The Daily Dish

February 25, 2026

How U.S.-Centric Is the Inflation Problem?

Inflation has been at the center of economic discussions in the United States since the year-over-year consumer price index (CPI) jumped from 1.4 percent in January 2021 to 9.1 percent in June 2022. At the time, there was a vigorous debate over the relative contribution of more costly, congested global supply chains versus U.S. monetary and fiscal policies to the overall rise in inflation. The former were supply shocks and, presumably, outside the control of U.S. policymakers, while the latter influenced aggregate demand and were literally the responsibility of policymakers.

Eakinomics’ reading of the data is that in 2021 itself, roughly half was attributable to global supply chains, while half was due to massive over-stimulus by fiscal and monetary policies. A key part of the evidence is that in 2021 Europe and Canada did not undertake massive demand stimulus. As a result, their rise in inflation is a rough proxy for the impact of global supply chains and other supply-side shocks.

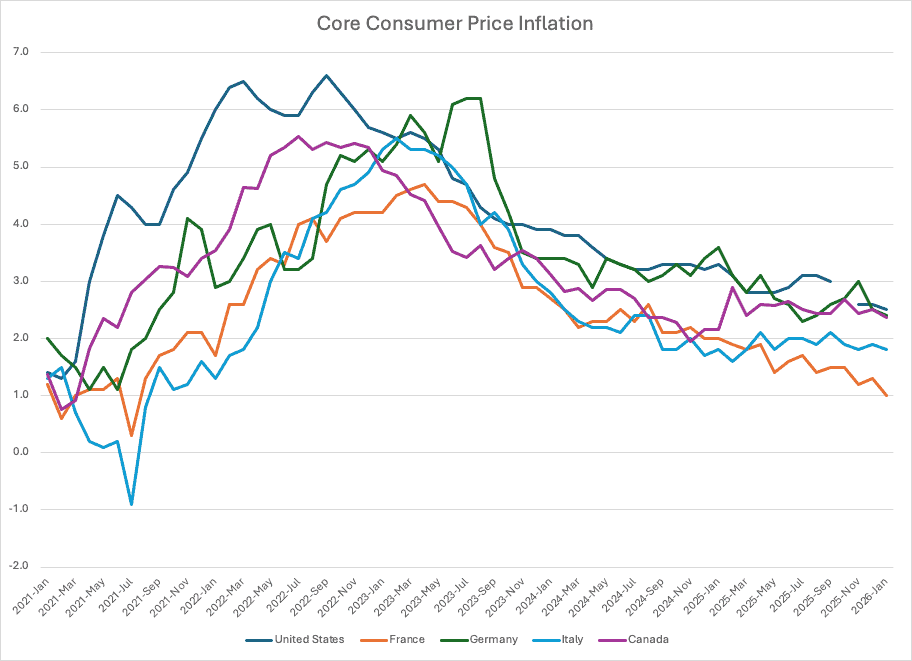

It is now 5 years later, and the debate continues as to whose fault it is that U.S. inflation is not back to the 2-percent target. To get a bit of international perspective, the graph below shows the evolution of core (non-food, non-energy) CPI inflation in the United States, France, Germany, Italy, and Canada from 2021 to the present. (Using core makes more sense as the post-Ukraine-invasion data in Europe are heavily influenced by energy costs.) The graph shows that in 2021 and early 2022, inflation rose more sharply and to a higher level in the United States than in the other countries.

Since then, the Federal Reserve has been operating under its dual mandate for full employment (sustained job growth) and price stability (an inflation target of 2 percent). The European Central Bank has a single mandate, which is implemented as an inflation target, while the Bank of Canada’s mandate is to promote the economic and financial welfare of Canada. It has as part of this a 2-percent inflation target, which it implements by keeping inflation in the 1–3 percent range,

What have been the results? France and Italy have moved down more quickly and are below the 2-percent target rate. In contrast, Germany has evolved in a fashion very similar to the United States, while Canada has had a recent uptick in inflation to put it on par with the United States. It is hard to conclude from this that inflation is a shared phenomenon driven by global supply chains. If it were, all the countries would be below 2 percent.

Instead, whatever common elements are shared by globally traded consumer and business goods have been augmented by country-specific decisions in the United States, Germany, and Canada. That means it is fair game to look at the contribution of tariffs and other fiscal policies to the path back to 2 percent. And it is fair game to look for places to improve the Fed’s performance, as well.

Fact of the Day

Between 1987–2015, the median age of first-time home buyers fluctuated between 28–31 years before climbing to an all-time high of 40 between July 2024 and June 2025.