Research

February 25, 2025

Health Savings Empowerment Plan: A Market-based Alternative to Medicare for All

![]()

The Health Savings Empowerment Plan (HSEP) is a proposal to augment the Affordable Care Act (ACA) to give consumers resources in the individual insurance market to protect populations with extraordinary costs, as well as offer a minimal insurance product for all U.S. citizens using federal funds allocated for the subsidized health insurance market. The aim of the plan is to provide a free market alternative to Medicare for All (M4A) under which all U.S. citizens not covered by Medicaid, Medicare, or employer-sponsored insurance are given the opportunity to access opt-out federal resources that can be used to purchase insurance and health care through consumer-owned health savings accounts (HSA). In addition, this plan would feature a Selective Risk Health (SRH) option where individuals with extraordinarily higher health risks and costs receive separate coverage to manage different health needs in a free market system.

This report details the findings of the Center for Health and Economy’s (H&E) combined Under-65 and Over-65 microsimulation models on HSEP’s impact on health insurance coverage, provider access, medical productivity, and the federal budget. While our estimates are associated with some degree of uncertainty, the summary of our findings is as follows:

KEY FINDINGS:

- With an opt-out provision for those in the individual insurance market, H&E expects the condition of universal coverage for U.S. citizens as result of the full execution of HSEP.

- By design, tfor this policy is expected to be the same as the status quo of current federal expenditures for the subsidized insurance market. .

- While the plan is intended to create universal access for U.S. citizens, there would remain 10 million uninsured non-U.S. citizens projected in 2027 when the plan is fully implemented.

- Under HSEP, an increase of 17 million insured U.S. citizens are projected to be enrolled in a private health insurance plan by 2027 compared to projections under current law, thus leaving no U.S. citizen without a health insurance contract opportunity.

Microsimulation Analysis

This analysis utilizes a microsimulation model developed for use by H&E. The model employs micro-data available through the Medical Expenditure Panel Survey to analyze the effects of health policies on the health insurance plan choices of the under-65 population and interpret the resulting impact on national coverage, average insurance premiums, the federal budget, and the accessibility and efficiency of the health care sector.[1]

The HSEP plan, which is scored in this report as taking effect in 2026 as part of reconciliation or omnibus in 2025, is a proposal to create universal coverage for U.S. citizens who are not already covered by Medicare, Medicaid, or an employer-sponsored health plan. To do so would require the creation of two sets of individual health insurance markets: one for extraordinary, expected health costs and one for the remaining and less resource-intensive population.

To implement an extraordinary cost health insurance risk pool for individuals in the U.S. market – which focuses on rare diseases and annual costs exceeding $25,000 – the first phase (Year 1) would involve establishing a national framework for identifying and categorizing eligible individuals. The government, in coordination with insurers and health care providers, would create a standardized registry for individuals diagnosed with rare diseases or those whose projected annual health care costs consistently exceed $25,000. This step requires defining eligibility criteria, conducting risk assessments, and identifying individuals through predictive analytics based on medical histories. In addition, public-private partnerships would be established to fund the pool through a combination of federal funds, insurer contributions, and state-level assistance.

In Year 2, the pool would be expanded and integrated into existing insurance markets. The implementation would involve insurers offering plans in the individual market while offloading high-cost individuals into the extraordinary cost risk pool, thereby stabilizing premiums for healthier participants. The risk pool would function to cover the catastrophic health care costs, allowing insurers to focus on standard health care coverage. Over these years, policy incentives such as tax benefits or subsidies could be provided to encourage insurers to participate. To ensure sustainability, oversight mechanisms and cost-containment strategies (such as negotiated pricing for rare disease treatments) would be put in place. By the end of Year 2, the system would be fully operational, with a focus on refining eligibility, managing costs, and ensuring equitable access for individuals with exceptionally high health care expenses.

Since H&E’s Under-65 Microsimulation Model is a plan-choice model that does not account for the over-65 population, certain assumptions and adjustments had to be made to simulate the effects the HSEP policy would have. The assumptions made are as follows:

- Use of HSAs to purchase health insurance: Starting in 2026, consumers eligible to receive funds for their HSA would be expected to use those funds to purchase a minimum level of qualified health insurance. This would also apply to the subsidized individual insurance market. A default minimum level of insurance would be provided to the consumers from which they can opt out only if they agree that funds associated with the minimum level of insurance for their geographic area will be treated as taxable income. Consumers would be required to have a personal HSA maintained by existing qualified financial institutions. The amount provided to each consumer into their HSA would be adjusted for age and gender and geographic region. Any unused portion of the HSA for the purchase of health insurance would be allowed to accumulate tax free and would only be allowed to be used for qualified medical expenses.

