Research

June 2, 2022

The Future of America’s Entitlements: What You Need to Know About the Medicare and Social Security Trustees Reports

Executive Summary

Today, the Social Security and Medicare Trustees issued their annual reports detailing the financial state of America’s two largest entitlement programs. The reports echo past conclusions: Social Security and Medicare are still going bankrupt.

At its current pace, Medicare will go bankrupt in 2028 and the Social Security Trust Funds for old-aged benefits and disability benefits will become exhausted by 2035.

A quick look at the data proves just how broken our current entitlement programs are. An American Action Forum analysis of the data found other startling statistics, including:

- Medicare’s Annual Cash Shortfall in 2021 was $409 billion;

- Payroll taxes would have had to increase by almost 18 percent to pay for Medicare Part A in 2021; and

- Over the next 75 years, Social Security will owe $20.4 trillion more than it is projected to take in.

What You Need to Know About the Medicare and Social Security Trustees Reports includes one-pagers and relevant statistics on:

- The solvency of Medicare;

- The president’s stewardship of Medicare;

- The solvency of the Social Security Trust Fund;

- The solvency of the Social Security Disability Insurance (DI) program; and

- The solvency of the Social Security Old-age and Survivors Insurance (OASI) program.

The Solvency of Medicare

This week, Treasury Secretary Janet Yellen released the 2022 Medicare Trustees Report. This annual report delivered yet another reminder to the American public that Medicare is undeniably going bankrupt.

The report estimates that the Medicare Hospital Insurance Trust Fund will be bankrupt by 2028. While the bankruptcy projection may snag the headlines, there are three key budgetary numbers that shouldn’t go unnoticed.

|

$409 Billion |

Medicare’s Annual Cash Shortfall in 2021

|

|

$6.4 Trillion |

Medicare’s Cumulative Cash Shortfall Since 1965

|

|

29 Percent |

Medicare’s True Contribution to the National Debt

|

Continuing with the Medicare status quo is unacceptable. Balancing Medicare’s annual cash shortfalls under the existing system would prove devastating to seniors and failing to reform the status quo would result in the following impacts:

|

9 Percent Increase |

Annual Payroll-Tax Increase Needed to Balance Medicare Part A

|

|

$4,728 Increase |

Annual Premium Increase Needed to Balance Medicare Part B

|

|

$1,952 Increase |

Annual Premium Increase Needed to Balance Medicare Part D

|

The Executive Branch’s Stewardship of Medicare

An Evaluation of the Executive Branch’s Medicare Stewardship

Each year, the Trustees Report provides a non-partisan evaluation of the president’s stewardship of Medicare. Prepared annually for Congress by the Office of the Chief Actuary, the Trustees Report offers unparalleled detail on the financial operations and actuarial status of the Medicare program. In short, it’s where every administration’s soaring Medicare rhetoric meets fiscal reality. So far, President Biden has resisted undertaking significant Medicare reform. The 2022 Trustees Report provides a sense of what the future may look like should Medicare continue to remain unchanged, and why sooner or later Medicare reform is inevitable.

