The Daily Dish

June 4, 2026

A Check up on Consumer Health

Consumer spending represents nearly 70 percent of the U.S. economy, so regularly tracking consumer health can help forecast the direction of the broader economy. Despite taking jab after jab to the chin – including tariffs, geopolitical conflicts, and five years of inflation above the Federal Reserve’s 2-percent target – the American consumer has remained resilient. There are signs, however, that a knockout punch may not be far off.

Recent data from the Bureau of Economic Analysis showed that the personal savings rate has slumped from 5.5 percent a year ago to 2.6 percent in April 2026, the lowest level since mid-2022. This steady decline suggests that consumers are dipping into their monthly savings just to maintain their current standard of living as rising prices continue to plague everyday essentials such as food and gasoline.

In addition to drawing down cash savings, increased financial pressure has pushed more savers to tap their retirement accounts – typically seen as a last resort. Data from Fidelity showed that 2.4 percent of workers initiated a new 401(k) loan in Q1 2026, an uptick from 2.3 percent in the same quarter a year earlier. Moreover, 19.2 percent of workers have an outstanding 401(k) loan in Q1 2026, up from 18.8 percent in Q1 2025. As the cost of covering the basics continues to climb, those who have already leveraged their retirement accounts – and locked into a rigid repayment schedule – may be left with few options, putting long-term financial health in jeopardy.

