The Daily Dish

November 25, 2025

What Is Keeping Inflation Up?

On December 9 and 10, the Federal Open Market Committee (FOMC) will meet to decide the near-term future of monetary policy. Recall that the FOMC has eight permanent members – the seven Fed governors, including the chairman, and the president of the New York Federal Reserve Bank (usually the FOMC vice chair). The other four members are drawn from the remaining 11 regional Federal Reserve banks on a rotating basis. At the moment, the latter four are Austan Goolsbee (Chicago), Susan Collins (Boston), Alberto Musalem (St. Louis), and Jeffrey Schmid (Kansas City).

The question that faces them is: Should the committee cut rates by 50 basis points (one-half of one percent), 25 basis points, or not at all? Could it even justify raising rates? Given the Fed’s dual mandate for price stability and full employment, a key aspect of the decision is the outlook for inflation.

Since Liberation Day in April, most of the inflation discussion has focused on tariffs, and their upward pressure on prices. Inflation, as measured by the Consumer Price Index, reached a low of 2.3 percent in April, and has risen to 3.0 percent since. Careful recent empirical research indicates that:

Prices began rising immediately after the broader tariff measures announced in early March and continued to increase gradually over subsequent months, with imported goods rising roughly twice as much as domestic ones. Our estimated retail tariff pass-through is 20 percent, with a cumulative contribution of about 0.7 percentage points to the all-items Consumer Price Index by September 2025.

Taken at face value, this says that all of the recent surge in inflation is due to tariffs, and there is more in store. This is a dilemma for the FOMC, as tariffs destroy purchasing power and are a headwind to growth – but so are high interest rates. It is a judgment call, but may lead some to favor additional cuts.

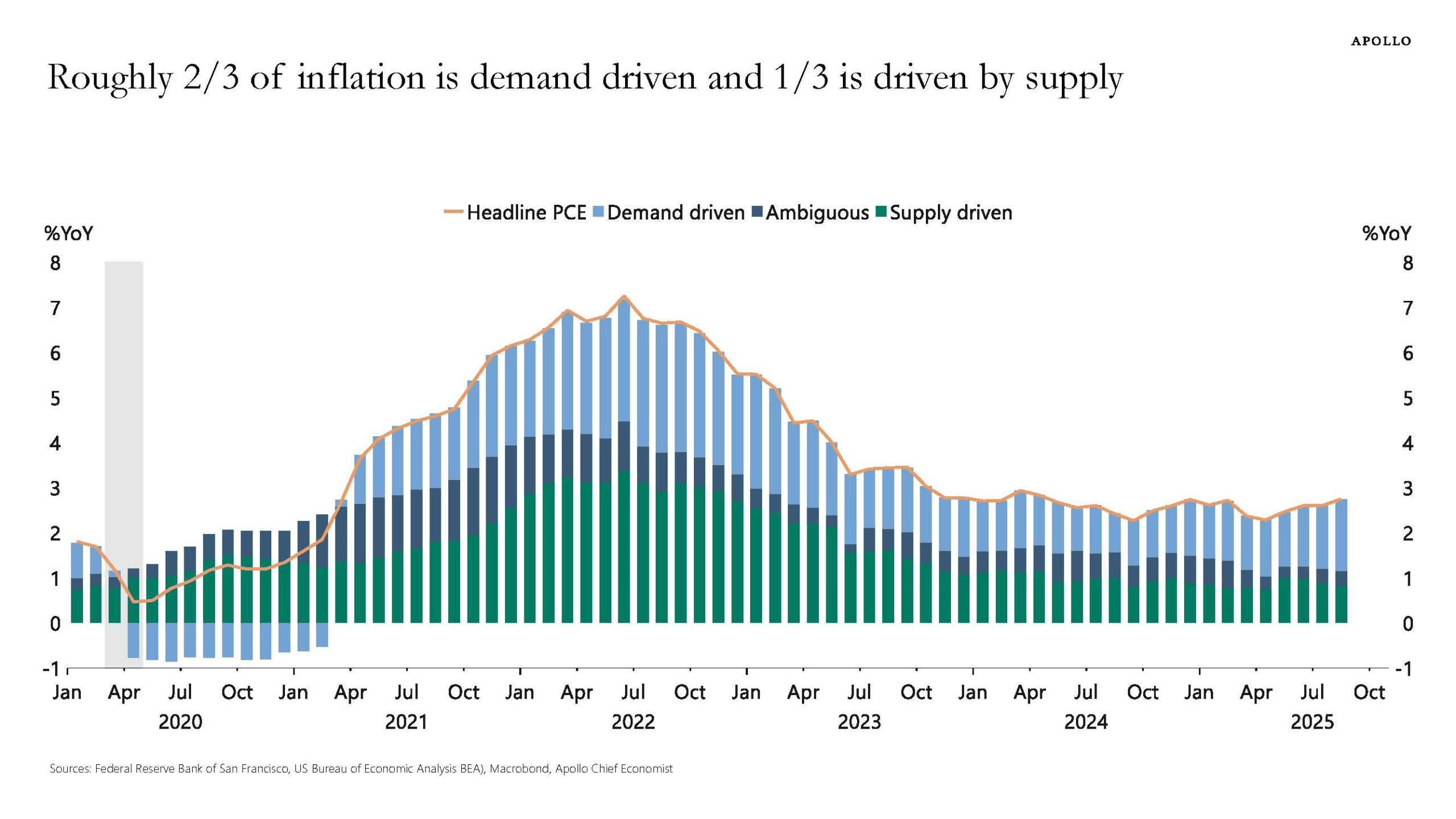

In the other direction, Torsten Slok (Apollo chief economist) published this decomposition of the source of inflation (based on research by the San Francisco Fed). It indicates that a majority (two-thirds) of the inflation is driven by strong demand – not cost pressures such as tariffs – and this is consistent with the stronger labor market found in the much-delayed September employment report.

Where does that leave the FOMC? Divided. Reports indicate that there is sentiment ranging from no change to a 50-basis-point cut. This is hardly surprising given the ambiguous nature of the evidence. Expect a close vote.

Fact of the Day

Across all rulemakings, federal agencies published roughly $925 million in total costs and added 3.1 million paperwork burden hours.