The Daily Dish

May 18, 2026

The Powell Record

The handoff of the chairmanship of the Board of Governors of the Federal Reserve is underway. Kevin Warsh has been confirmed by the Senate and awaits being sworn in. In the interim, Jerome Powell, whose term ended on Friday, will be chair pro tempore. It is a natural moment to assess the performance of the Powell Fed.

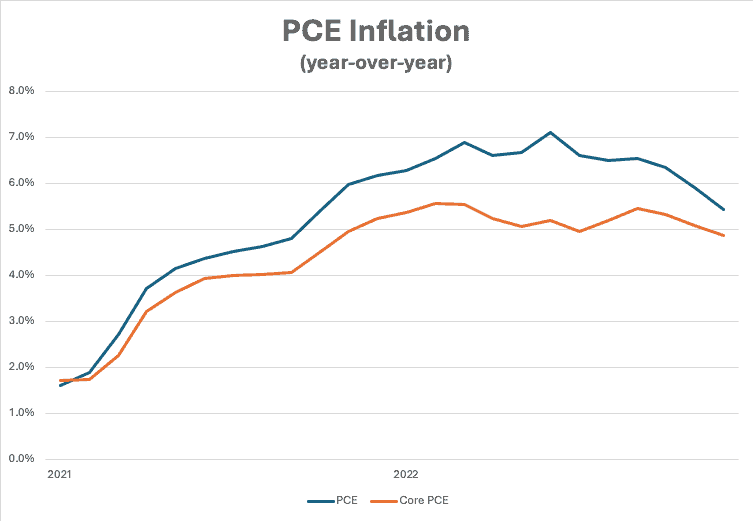

First, it should be acknowledged that the Powell performance was a high degree-of-difficulty routine. He faced three 100-year events – a pandemic, the Trump Liberation Day tariffs, and a sustained assault on Fed independence – and one all-too-frequent event: a highly disruptive Mideast war. It also contained a major policy error when inflation was permitted to run up in 2021. The path of inflation, measured by the personal consumption expenditures (PCE) price index, is captured in this graph:

As one can see, year-over-year PCE inflation was 1.7 percent in January 2021 (the core measure was 1.6 percent). It rose sharply in early 2021 and kept rising steadily to a peak of 7.1 percent, 18 months later. The policy error was to keep the federal funds rate at zero and continue quantitative easing throughout 2021. In effect, as the inflation bonfire blazed steadily higher, the Fed kept its foot on the gas.

The mystery is, why? One line of reasoning is that the Fed thought the withdrawal of the coronavirus and the opening of the economy meant a return to 2019 conditions. In that year, the Fed had chosen to keep rates low even though unemployment had dropped to low levels and wages were rising rapidly. Usually these are the indicators that would lead the Fed to pre-emptively tighten policy and avoid an increase in inflation. The Fed labelled its policy stance “running it hot” and held listening sessions around the country that were effectively celebrations of its success. One could understand that the Fed might think the end of the pandemic meant it could run very loose monetary policy without inflation. That did not turn out to be the case.

Another factor is that President Biden did not re-appoint Powell until December 2021. Once confirmed in early 2022, the Fed quickly turned to a tightening cycle. Again, one could understand the Fed not wanting to make a 180-degree change in policy without having its leadership in place.

In any event, it was a major error that required a return to the 2-percent target to completely restore Fed credibility. Sadly, 5 years later that remains unfulfilled. Powell will, properly, receive praise for leadership skills and effectiveness in fighting for Fed independence. The Achilles heel of his record, however, is the actual performance in managing inflation.

Fact of the Day

The Shipment estimates that Section 122 tariff costs (and future refunds) could amount to approximately $25–$30 billion.