Research

August 29, 2017

Fixing Tax Incentives is Key to Bolstering Clean Energy Growth

Summary

- Tax credits for energy will cost the U.S. taxpayers around $130 billion over a ten-year period.

- Since only existing energy sources are eligible to claim tax credits, the current tax code favors incumbents and discourages innovation.

- With tax reform and an infrastructure bill on the horizon, the time is right to move to a technology-neutral and revenue-neutral tax treatment of energy, encouraging clean energy growth, innovation, and valuing consumer preference.

Introduction

As both the administration and Congress have stated that moving an infrastructure package is a priority, so energy policy decisions will likely come to the fore. This may present a rare opportunity to reform the ill-designed energy policies that were conceived to address the concerns of the 1970s. Thus far, the federal government’s approach to energy policy has consisted largely of subsidizing a menu of sources via tax credits. But such policy creates significant distortions in energy markets, favoring incumbents over innovation. It would be prudent for policymakers to pursue a technology neutral approach to energy subsidies, and do so in a way that promotes competition. This can be achieved by replacing cost-recovery subsidies with full-expensing, and replacing other energy-specific subsidies with tax treatment that focuses on pollution abatement.

Current Design of Energy Subsidies

Currently, the U.S. Treasury projects $94 billion in energy-related tax expenditure subsidies (tax credits or tax refunds, rather than direct subsidies or funding) from 2017-26. An alternative projection from the Joint Committee on Taxation (JCT) estimates $74.1 billion over a mere five years. Both estimates are likely below the subsidy levels that will be realized, since they gauge “tax form behavior,” meaning they gauge the cost only by the current projected demand for the subsidies, not the increase in demand that would occur from introducing the subsidy (the Treasury Department explains that estimating market reactions to the tax breaks would be overly complex and not necessarily accurate).

The purpose of tax subsidies is to change taxpayers’ behavior for myriad economic, political, and other purposes. In the energy sphere, the ideology of preferential tax treatment for domestic energy production is rooted in the oil crises of the 1970s, when foreign energy suppliers embargoed the United States to induce policy change. Since that time, energy security has been a driver of subsidies designed to bolster domestic energy production, mostly from fossil fuels. After the attacks of September 11th, 2001, the concern that U.S. oil purchases were funding terrorism further entrenched such policies.

The Obama Administration expanded upon existing energy subsidies as part of its stimulus plan, allocating roughly $90 billion towards clean energy, mostly for renewables. The intent of the package was to stimulate growth by reducing externalities (when the cost of pollution is borne outside of the sale price), and by reducing innovation spill-over concerns (that investing in innovation may be discouraged because competitors can reap the benefits without paying the cost). The narrow targeting of the subsidies likely diminished the program’s effectiveness, but the legacy of those subsidies remains in the current tax expenditure outlook.

An unfortunate effect of the U.S.’ preferential tax treatment for a wide array of energy sources is that incumbent energy suppliers who benefit from existing subsidies have a competitive advantage over emerging technologies that were not considered in the crafting of subsidies. Consequently, innovative energy sources are disadvantaged. The United States would be wise to revise its tax expenditures to strive for a technology-neutral policy.

The First Step to Technology Neutral Energy Policy: Expensing

The key to a technology-neutral tax treatment for energy is to treat all energy projects equally, regardless of their capital cost (innovation tends to require a lot of capital). There is a method of eliminating investments from the tax base known as expensing. Under the current tax system, investors may deduct the depreciation in asset value from their taxable income over time, or at an accelerated rate through programs such as the Modified Accelerated Cost Recovery System (MACRS). However, capital is more useful if acquired immediately than over time, so a gradual cost recovery still discourages investment. Furthermore, the Tax Foundation estimates that cost-recovery tax deductions do not fully deduct investments from taxable income, deducting an average of only 87 percent. The net effect is that the current tax system discourages capital-intensive expenses.

Many economists believe that the United States should adopt a full and immediate expensing policy economy-wide, and consider it a key to bolstering economic growth as it encourages investment. The downside of such a policy is that eliminating investment from the tax base results in less tax revenue (obviously), at an amount equal to the tax rate multiplied by the amount to be invested. Since the United States has such a high corporate tax rate, this means the on-paper calculations of the forgone tax revenue from expensing can also be quite high. However, it should be noted that such policies do not occur in a vacuum. The tax code already allows deductions over time, so the long-term “cost” difference of full-expensing is very small, all it really does is transfer lifetime deductions to the first year. In an abstract sense, an observer should consider that although the method of estimation gauges high near term costs, the theoretical change in cost over a long enough period is nil.

