Weekly Checkup

August 9, 2019

Flying Into Surprise Bills

With this week’s news that the House Committee on Ways and Means is putting together legislation to reduce surprise billing, there are now likely to be four different (yet similar) bills aimed at combating surprise billing. One of the more niche problems that a couple of these bills seek to solve is that of surprise bills for air ambulance transport. It’s worth considering the nature of the air ambulance market to see what kinds of policies might work.

According to the Government Accountability Office (GAO), about 69 percent of air ambulance trips are out of network for the privately insured. The median charge for out-of-network trips was greater than $36,000 in 2017, although we do not know how much the patients were responsible for paying. Not only are air ambulance trips expensive, but the market for these services is also very concentrated. The GAO found that, as of 2015, three companies own roughly two thirds of all air-ambulance helicopters nationally. Because there are so few providers, and because ambulance services are unpredictable, air ambulance providers have little incentive to contract with insurers: One large company reported that it contracted with less than 1 percent of the 1,000 private insurers it works with per year. And because there are such high fixed costs for air ambulance providers (helicopters, planes, training, etc.), high prices do not necessarily encourage more entrants into the market.

The air ambulance market is clearly unique in some ways, and policies must account for these unique factors to be successful. For example, in S. 1895, which the Senate Health, Education, Labor, and Pensions Committee produced, the solution for all surprise out-of-network bills (including for air ambulance services) is to charge the patient the in-network rate while allowing insurers to pay their in-network rate for the same or a similar service. If the insurer doesn’t have a negotiated rate for the service, it can pay a rate similar to the prevailing one in that area. (To learn more about the various proposals for surprise billing, you can read my recent paper.)

Under the system laid out by this bill, however, it’s highly likely that there would be many geographic areas where there would not be a single negotiated rate between a private insurer and an air ambulance company. In these instances, the geographic area would have to be expanded until a rate for the area can be established, potentially allowing the rate set for services hundreds of miles away to dictate the rate for all areas in between.

The state of Wyoming recently proposed a different approach to this problem. Last week, Wyoming proposed expanding Medicaid to cover air ambulances for all Wyoming residents. In essence, Wyoming’s plan would treat air ambulances like a public utility. Medicaid would determine statewide requirements for air ambulance coverage, rates would be determined through a non-benchmarked competitive bidding process, and the state would make periodic flat payments to providers and set cost-sharing requirements for patients.

It’s unsurprising that Wyoming would produce a waiver proposal like this. As states go, Wyoming has one of the more unique relationships with air ambulances. Because the state’s population is spread out over so much land, air ambulances are used more in Wyoming relative to other states. According to GAO data, Wyoming has seven times as many air ambulance bases per capita than the United States as a whole, while Wyoming bases serve 40 percent fewer people per base than the national average.

Though Wyoming represents a unique case among states, its proposal represents a creative solution to a market failure. State intervention could, perhaps ironically, inject competition into a market that currently lacks it, and the proposal also avoids rate setting, an added bonus. The proposal would need to overcome a host of barriers to become law—and even more complications if it were to be approved—but the proposed policy would address the unique challenges posed by air ambulances.

Chart Review

Ryan Haygood, Health Care Policy Intern

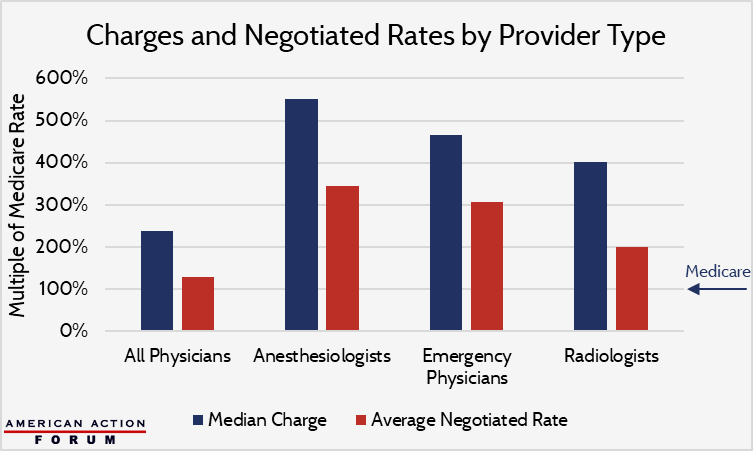

Hospitals and physicians generate most of their profits from the privately insured. On average, physicians’ privately negotiated rates are only 28 percent greater than Medicare payments, but their median charges are 139 percent greater. Providers’ charges are rarely paid in full and typically serve more as a starting negotiating point. Charges do matter, though, for the uninsured and patients whose doctors aren’t included in their insurer’s network. They matter most when a patient is unable to choose their provider and are unexpectedly treated by an out-of-network doctor: When this happens, the patient is likely to incur a “surprise bill.” It’s no accident that anesthesiologists, ER doctors, and radiologists – the providers most likely to encounter patients out of network – charge rates significantly higher than what Medicare pays. For these doctors, surprise billing can be lucrative, not simply because they collect their elevated charges more often than other doctors, but also because they can leverage the profitability of their out-of-network options to demand higher in-network rates. Legislation from the Senate HELP Committee (noted above) would forbid providers from collecting their full charges in “surprise” out-of-network scenarios and tie payment to the median privately negotiated rate, which itself may fall as providers lose leverage. The Congressional Budget Office projects lower premiums and $25 billion in public savings as negotiated rates prevail over artificially high charges.

Data are from the USC-Brookings Schaeffer Initiative for Health Policy.

From Team Health

The Latest Drug Pricing Bill – A Mixed Bag

Deputy Director of Health Care Policy Tara O’Neill Hayes examines the various proposals in the Senate Finance Committee’s bill seeking to address drug pricing.

Worth a Look

Axios: Medicare will now cover a costly cell therapy for cancer patients

Wall Street Journal: Health-Care Spending Soars in New York State