The Shipment

April 10, 2025

April Fools: Trump Pauses Largest Tariff Hike in History

Liberation from “Liberation Day” Tariffs

What’s Happening: Yesterday, President Trump posted on Truth Social that the “reciprocal” tariffs announced on April 2 (“Liberation Day”) would be put on pause for 90 days – ostensibly to buy time for the more than 75 countries that are attempting to negotiate new trade deals with the United States. While these tariffs are delayed, there remains a universal 10-percent tariff on all U.S. trade partners, a 25-percent tariff on steel and aluminum, and a 25-percent tariff on automobiles. Meanwhile, China was slapped with a tariff of 125 percent after it announced a retaliatory 84-percent tariff on all U.S. goods, bringing the final tariff rate to 145 percent. Additionally, the European Union initially retaliated with tariffs on over $21 billion worth of U.S. goods in response to already implemented U.S. steel and aluminum tariffs but has since put these on pause to facilitate negotiations.

Why It Matters: The pause of the “Liberation Day” tariffs means that the $366.5–$391.6 billion in increased costs for U.S. consumers and businesses has also been, for the most part, delayed. Unfortunately, some companies, amid the trade chaos, already increased prices and planned for tariff surcharges. It is also important to remember that there is still a universal 10-percent tariff and a whopping 145-percent tariff on China, which combined would theoretically cost U.S. consumers over $300 billion. More likely than not, however, demand for Chinese products will dry up due to this large barrier, thereby reducing any government revenue that may have been collected. This large-scale trade barrier will reduce the accessibility of foreign goods for U.S. consumers, limiting the supply of certain products and raising the price of alternatives if demand holds relatively steady. One example of this predicament is the fact that 41 percent of computers were imported from China in 2023. Filling this gap in a short period of time is nearly impossible, meaning producers of alternatives to Chinese products will raise their prices, assuming stable demand for computers, adding additional costs to U.S. consumers that are tariff-related even if they’re not direct tariff costs.

Looking Ahead: A single social media post that merely pauses Great Depression-era tariff rates will not reverse the damage to trade partner relationships or supply chains overnight. The whiplash of U.S. trade policy has, for the foreseeable future, completely altered the way close allies judge the reliability of the United States. Mexico plans to diversify its trade away from the United States, while Canada makes similar plans, echoed by new campaigns undertaken by Canadian businesses and consumers to buy fewer U.S. goods and take vacations elsewhere. It remains to be seen what types of trade deals will be struck over the next 90 days and what sort of messaging the Trump Administration will use. Many questions remain: Will the administration consider it a victory to establish more free trade at the end of its tariff onslaught? Will the higher tariffs announced on April 2 be reimplemented? If the tariffs snap back into place, the United States is back to square one. Future deals that require countries to purchase more of a certain U.S. product make for good headlines, but at the end of the day, it is individuals and firms that make market-based decisions, not countries or leaders.

Reflecting on “Liberation Day” Fantasies

Last week, the Trump Administration declared U.S. “liberation” from foreign products in an announcement that shocked global markets, economists, and pretty much everyone else. Even more shocking was the sudden delay of U.S. “liberation” announced yesterday with the 90-day pause period. The highly anticipated “reciprocal” tariffs, which were levied on nearly every country, were much larger than expected, creating a universal baseline import duty of 10 percent and bringing the average U.S. tariff rate to a level not seen since the 1930s. The rollout of the “Liberation Day” tariffs, as well as many of the claims surrounding them, are shrouded in fallacies and fantasies that deserve analysis. Below are some of the key problems that demonstrate why this costly trade policy should be buried for good.

American vs. Foreign Products: One of the main rationales behind instituting across-the-board tariffs was the need to “liberate” the United States from dependence on trade partners for goods. This thinking puts goods into two basic categories: “American” and “foreign.” But these categories are not as neat as one might think. Many, if not most, U.S. products rely on inputs from abroad. A car, for example, might be assembled in the United States but have an engine from Germany, steel from South Korea, and electronics from Taiwan. Peanuts might be grown in the United States, but the plastic container in which they’re packaged may have been imported from Japan. A portion of the wood used to make pencils may have come from Canada, while the machines used to shape the wood could have parts from Europe, and the raw graphite probably came from China. All these inputs are “foreign,” but they are compiled to manufacture “American” pencils, employ U.S. workers, and generate profit for U.S. shareholders. In effect, exorbitant tariffs on all imports will not only raise prices for imported finished goods but also raise prices for goods made in the United States and harm U.S. businesses.