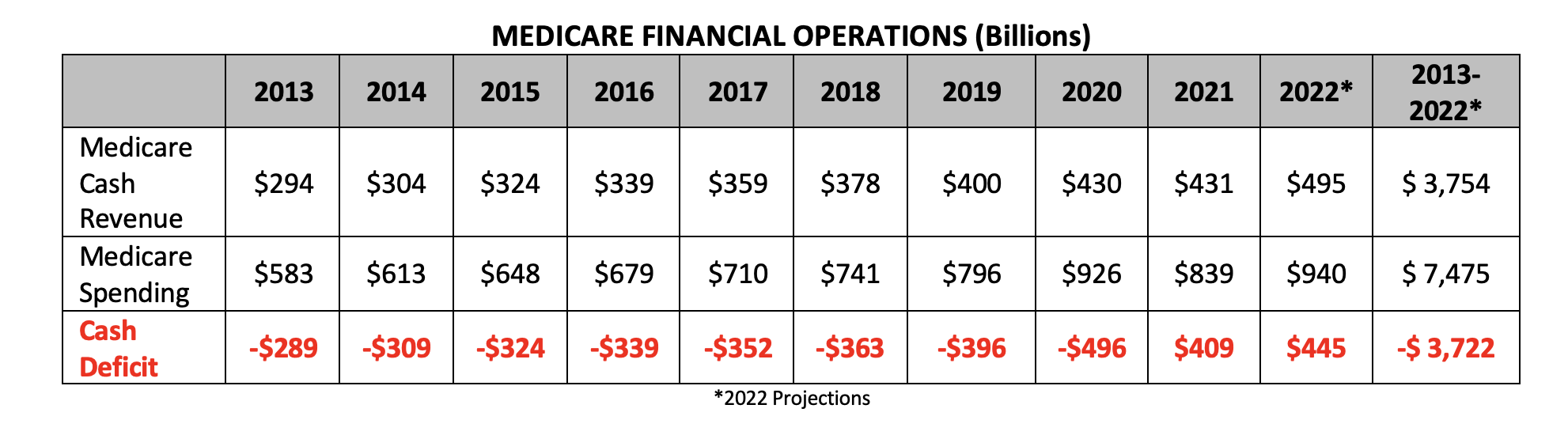

MEDICARE FINANCIAL OPERATIONS (Billions)

The Obama Administration oversaw a $2.4 trillion cash shortfall over eight years (2009-2016). The Trump Administration oversaw its own $1.6 trillion Medicare cash shortfall during this presidential term. The fiscal reality is that continuing the previous two administration’s Medicare policies and leaving Medicare unchanged all but guarantees bankruptcy. The Trustees project that President Biden will oversee an $854 billion cash shortfall before he is even halfway through his first term.

With such unprecedented levels of cash shortfalls continuing through the budget horizon, maintaining the status quo ensures that Medicare will soon not exist for today’s seniors, let alone future generations of Americans. These rising costs and the measures necessary to cover them will increasingly harm seniors if Medicare reform is not undertaken.

| Medicare and Medicaid Will Cost $2 Trillion by 2024 | Medicare Costs Will Continue to Rise

|

The Solvency of the Social Security Trust Fund

This week, the board of trustees that oversees the Social Security program released its annual report. The report shows that the financial outlook for the nation’s primary safety net for retirees, survivors, and the disabled will fail to meet its promises to future seniors in the absence of meaningful reform.

The report estimates that the combined (retirement and disability) Social Security Trust Funds will be exhausted by 2035, one year later than last year’s estimate. The Trustees Report makes clear the program’s structural imbalance that puts at risk the retirement benefits of millions of working Americans.

|

$126.4 Billion |

Social Security’s Contribution to the Debt in 2021

|

|

$20.4 Trillion |

Social Security’s Unfunded 75-Year Liability

|

|

13 Years |

Years Until the Trust Funds Are Exhausted

|

The Trustees Report paints a distressed picture of Social Security’s financial health and demonstrates that the present course is unsustainable. Social Security is now contributing to the annual deficit, while promised benefits exceed planned funding by over $20 trillion. The implications of failing to reform the status quo are:

|

20 Percent |

Reduction in Benefits in 2035

|

|

26 Percent |

Payroll Tax Increase

|

The Solvency of Social Security Disability Insurance

This week, the board of trustees that oversees the Social Security program released its annual report. The report reflects continued improvement in the outlook for the Disability Insurance (DI) program.

The report estimates that the DI Trust Fund is solvent over the long term. This outlook marks the first time since 1983 the program has been sustainable over the long-term. The program has faced recent solvency challenges, requiring a payroll tax reallocation in 2015.

|

$85.3 Billion |

DI’s 10-Year Contribution to the Debt

|

|

$-56 Billion |

DI’s Unfunded 75-Year Liability

|

The Trustees Report reflects a significant decline in the outlook for America’s safety net for disabled workers.

Solvency of Social Security Old-Age and Survivors Insurance

This week, the board of trustees that oversees the Social Security program released their annual report. The report shows that the Old-age and Survivors Insurance (OASI) program remains unsustainable and will be unable to meet the needs of future beneficiaries absent reform.

The report estimates that the OASI Trust Funds will be exhausted by 2034. The report also makes clear several additional structural challenges that endanger the millions of current and future retirees and survivors who rely on this program.

|

$126.5 Billion |

OASI’s Contribution to the Debt in 2021

|

|

$20.5 Trillion |

OASI’s Unfunded 75-Year Liability

|

|

12 Years |

Years Until the OASI Trust Fund Is Exhausted

|

|

71.6 Million |

Number of Beneficiaries in 2034 (Trust Fund Exhaustion Year)

|

The Trustees Report makes clear that the primary federal retirement program remains unsustainable. On its present course, the program is on track either to reduce the retirement benefits of over 71 million Americans, or to raise taxes significantly on future workers.