The Daily Dish

February 10, 2026

Delayed Jobs Report Is a Two-for

January’s employment report – which was delayed until Wednesday, February 11 due to the partial government shutdown – is a two-for: the data for January and the annual benchmark revisions to the payroll data. This first look at employment in 2026 is likely to continue the trend from 2025 of slowing job growth. More on that later.

Recall that back in September, the Bureau of Labor Statistics (BLS) published its preliminary benchmark revisions to total nonfarm employment for April 2024–March 2025. The preliminary estimate showed 911,000 fewer jobs, or 0.6 percent of employment, were created over that 12-month period than first estimated. On Wednesday, the BLS will publish revisions to reflect the annual benchmark process and updated seasonal adjustment factors. Not seasonally adjusted data beginning with April 2024 and seasonally adjusted data beginning with January 2021 are subject to revisions. The Friends of the Bureau of Labor Statistics – a group of statistical and economic organizations focused on supporting, educating, and advocating for the BLS – provide a detailed explanation of the benchmarking process and other changes the BLS is making to improve the accuracy of initial estimates.

Expectations are that the data for the latter half of 2025 will come in weaker than originally estimated. Pessimists include Federal Open Market Committee (FOMC) Governor Christopher Waller. In a statement following his dissent at the January FOMC interest rate policy meeting, Governor Waller stated that “Payroll gains in 2025 were very weak. Compared to the prior ten-year average of about 1.9 million jobs created per year, payrolls increased just under 600,000 for 2025.” Waller added that “last year’s data will be revised downward soon to likely show that there was virtually no growth in payroll employment in 2025. Zero. Zip. Nada.”