Tariffs for Revenue…or Tariffs for Re-shoring: The common claim in support of recent tariffs is that they will provide a new source of revenue to address budget deficits – and, at the same time, incentivize companies to make products in the United States. In the long run, however, these goals are mutually exclusive. The more U.S. consumers buy domestic products to avoid the added cost of foreign goods, the less tariff revenue the government will generate. And if consumers bite the bullet and continue purchasing foreign goods, the Trump Administration can claim to have boosted revenue, but it can’t claim to have boosted domestic manufacturing. Either consumers and businesses will respond to the tariffs by switching to domestic alternatives – thereby increasing (to some degree) manufacturing production and employment – or they will continue to import large quantities of goods for the government to tax. In the end, the administration cannot have it both ways.

Penguin Tariffs: Another interesting situation with the rollout of these tariffs was which countries and territories were listed – and which were not. For example, the Heard and McDonald Islands, home to a couple hundred thousand penguins, was slapped with a 10-percent tariff, while Russia, a geopolitical adversary, was not listed at all. Presumably, all countries – including Russia – were hit with the 10-percent minimum tariff, but the absence of a specific mention is odd (the White House rationalized that Russia already faces extremely high tariffs and sanctions). Meanwhile, the supposed rationale for listing uninhabited islands was to prevent any loopholes countries could use to avoid tariffs. This does not hold up for two reasons. First, those penguin-heavy islands are a territory of Australia, which was already hit with a 10-percent tariff. Second, the likelihood is very low that any country would (or could) build the infrastructure needed for trade on remote islands to circumvent tariffs.

The Formula: The United States Trade Representative published the formula used to calculate the tariff rates introduced on “Liberation Day” for each country. Each country’s rate is equal to dollar values of U.S. exports to that country, minus U.S. imports from that country, divided by U.S. imports from that country, multiplied by the price elasticity of import demand (ε) and the elasticity of import prices (φ). To the untrained eye, this formula may appear to be a reasonable way to calculate a tariff rate. Breaking this down further, ε equals 4 and φ equals 0.25, which means that – to calculate the total of tariff and non-tariff barriers another country places on the United States in an effort to identify the proper level of “reciprocity” – the formula simply divides the dollar-value trade deficit with that country by U.S. imports from that country. Setting aside the fact that the elasticity used was incorrect, this formula sets a tariff rate that doesn’t even attempt to consider other countries’ tariffs on the United States and instead considers only the “trade deficit,” apparently based on the belief that a trade deficit is an indication of cheating, trade barriers, and manipulation.

The Apple Problem: Apple has announced it will begin to shift more production from China to India, likely to take advantage of the comparatively lower tariff rate. With the incoming tariffs, this makes geopolitical and economic sense at the moment. Consider, however, how the administration’s tariff formula is calculated. Assume Apple moves all production from China to India. In that event, Apple products heading for the United States will come from India and not China. In a vacuum, this would grow the U.S. trade deficit with India and shrink the U.S. trade deficit with China. Using the administration’s tariff formula – which, recall, does not punish countries that levy tariffs on the United States but rather countries that have trade deficits with the United States – tariffs on India would then be increased while tariffs on China would be lowered, leaving Apple in the same situation before shifting production. Thus, the administration has apparently failed to engineer a way to incentivize companies to leave China, at least in the long run.