- Minimum qualified insurance: The minimum qualified insurance plan for HSEP would have a medical loss ratio (MLR) of 50 percent and would be assumed to be a high deductible health plan (HDHP) with a deductible set in accordance with the 50-percent MLR. Consumers would be free to purchase additional coverage with HSA or personal funds up to 90 percent MLR.

- Mandatory primary and secondary prevention: With the assumption of minimum HDHP, Internal Revenue Service Treasury guidance (NOTICE 2019-45)[1] would come into effect to guarantee pre-deductible primary and secondary prevention. This is assumed to lower the cost of the non-extraordinary care risk pools with secondary prevention costs for maintenance of major chronic condition covered pre-deductible.

- Automatic minimum insurance opt-in for catastrophic care cost: Within the individual insurance market only, there would be opt-in automatic minimum insurance available to a set of qualified default HDHPs within a geographic area of the consumer with premiums levied from the consumer’s HSA. This is expected to keep the risk pool for HDHPs predictable over the long run by geographic area with current estimates of population expected expenses.

- National network of default private minimum insurance carriers: By 2026, a national network of federal and state qualified minimum insurance carriers are assumed to be operational and offering insurance for all 50 states. They would be able to offer contracts across state lines as long as at least two states certify the carrier as compliant with associated state as well as federal consumer protection ACA regulations regarding guaranteed offer of coverage.

There are several factors not considered in the HSEP that are outside the scope the microsimulation. First, we do not consider the potential of plan switching from the employer sponsored to the individual market or vice versa. Second, we do not consider any change in Medicaid expansion from 2024 to 2033.

