The Daily Dish

February 9, 2026

Artificial Intelligence (AI) and the Macro Outlook

To paraphrase Dickens, AI is the best of things, AI is the worst of things. At the micro level, does the threat of job destruction outweigh the promise of new activities, products, and jobs? At the macro level, a similar debate is underway on the impact of AI on the outlook for inflation, growth, and monetary policy.

As reported by the Financial Times

Top academics have dismissed Kevin Warsh’s claim that an AI-induced productivity boom will create room for interest rate cuts, according to a snap FT economists’ poll that highlights the challenges facing Donald Trump’s pick for Federal Reserve chair.

Warsh, who Trump named as his nominee to replace Jay Powell at the end of January, has argued that AI will trigger “the most productivity enhancing wave of our lifetimes — past, present and future”. This will expand output and pave the way for the Fed to cut US borrowing costs from their current level of 3.5-3.75 per cent without triggering a rise in prices, he says.

Almost 60 per cent of the 45 economists polled by the University of Chicago’s Clark Center for Financial Markets this week said any impact on prices and borrowing costs over the next two years was likely to be negligible — lowering PCE inflation and the neutral interest rate by less than 0.2 per cent over the next two years.

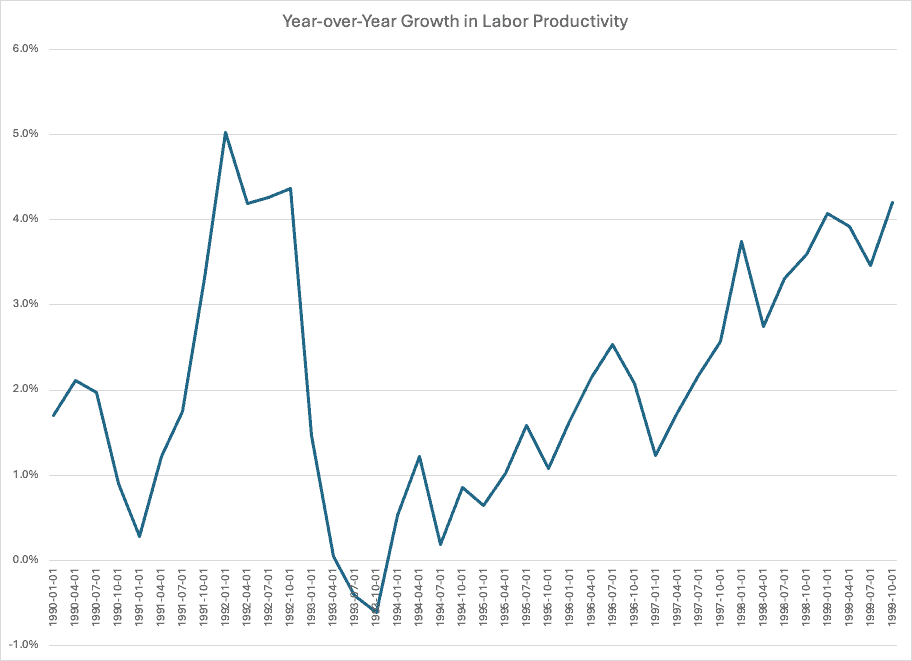

Certainly, recent productivity growth has been quite rapid – a 4.9 percent annual rate in the 3rd quarter of 2025. But is that a durable, seismic shift that policymakers can count on for years to come? Or is it another blip in the notoriously noisy productivity data? Proponents of the former view point to the late 1990s and then-Fed Chair Alan Greenspan’s bet on productivity growth. Those data are reproduced below. At what point would one be confident that there is a shift in the underlying growth of productivity?

The other channel by which AI is affecting the macro outlook is spending on AI investments – software, servers, electricity generation, and so forth. As reported by The Wall Street Journal:

It’s bigger than the railroad expansion of the 1850s, the Apollo space program that put astronauts on the moon in the 1960s and the decades long build-out of the U.S. interstate highway system that ended in the 1970s.

We’re talking about the data centers now being built and financed by some of the world’s biggest companies in the AI boom.

Four U.S. tech giants – Microsoft, META, Amazon, and Google – are planning to spend up to $670 billion to build out AI Infrastructure this year alone as they scramble to increase the computing power needed to operate and scale their AI-related endeavors.

The scale of the investment is stunning. At one end of the spectrum, it means a huge investment boom with dramatic near-term growth impacts. Or, the four giant firms may fight over a very few server farms. This will dramatically push up the prices of components, yielding a big nominal investment boom. But measured in real (inflation-adjusted) terms, it amounts to a lot less. Or, the output and price impacts may fall in between. In short, AI presents a number of very important – and entirely unclear – issues for policymakers.

Fact of the Day

Between the first and third quarter of 2025, service exports grew by $61 billion, with every major export category (except for government services) expanding.