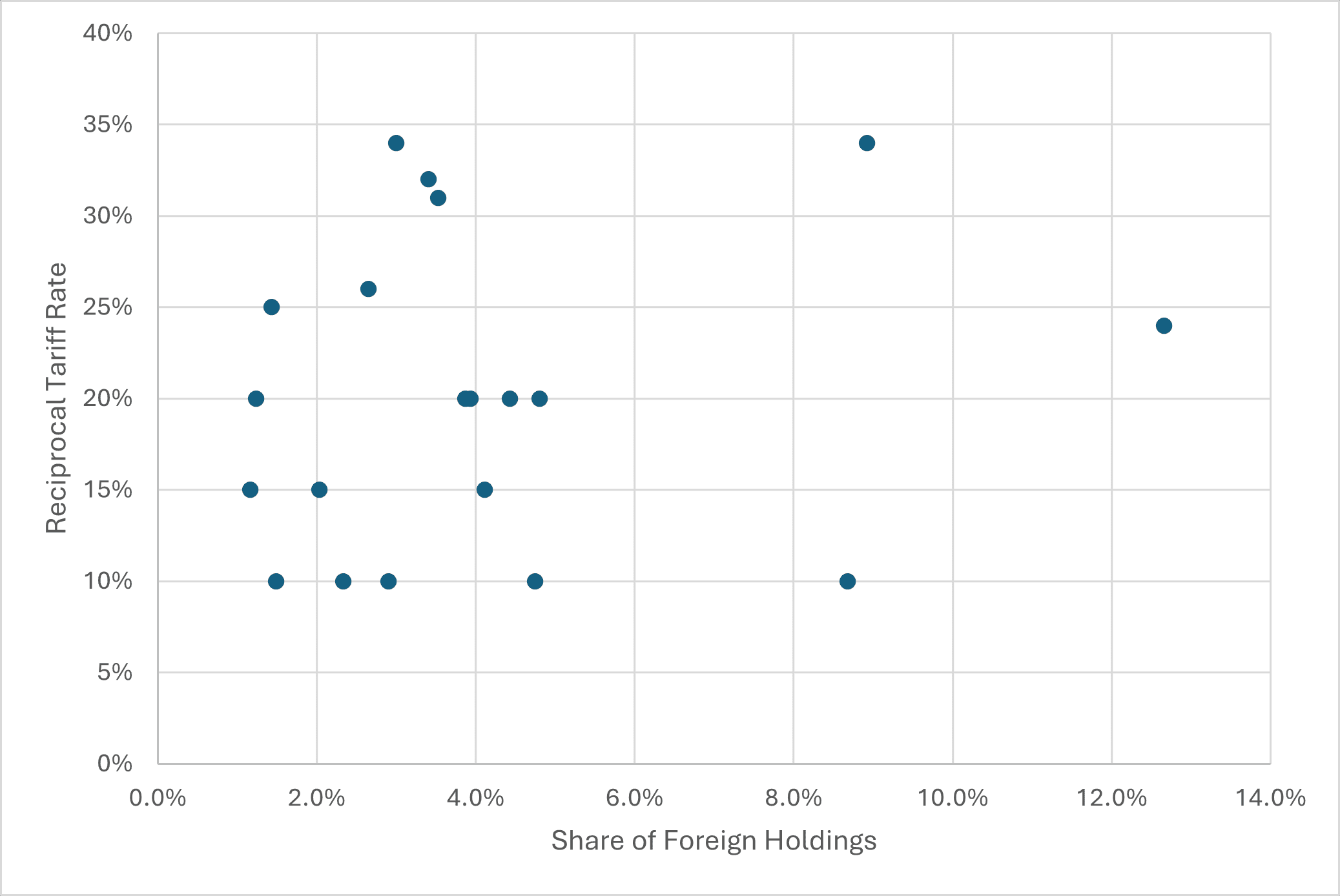

Foreign Holdings of U.S. Treasuries vs. “Liberation Day” Tariff Rate

Source: Treasury Tic Data

The chart above displays the top 20 foreign holdings of U.S. treasuries as a percentage of overall foreign holdings (X axis) and that country’s corresponding “Liberation Day” tariff rate (Y axis). The largest holders include Japan, China, and the United Kingdom, but there appears to be no real correlation between foreign holdings and the tariff that was introduced on April 2. This indicates that foreign holdings of treasuries were not a factor in the administration’s decision to impose tariffs.

![]()