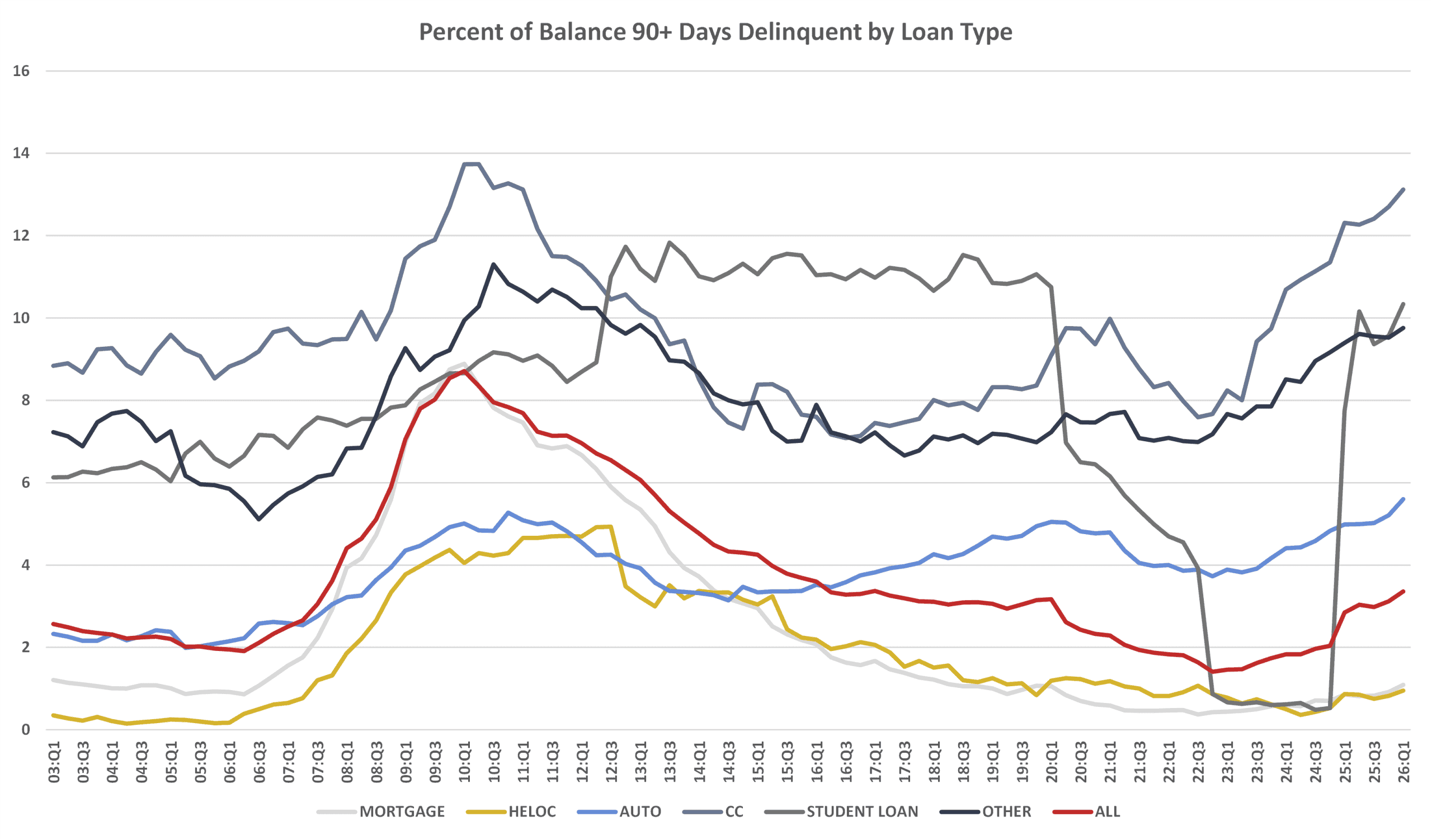

Data from the New York Fed’s Survey of Household Debt and Credit further highlight the mounting stress. The percent of debt balances 90+ days delinquent has steadily climbed from 1.41 percent at the end of 2022 to 3.36 percent in Q1 2026. Notably, student loan delinquencies surged from 0.53 percent in Q4 2024 to over 10 percent in Q1 2026 following the expiration of the COVID-era repayment freeze and subsequent on-ramp period in late 2024. Moreover, even though overall credit card balances declined in Q1 2026, the share of balances 90+ days delinquent continued its upward march, reaching 13.12 percent. Auto debt delinquencies are also on the rise. The percent of balance 90+ days delinquent rose from the near-term bottom of 3.73 percent in Q4 2022 to 5.60 percent in Q1 2026, coinciding with the steep climb in the average amount financed for new car loans, which reached nearly $42,000 in Q4 2025.

Compounding these debt dynamics is the drop in purchasing power. While the price of everyday essentials is rising, wages are not keeping pace. Annual average hourly earnings growth for private production and nonsupervisory workers has slowed from around 4.0 percent in 2025 to 3.7 percent in April. On a monthly basis, inflation has outpaced wage growth by 0.6 percentage points and 0.3 percentage points in March and April, respectively. On an annual basis, the rise in inflation surpassed annual wage gains in April, putting a firmer squeeze on consumer budgets.

The economic engine driving the U.S. economy faces a standing eight count as savings continue to dwindle and wage growth fails to exceed overall inflation. It is no wonder consumer sentiment is at an all-time low.

Freddy’s Forecast: May Jobs

The April jobs report showed payrolls increased by 115,000. This was fewer than the 185,000 jobs added in March, but it still represents the first back-to-back monthly increase since April and May 2025. The unemployment rate was unchanged at 4.3 percent.

Since the last report, data from ADP showed the pace of private-sector hiring gained steam in May as employers added 122,000 workers to payrolls. Small businesses added 67,000 workers while large and medium businesses increased headcount by 40,000 and 17,000, respectively. Job gains were more broad-based compared to recent months as goods-producing industries added 8,000 workers and service providers gained 114,000. Education and health services continued to outperform, adding 57,000 new hires. Manufacturers, meanwhile, halted a monthly job-cutting streak that began in April 2024, adding 3,000 jobs.

The Bureau of Labor Statistics’ Job Openings and Labor Turnover Survey data showed that job openings jumped to 7.6 million in April, the highest level in nearly two years. An increase in openings of 668,000 in professional and business services helped offset a 135,000 decrease in finance and insurance. The hiring rate, however, remained low, slipping to 3.2 percent during the month from 3.5 percent in the prior month.

Initial jobless claims rose for a second consecutive week ending May 30 to 225,000. It was the highest level since early February. The four-week moving average, which smooths out weekly volatility, increased to 214,750. Continuing claims, meanwhile, fell 8,000 during the week of May 23 to 1.777 million.

For May, expect gains in payrolls to decelerate to 75,000 and the unemployment rate to rise to 4.4 percent. Growth in average hourly earnings holds steady at 0.2 percent for a 3.3 percent annual gain.

Fact of the Day

Since the start of 2026, the federal government has published $974.5 billion in total regulatory net cost savings and 56.4 million hours of net annual paperwork increases.