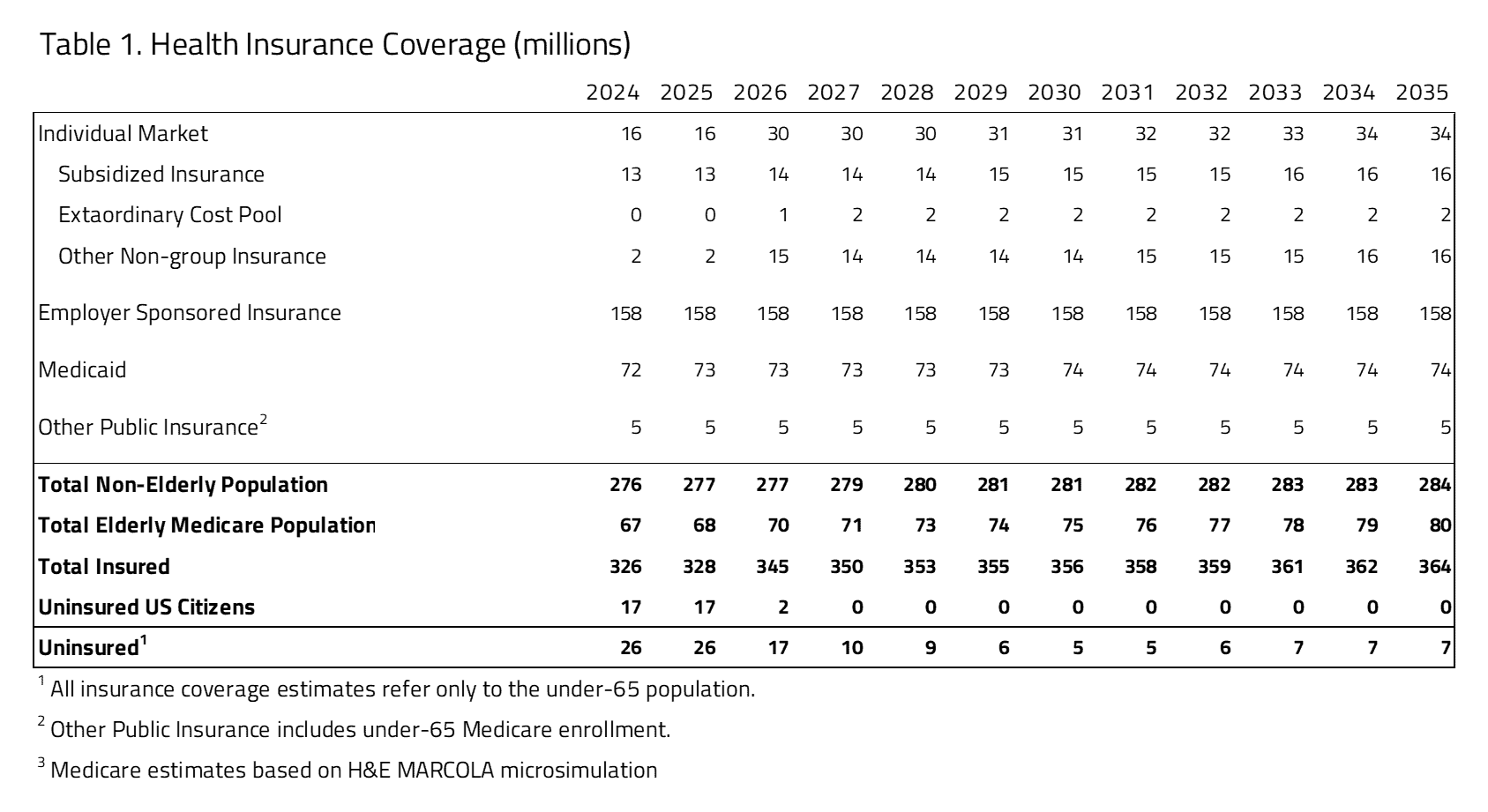

Coverage Impact

As seen in Table 1, H&E projects there will be full coverage of the U.S. citizen population by 2027. The employer sponsored and Medicaid markets are expected to be unchanged over the 10-year period examined. The number of total uninsured would decrease from 17 million in 2026 to 7 million in 2035. The remaining uninsured are expected to be non-U.S. citizens.

Productivity and Access

To evaluate access and productivity in the health care system, H&E estimates the Medical Productivity Index and the Provider Access Index. Health insurance plan designs are associated with varying degrees of access to desired physicians and facilities, as well as incentives that promote efficient use of resources. H&E estimates each index by attributing productivity and access scores to the range of plan designs available and exploiting changing plan choices to project the evolution of health care quality.

The net productivity of the HSEP plan is expected to increase compared to baseline due to an increase in enrollment of HDHP plans with mandatory primary and secondary prevention. This is due to a relative decrease in risk of unnecessary medical care associated with greater enrollment (proportionately) in more generous plans with low-cost sharing. The influx of the previously uninsured into the market required to use HSAs to obtain insurance encourages price-conscious decision-making among patients. This higher enrollment in HDHPs, combined with all private insurance required to post transparent medical prices to consumers, would create the conditions for greater price sensitivity to avoid medically unnecessary and less efficient care.

Under the HSEP, average provider access is projected to increase relative to current law due to the universal coverall of U.S. citizens. This projection assumes there is adequate provider supply.

Budget Impact

The HSEP is designed to be budget neutral and use existing projected funds already allocated to the ACA. It is expected that the ACA individual insurance market resources would be redeployed, with approximately one-third going to the cost of the extraordinary risk pool and the remaining funds to HSAs provided to consumers that will also fund a minimum level of insurance to be purchased from the consumer’s HSA account.

Additional resources may be available if the expanded ACA premium subsidies persist beyond 2025 through 2034. Under the HSEP, these would be redeployed to provide greater HSA resources to consumers.

UNCERTAINTY IN THE PROJECTIONS

The Center for Health and Economy uses a peer-reviewed micro-simulation model of the health insurance market to analyze various aspects of the health care system.[2] As with all economic forecasting, H&E estimates are associated with substantial uncertainty. While the estimates provide a good indication on the nation’s health care outlook, there is a wide range of possible scenarios that can result from policy changes, and current assumptions are unlikely to remain accurate over the course of the next 10 years. Of note, this uncertainty does not lead to biased results. H&E attempts to depict an unbiased, middle-ground representation of the future should the policy and economic environment remain constant. While the goal is to project the most likely scenario, actual events may differ significantly from published predictions.

With a proposal that puts forward substantial changes, there are bound to be myriad uncertainties when projecting different scenarios. There are three of these that will be brought up in the discussion: the magnitude of health care usage in such a system and the complications that may bring and certain cost effects that may arise from the HSEP plan; certain proposals that the model is unable to score; and the effects of the pay-fors that are included in the HSEP plan.

HSEP proposes a drastically different system that leads to many different assumptions for a plan choice model such as H&E’s Under-65 Microsimulation Model. Among those assumptions is the usage of insurance. Since the HSEP plan proposes to eliminate premiums and all cost sharing, it is highly likely that health care usage will go up – which is confirmed by the decrease in provider access above. Yet the magnitude of that increase is up for debate and increases the uncertainty involved in these estimates.

[1] Additional Preventive Care Benefits Permitted to be Provided by a High Deductible Health Plan Under § 223, NOTICE 2019-45, US Treasury

[1] https://healthandeconomy.org/2017-project-a-winning-alternative-to-obamacare/#_ftn2

[2] Parente, S.T., Feldman, R. “Micro-simulation of Private Health Insurance and Medicaid Take-up Following the U.S. Supreme Court Decision Upholding the Affordable Care Act.” Health Services Research. 2013 Apr; 48(2 Pt 2):826-49.