Replacing existing energy tax breaks with expensing would equalize the treatment of all energy sources under the tax code. Below is an example of the distortions under the current tax system, and how expensing would alleviate them. The hypothetical example assumes that any new power plant would recover 87 percent of its capital cost via depreciation deductions, and compares two hypothetical power plants with equal lifetime costs, equal electricity sales, and equal gross revenue.

Under the current system, before the introduction of investment subsidies beyond MACRS, a fossil fuel power plant has a competitive advantage because it can deduct a greater portion of its expenses from its taxable income.

| Current System (without ITC) | |||||||||

| Capital Cost | Cost Recovery | Tax Credit | Fuel Cost | Gross Revenue | Tax Rate | Taxes | Profit | Difference | |

| Natural Gas Plant | 500 | 87% | N/A | 1500 | 4000 | 35% | 722.75 | 1277.25 | 68.25 |

| Solar Farm | 2000 | 87% | N/A | 0 | 4000 | 35% | 791 | 1209 | |

Preferences for renewable energy, such as the Investment Tax Credit, offer a 30-percent tax credit for select energy sources. With such a tax credit, the profit incentive swings heavily towards the eligible energy source.

| Current System (with ITC) | |||||||||

| Capital Cost | Cost Recovery | Tax Credit | Fuel Cost | Gross Revenue | Tax Rate | Taxes | Profit | Difference | |

| Natural Gas Plant | 500 | 87% | N/A | 1500 | 4000 | 35% | 722.75 | 1277.25 | |

| Solar Farm | 2000 | 87% | 30% | 0 | 4000 | 35% | 191 | 1809 | 531.75 |

However, if the tax credits and cost recovery systems are replaced with full expensing, then there is no incentive to select one energy source over another. Private sector choice would be the deciding factor.

| Proposed Full Expensing System | |||||||||

| Capital Cost | Expensing of Capital Investment | Tax Credit | Fuel Cost | Gross Revenue | Tax Rate | Taxes | Profit | Difference | |

| Natural Gas Plant | 500 | 100% | N/A | 1500 | 4000 | 35% | 700 | 1300 | 0 |

| Solar Farm | 2000 | 100% | N/A | 0 | 4000 | 35% | 700 | 1300 | 0 |

Of course, such an example is somewhat simplified. Utilities able to make choices are still constrained by regulated electricity markets, but the point remains that full expensing eliminates distortions in utility preference.

The Second Step to Technology Neutral Energy Policy: Target Pollution, not Energy Sources

In a perfect economic policy, the United States would simply eliminate the tax expenditure subsidies, adopt full expensing, and resist the temptation to introduce new subsidies. However, since the current swathe of subsidies are mostly targeting pollution and climate, some deference to these interests must be given in a revised policy. The next best policy is to focus on eliminating the most hazardous pollutants (giving the greatest likelihood of benefits exceeding cost), and rewarding pollution abatement. A simple policy would be to replace existing energy-specific production tax credits and investment tax credits with a production tax credit based on energy cleanliness relative to the average, and for the total value of the tax credit to be scored to keep it below the expected current-law tax expenditures. Doing so would ensure a revenue-neutral policy that only rewards pollution abatement without preference for the method of abatement, capturing as many opportunities as possible.

Scoring Policy: A Revenue-Neutral and Technology-Neutral Tax Treatment for Clean Energy

The policies discussed above are possible, but consideration is needed for the proposed changes to the tax code. The current House tax reform Blueprint advocates for economy-wide full expensing with a tax cut, and plans to pay for it by eliminating tax loopholes, and broadening the tax base. Policies that would jeopardize Congress’ ability to make tax reform revenue neutral (a constraint of using budget reconciliation procedures to circumvent a filibuster) would face serious challenges. Operating within the constraints of revenue neutrality, below is a potential policy that would expand clean energy, reduce pollution, and avoid further budgetary constraint. For both simplicity and practicality, proposed new tax expenditure policies are only focused on electricity markets (though would repeal non-electricity energy subsidies), which the Energy Information Administration’s (EIA) has noted are significantly more responsive to price changes than other energy markets.

