The Daily Dish

August 18, 2023

Interest Rates Spike

Yesterday, mortgage rates hit their highest level since 2002, with Freddie Mac’s average rate on a 30-year, fixed loan jumping to 7.09 percent. Meanwhile, global interest rates hit 15-year highs, with Bloomberg reporting: “In early US trading Thursday the 30-year Treasury yield rose as much as seven basis points to 4.42%, slightly exceeding last year’s high. It was below 4% as recently as July 31. The US 10-year yield approached 4.31%, within a few basis points of its 2022 peak. The equivalent UK yield jumped to a 15-year high, while its German counterpart approached the highest since 2011.”

What is going on?

It is unsurprising. During the past week, the data have continued to show unexpected growth momentum. Retail sales rose sharply, housing permits and starts advanced solidly, new claims for unemployment insurance dipped, and the Philadelphia Fed manufacturing index rose for the first time since the fall of 2022. Continued strong growth in demand raises the specter of inflation that is more resilient to the Fed’s tightening efforts, which increases the probability that interest rates would have to be raised further.

On Wednesday, the minutes of the most recent meeting of the Federal Open Market Committee indicated that the Fed was prepared to do just that: “With inflation still well above the Committee’s longer-run goal and the labor market remaining tight, most participants continued to see significant upside risks to inflation, which could require further tightening of monetary policy.” So, the rise in interest rates is consistent with the need for higher rates and the expectation that the Fed could make such a move in the near future.

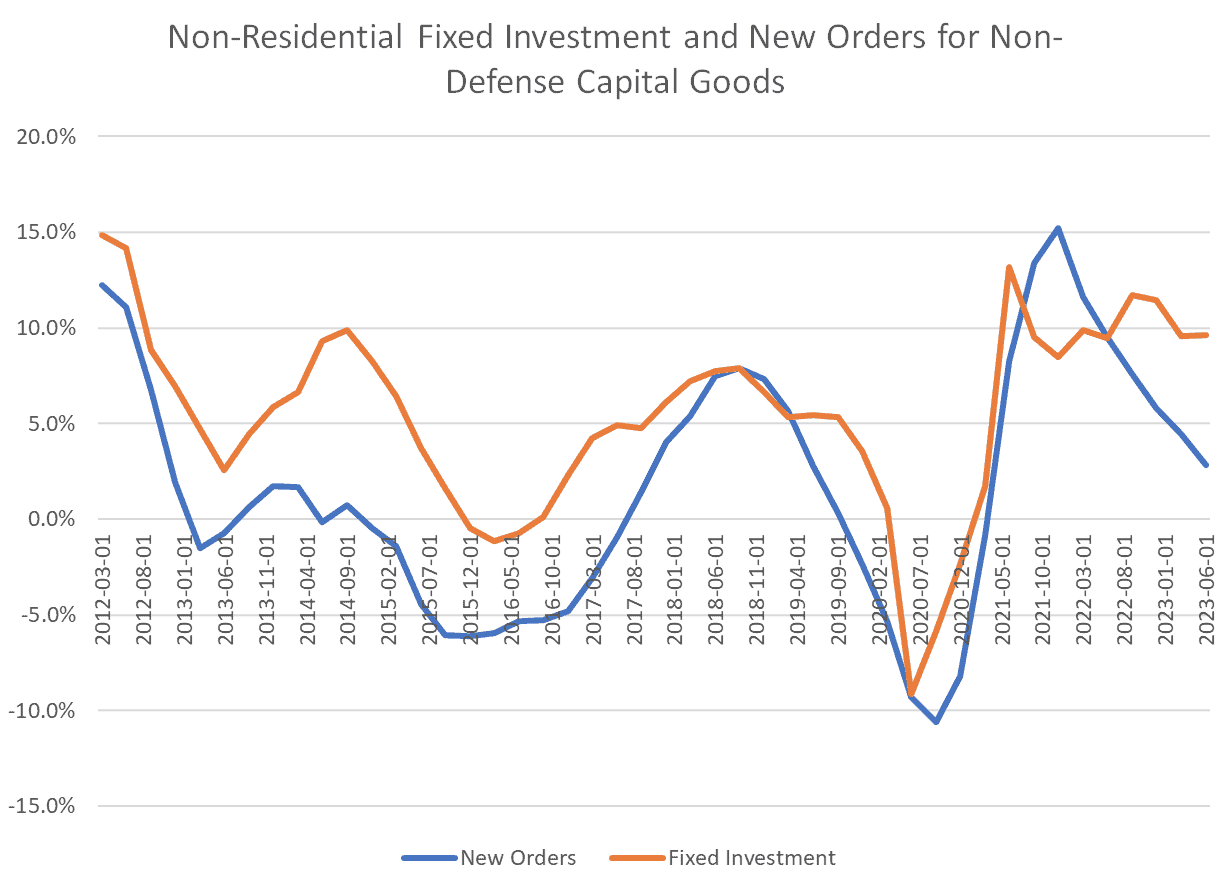

But why has economic growth remained so strong? As Eakinomics has noted, the typical postwar recession is led by a decline in business investment spending, followed a quarter or two later by a falloff in household spending. The key to the resilience of the current macroeconomy has been non-residential fixed investment in 2023. Structure, equipment, and intellectual property investment all softened or declined at times in 2022, but business investment has unexpectedly firmed.

The graph below shows the annualized growth rate of fixed investment over the past six months compared to the growth rate of new orders for non-defense capital goods (excluding aircraft; three-month moving average) six months prior. Typically, orders are a good predictor of future growth in investment spending. Yet in late 2022 and 2023, investment growth has stayed well above what one might have expected based on the orders data.

Will investment stay elevated or come back to Earth? Will the economy continue to push off the threat of recession? Will the Fed continue to need further tightening of monetary policy? It turns out these are all the same question.

Fact of the Day

Since January 1, the federal government has published rules that imposed $356.5 billion in total net costs and 165.6 million hours of net annual paperwork burden increases.