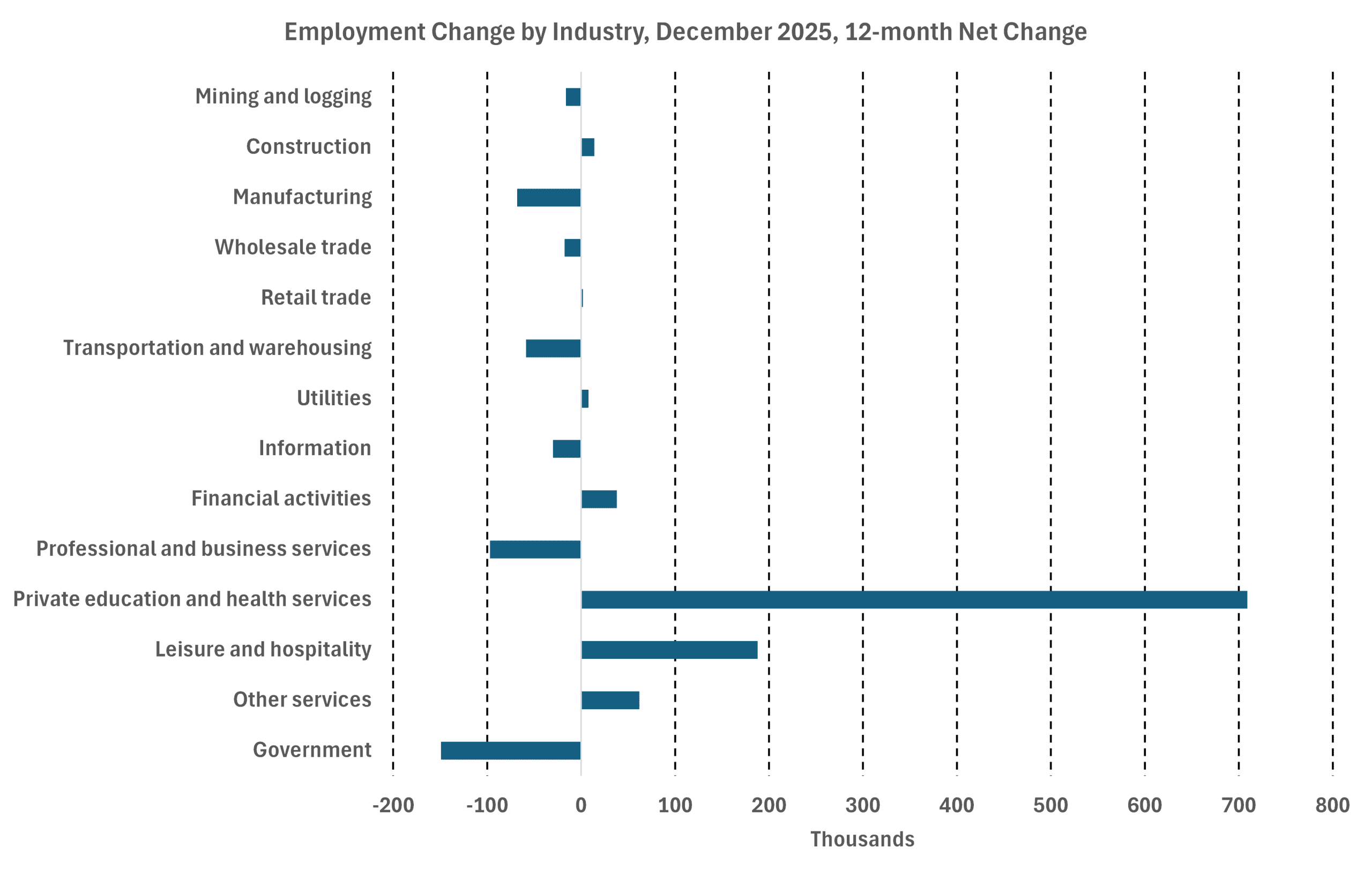

Total nonfarm employment expanded by just 584,000 in 2025, or 49,000 per month. That was a sizable drop from nearly 168,000 per month in 2024 and 217,000 per month in 2023. Moreover, the job gains were anything but evenly distributed. Private education and health services added 709,000. The rest of the economy was flat to negative (see graph below). Manufacturers cut 68,000 jobs while trade and transportation shed nearly 60,000. Is it a coincidence that both sectors are trade-reliant? Doubtful.

Freddy’s Forecast: January Jobs

Jobs Wednesday. It just doesn’t sound right, but here we are. After the short, partial government shutdown, the BLS will report the first look of the jobs market in 2026.

A quick recap of where we’ve been: The December jobs report showed hiring held steady at 50,000 while the unemployment rate ticked down to 4.4 percent.

Since the last report, data from ADP showed that private employers added a paltry 22,000 workers to their payrolls in January. The topline number was buoyed by the gain of 41,000 jobs among medium establishments, while small establishments added zero and large establishments slashed 18,000 workers. Gains were largely concentrated in education and health services. Manufacturers, which have lost jobs every month since March 2024, cut 8,000. In an interview on CNBC, ADP Chief Economist Nela Richardson noted that private payrolls for 2025 were cut by 212,000 as part of that company’s annual revision process, which is a similar process to that of the BLS, bringing the annual total to 398,000.

Data from the Institute for Supply Management were generally positive in January. Economic activity in the manufacturing sector expanded for the first time in 12 months. Growth in new orders, production, and new export orders – which measures foreign demand – lifted the overall index. Employment remained in contraction in January, albeit at a slower pace than in December. The January services index was unchanged from December. Production expanded, but new orders and employment growth slowed.

The Job Opening and Labor Turnover Survey data from BLS were weak and further confirmation that the low-hire, low-fire job market continues. The rate of hiring remained low at 3.3 percent, more consistent with an unemployment rate of 8 percent. Job openings also slumped to 6.542 million in December from 6.928 million in November, with nearly 1 million fewer job openings than a year ago.

Initial jobless claims ticked up to 231,000 for the week ending January 31, an increase of 22,000 from the previous week. Continuing claims, meanwhile, remained below 1.9 million during the week ending January 24 at 1.844 million. The four-week moving average, which smooths out weekly volatility, was 1.851 million, the lowest level since October 5, 2024. Initial claims suggest that firings remained muted.

For the January report, expect payroll growth of 42,000 and the unemployment rate to stay at 4.4 percent. Growth in average hourly earnings holds steady at 0.3 percent for a 3.6-percent annual gain.

Fact of the Day

In 2025, 62 percent of organizations reported experiments with agentic artificial intelligence workflows across varied industries such as health care, finance, retail, and customer service.