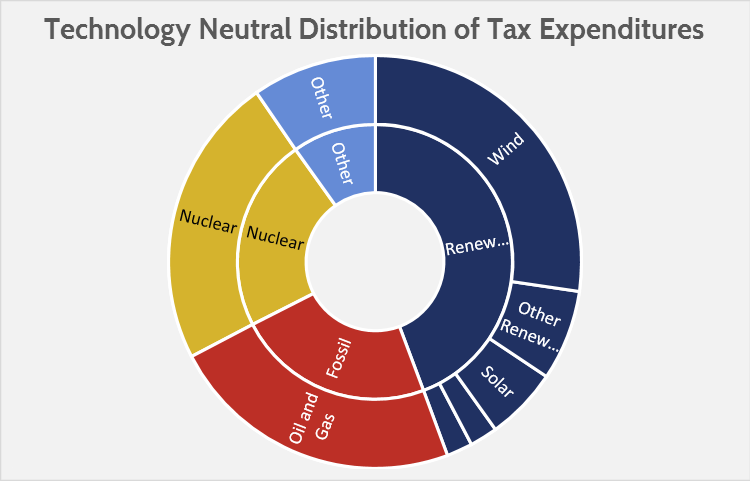

To achieve revenue neutrality, first a projection of existing tax expenditures is needed. A proper policy evaluation with a budgetary impact should be done over 10 years if possible, and the only 10-year estimate of energy tax expenditures is from the Treasury Department. Below is a chart showing the current disbursement of energy tax expenditures.

Source: AAF estimate based on Treasury Department’s FY2018 Tax Expenditures.

Source: AAF estimate based on Treasury Department’s FY2018 Tax Expenditures.

