The Daily Dish

January 5, 2023

The Fed’s Labor Market Challenge

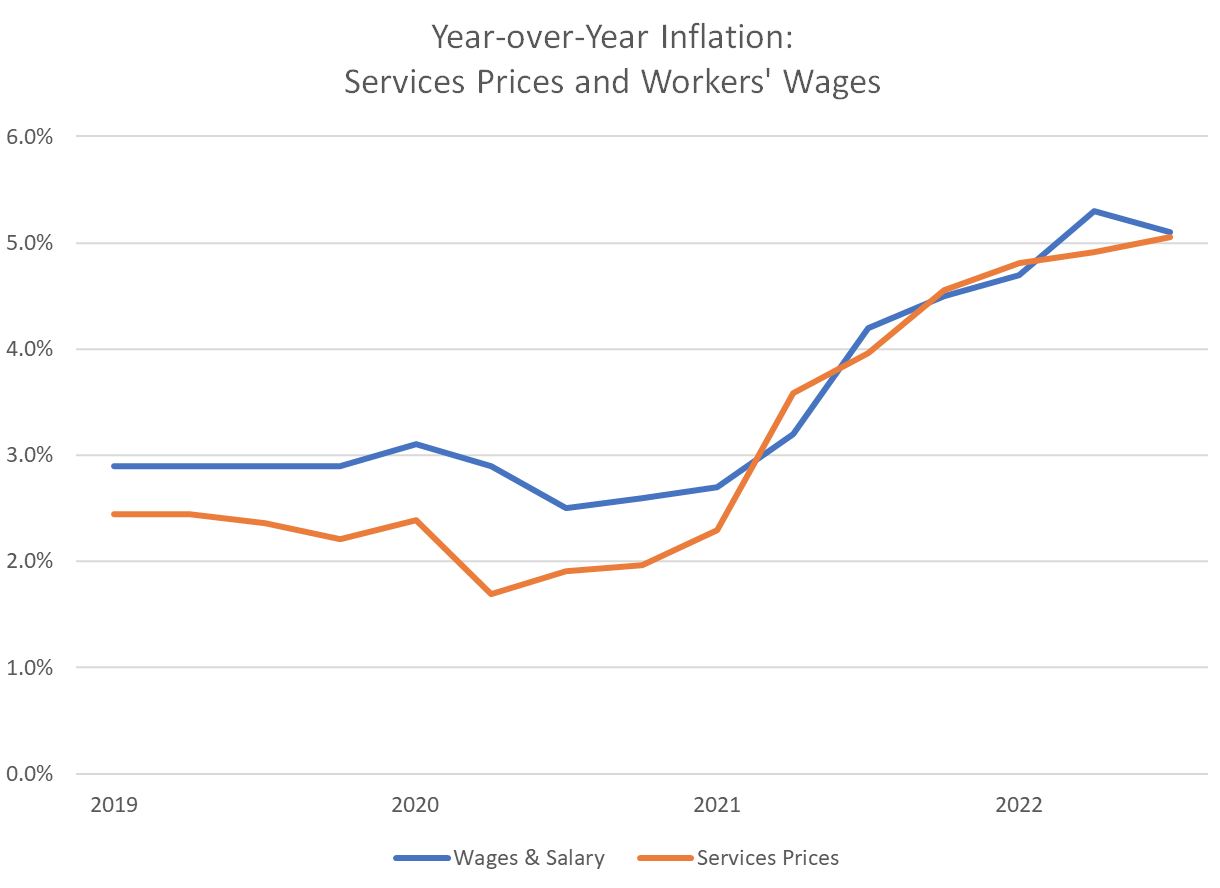

Inflation remains the pre-eminent macroeconomic challenge. While the Federal Reserve has had some modest success in bringing down expectations (see the New York Federal Reserve survey data here) to under 6 percent over the next year, and has seen some modest declines in the pace of goods-price inflation, there has been essentially no progress in reducing inflation in the prices of services (see the orange line in the chart below).

Indeed, services inflation is the story of 2022 and it is intimately tied to labor market performance. As Fed Chair Jerome Powell has repeatedly stressed, the most important cost for service providers is labor, so wage inflation (or, more broadly, compensation inflation that includes benefits) is a central feature of the Fed’s attempts to bring down inflation.

The blue line in the graph is inflation in (cash) wages and salary – using total compensation yields a similar picture – taken from the Department of Labor’s employment cost index data. It is a mirror of the services inflation trajectory.

(These data are adjusted for the mix of employees and, thus, are a cleaner measure than the monthly data on average hourly earnings provided in the employment report.)

This is the reason for such a tight focus on the monthly reports on jobs and the labor market; only if wage inflation cools will there be success with services and overall inflation. To date, there has been precious little success on this front, a fact one was reminded of by the release of the Job Openings and Labor Turnover Survey (JOLTS) for November yesterday.

In the dry language of government statisticians, the bottom line was that: “The number of job openings was little changed at 10.5 million on the last business day of November, the U.S. Bureau of Labor Statistics reported today. Over the month, the number of hires and total separations changed little at 6.1 million and 5.9 million, respectively. Within separations, quits (4.2 million) and layoffs and discharges (1.4 million) changed little.”

Despite all the fuss over the pace of Fed rate hikes, the size of Fed rate hikes, and the promise of more Fed rate hikes, the inflation outlook and labor market have “changed little.” (As an aside, the fiscal side has done little to help, as expected. The recent omnibus spending bill raised defense spending by 10 percent, non-defense spending by 6 percent, and the Social Security cost-of-living adjustment raised benefits by 8.7 percent, so the fiscal inflation stimulus continues.) The outstanding question: What will it ultimately take?

Fact of the Day

Federal agencies collectively finalized $117.1 billion in net regulatory costs in 2022, making it the fifth-most expensive year since 2005.