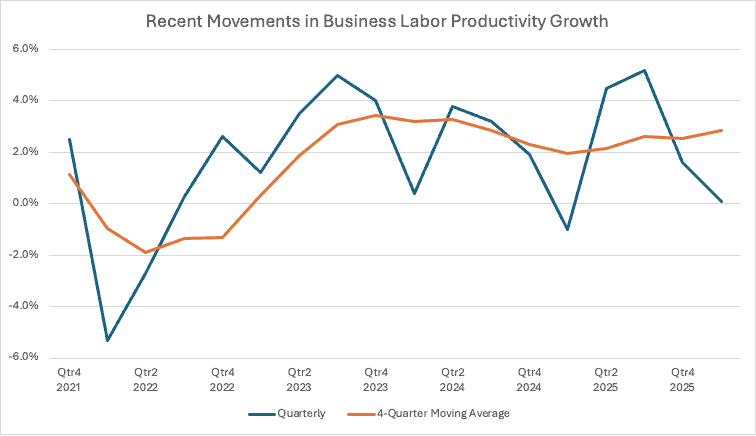

In the past, Chairman Warsh has pointed to the potential for productivity growth to ease inflation pressures and augment supply-driven growth, thereby permitting lower rates that allow demand to keep pace with supply. This argument was especially potent in the aftermath of the labor productivity data for the 2nd and 3rd quarters of 2025, which came in at 4.5 percent and 5.2 percent (annual rates), respectively (see the blue line in the chart below). Unfortunately, productivity data are notoriously volatile and the growth rate plunged back to nearly zero over the next two quarters.

To get a cleaner view of the trends, consider the orange line in the chart, which shows a four-quarter moving average of productivity growth. This suggests productivity growth in the range of 2.5–3.0. This is solid, but slightly down from earlier years and does not suggest a sea change that would permit a dramatic shift in the policy stance.

Labor productivity growth is important because, mechanically, it permits wages to rise without a 1-for-1 rise in unit labor costs. This reduces the upward pressure on prices stemming from the labor market. Recently, however, there has been very little connection between the labor market and inflation. Instead, there has been a broad array of input prices (including tariffs) feeding consumer inflation. In these circumstances, it makes sense to look at a broader measure of productivity.

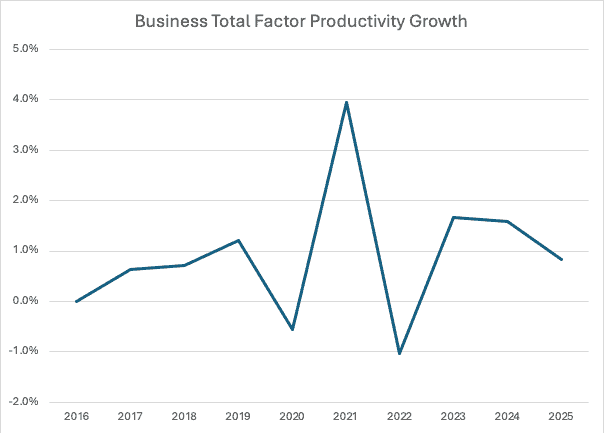

Graphed below is the Bureau of Labor Statistics estimate of productivity growth of all factors of production (cleverly named total factor productivity), available only on an annual basis. What jumps out in the chart are the pandemic-related moves. Outside of that interval, there is nothing to suggest that productivity has moved up in a significant fashion.

As the AI revolution evolves, it may be the case that the current investment in AI infrastructure generates greater supply and productivity. At present, however, it looks much more like a demand-side investment boom without a matching supply component. None of that translates into a need for lower rates.

Fact of the Day

Across all rulemakings last week, federal agencies published roughly $362.9 million in total cost savings and cut 43,222 paperwork burden hours.