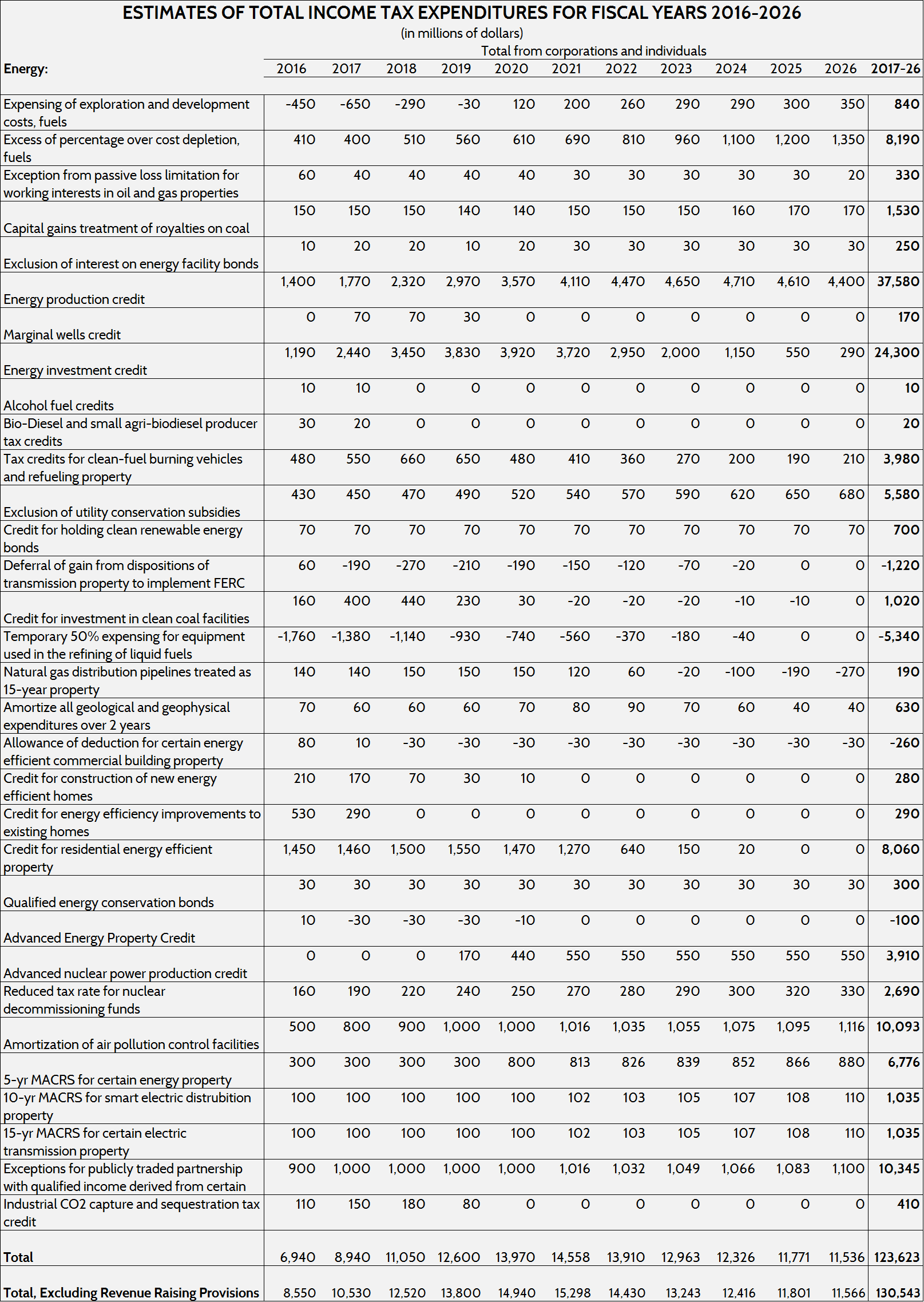

However, the Treasury definition of energy-related tax expenditure differs from that of the JCT. Furthermore, the Treasury also includes revenue-raising tax expenditures outside of its baseline (caused by replacing other subsidies, or adjusting the year in which taxes are paid). For this analysis, the American Action Forum (AAF) made its own 10-year estimate of energy-related tax subsidies, based on a composite of tax expenditure estimates from the JCT and Treasury (excluding revenue raising provisions), and Congressional Budget Office (CBO) growth expectations (the table is attached in the appendix). AAF’s estimate is $130.5 billion over 10 years, putting it roughly between the Treasury’s estimate and what a 10-year JCT estimate would be. A database which tracks fossil fuel subsidies, Green Scissors, estimates around $90 billion in fossil fuel tax breaks over 10 years, and if the Treasury’s estimated $61.9 billion in renewable energy production and investment tax credits were included, would exceed AAF’s estimate. $130.5 billion could be considered a middle-of-the-road estimate.

In the context of $130.5 billion, an estimation of the forgone tax revenue from full expensing is needed. For this, AAF used the EIA’s expectation of electricity generating capacity additions, combined with EIA estimates of capital costs, to generate an estimation of the total capital investment in new power plants over the next 10 years (both planned and unplanned additions).

| Cumulative Additions 2017-26 (GW) | Overnight Capital Cost (per KW) | Total Capital Investment (billions) | Forgone Revenue for Full Expensing (Post-Tax Reform) | Forgone Revenue for Full Expensing (No Tax Reform) | |

| Coal | 0.00 | N/A | N/A | N/A | N/A |

| Natural Gas | 35.29 | $1,040 | $37 | $7 | $13 |

| Nuclear | 4.40 | $5,945 | $26 | $5 | $9 |

| Wind | 50.88 | $2,354 | $120 | $24 | $42 |

| Solar | 5.07 | $4,120 | $21 | $4 | $7 |

| Hydro | 0.46 | $3,123 | $1 | $0 | $1 |

| Geothermal | 1.69 | $5,641 | $10 | $2 | $3 |

| Other Renewable | 12.50 | $3,704 | $46 | $9 | $16 |

| Other | 2.01 | $3,704 | $7 | $1 | $3 |

| Total | 112.3 | $268 | $54 | $94 |

Source: AAF estimates based on EIA Annual Energy Outlook 2017, and EIA Capital Cost Estimates for Utility Scale Electricity Generating Plants. Non-specific energy source capital costs treated as averages.

With such investments, assuming a post-tax reform America with a 20-percent applicable tax rate, the cost of expensing would be $53.6 billion. This leaves approximately $76.9 billion of current-law tax expenditures.

If the remaining $76.9 billion was used towards a production credit for clean energy, nitrogen oxides (NOx) would be an attractive target. NOx is correlated with particulate matter (the most important air pollutant in estimating early deaths), as well as greenhouse gas emissions. As a note, a policy of subsidizing pollution abatement would still be less effective than a revenue neutral tax on the pollutant (taxing pollution and then using revenues to cut other taxes). Based on each energy source’s relative NOx emissions to the national average pounds of NOx per MWh (about 1.3 lbs/MWh in 2011), and assuming no NOx emissions for renewable energy, the distribution of a clean energy production tax credit would be as follows (for simplicity, low-emission sources are estimated as zero emissions):

| Avg Lbs NOx/MWh | Million MWh (2017-26) | Avoided NOx (lbs, millions) | Eligible Tax Credits (billions) | |

| Coal | 2.09 | 13,250 | – | $- |

| Natural Gas | 0.37 | 10,072 | 9,303 | $22.8 |

| Nuclear | 0 | 7,747 | 10,022 | $24.6 |

| Wind | 0 | 3,691 | 4,775 | $11.7 |

| Solar | 0 | 1,011 | 1,308 | $3.2 |

| Hydro | 0 | 3,035 | 1,060 | $2.6 |

| Geothermal | 0 | 222 | 288 | $0.7 |

| Other | 0.04 | 1,434 | 4,576 | $11.2 |

| Total | 40,599 | $76.9 |

Source: AAF estimates based on Oak Ridge National Labs Environmental Quality report.

After both full expensing and a pollution avoidance tax credit, the distribution of tax expenditure subsidies would shift dramatically.

Source: AAF estimates.

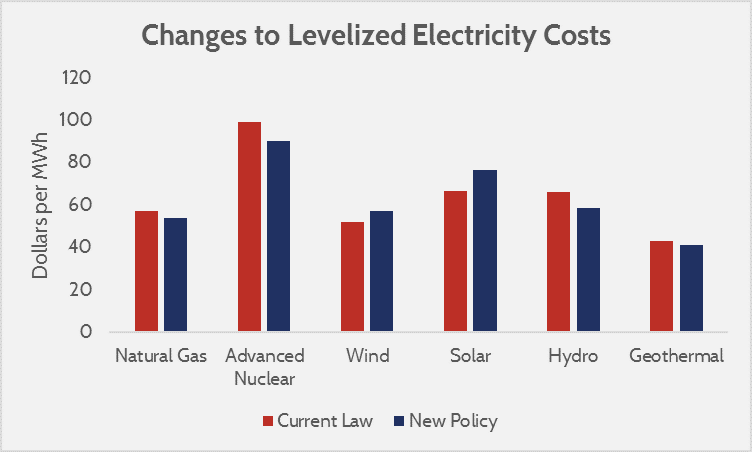

Under the technology neutral distribution of tax credits, there would be significant implications to the levelized cost of electricity. The graph below shows an estimation of the levelized cost of electricity with both full expensing and a pollution tax credit relative to the EIA’s projected costs (change in capital costs assumed as difference between MACRS and full expensing).

Source: EIA Levelized Cost of New Generation Resources and AAF estimates.

Source: EIA Levelized Cost of New Generation Resources and AAF estimates.

Under the policy change, the difference in levelized cost between advanced nuclear power and solar power would be cut in half. The only effect of tax credits would be to favor clean energy over polluting energy. Newer technologies, as well as capital intensive ones like nuclear or hydro, would no longer be disadvantaged compared to subsidized incumbents. The overall effect of the above policies is that capital-intensive energy sources are no longer subject to more taxes, and energy specific subsidies (mostly wind and solar) are replaced by a reward for pollution abatement. Nuclear power, being both capital intensive and the biggest source of clean electricity, receives the most benefit (along with hydroelectricity), whereas sources that receive large subsidies despite very small roles in the energy supply, like solar power, suffer the most.

Although too small to estimate, the above policies would also benefit carbon-capture power plants. Ancillary technology, such as battery storage, would also benefit—both from expensing, and being able to increase the amount of electricity from intermittent sources (wind and solar) that would be eligible for a tax credit.

Policy Constraints: Expiring Tax Credits

The policies stated above are assuming a status quo of legislative action that has extended expiring subsidies, or replaced them with alternative subsidies. An alternative way of viewing the U.S.’ tax expenditure is to exempt all tax credits that are expiring. Most of the observed tax breaks are for renewable energy, were introduced by the Obama Administration, and may face opposition from the Trump Administration.

A baseline projection of tax expenditures that exempts expiring credits would leave approximately $49.2 billion in tax expenditures—near equal to the cost of implementing full expensing for new electricity plants ($53.6 billion) post-tax reform. If the introduction of a tax credit aimed at replacing current law renewable energy credits with an anti-pollution credit is unfeasible, then it is still possible to implement full-expensing (assuming a 20-percent tax rate) at minimal budgetary impact. This would result in a policy that greatly benefits capital-intensive energy sources (including renewable sources), while putting a sunset on both fossil fuel and renewable subsidies.

Conclusion

If the United States wants an energy policy that promotes (or, at the least, doesn’t hinder) innovation, it needs to target the current uneven tax treatment of business expenditures versus investment. Attempting to mask the problem with targeted tax credits has only entrenched incumbents, and put unsubsidized emerging technologies at a competitive disadvantage. Moving to a full-expensing system would alleviate this, and would predominantly benefit clean energy sources. If policymakers want to take a technology-neutral approach to energy a step further, a tax credit for pollution abatement could be introduced to replace the remaining energy subsidies, and would result in a revenue-neutral policy whose only incentive is to produce clean energy over polluting energy.

Source: Estimates based on Treasury Department Tax Expenditure Estimates (FY2018), Joint Committee on Taxation Tax Expenditure Estimates (2016-2020), and where applicable projections were done using Congressional Budget Office growth rates, June, 2017, 10-year economic outlook.