The Daily Dish

November 19, 2025

What We Were Watching During the Shutdown

The 43-day government shutdown left policymakers, market participants, and the public in a data desert. But private-sector data – while not a perfect substitute – helped quench our thirst. A few things we were watching:

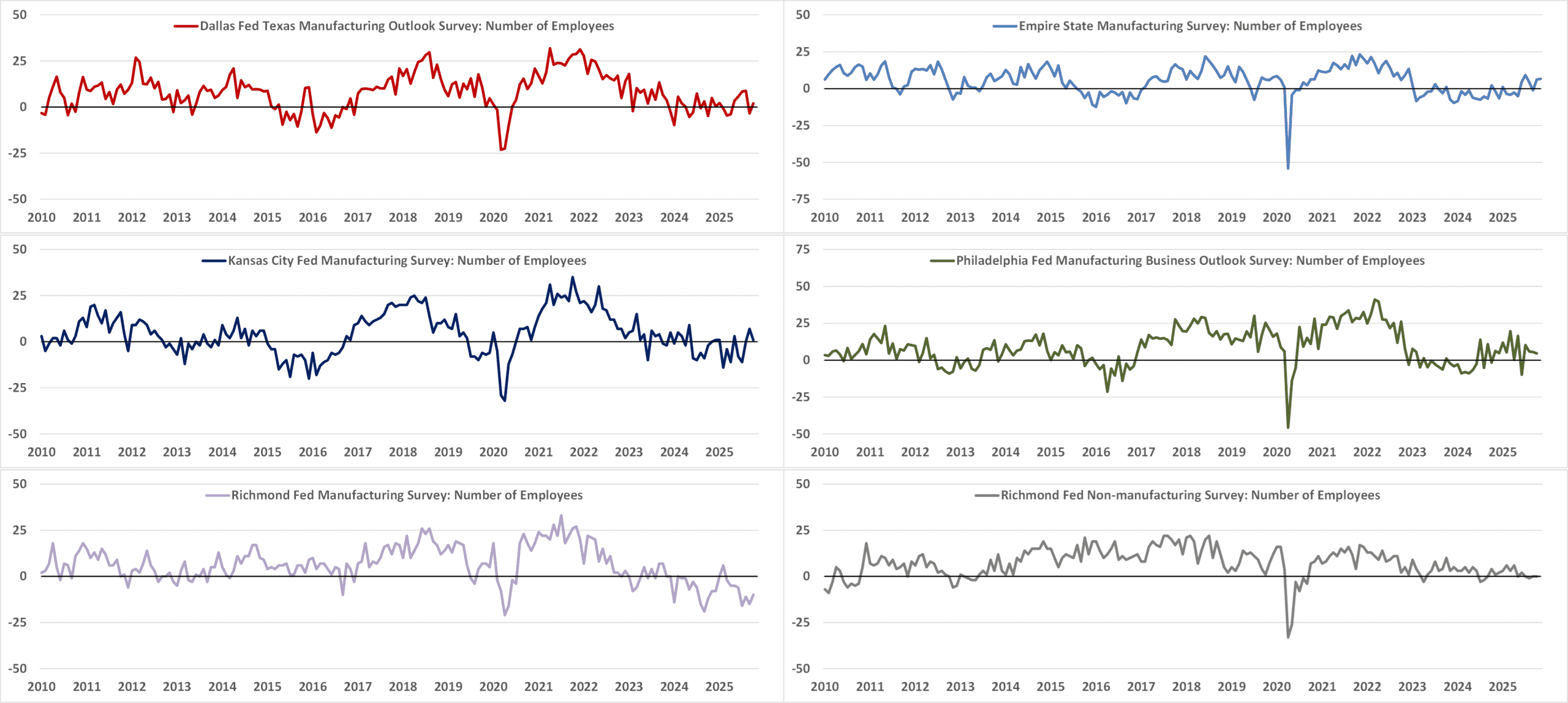

The Federal Reserve Regional Banks publish diffusion indexes, which compare the share of respondents reporting an increase or a decrease, for the current number of employees. To little surprise, there was weakness across the board.

The Richmond Federal Reserve showed the number of employees in the manufacturing sector declined for the eighth consecutive month in October, albeit at a slower pace than the prior three months. Outside of manufacturing, the number of employees remained unchanged. Two Fed surveys – Kansas City and Philadelphia – showed that the number of manufacturing employees increased, but at a slower pace than the prior months, while the Dallas and New York Fed showed a faster pick-up in the number of employees.

The Fed’s October Beige Book noted that “employers reported lowering head counts through layoffs and attrition” in most Districts, while “employers that reported hiring…favored hiring temporary and part-time workers over offering full-time employment opportunities.” In all, the labor market continued to show signs of a further slowdown based on the Fed data.

The Federal Reserve Bank of Chicago estimated that the unemployment rate likely ticked up to 4.4 percent (rounded) in September and largely held steady in October. That would be a slight uptick from the official August unemployment rate of 4.3 percent.

Data from Revelio labs, a workforce analytics firm, showed that employers shed an estimated 9,000 jobs in October, while hiring in September was just 33,000.

More bad news came from Indeed, as job postings continued their steady decline, down 6.5 percent from a year ago to the lowest level since February 2021.

ADP – best known for its monthly National Employment Report – recently started publishing a weekly estimate of the four-week moving average of private-sector job creation. Private-sector employers shed an average of 2,500 jobs per week for the four weeks ending November 1, an improvement from the 14,250 job cuts estimated for the week ending October 25. The most recent estimate equates to 10,000 fewer jobs over the prior four weeks.

These alternative indicators present an opportunity to compare their performance to official government statistics as they play catch-up.

Freddy’s Forecast: And We’re Back– September Jobs…Again

It’s been a while, so let’s do a quick review of the August jobs report. Total nonfarm payroll employment was little changed, up just 22,000 during the month. The unemployment rate rose to 4.3 percent, its third-straight monthly increase. Average hourly earnings, meanwhile, increased 10 cents, or 0.3 percent in August, which was a 3.7-percent increase from the prior year.

Since the last report, it’s been radio silence from the government statistical agencies. But the upcoming deluge of data – although stale at this point – will be released in the coming weeks.

Data from the Institute for Supply Management (ISM) showed manufacturers continued to shed jobs in October, but at a slightly slower pace than in September. Survey respondents noted that tariffs and the trade war continued to harm some manufacturers and keep others sitting on the sidelines. A machinery manufacturer noted that depressed agricultural exports “negatively impacts farmer revenue and the likelihood of farmers investing in new equipment,” while a computer and electronics products manufacturer stated that “Challenges with tariffs on production equipment necessary for internal production makes it difficult to justify expansion of capacity.” The ISM services survey, meanwhile, showed employers continued to reduce headcount during the month.

The Challenger report showed that employers announced 153,074 job cuts in October, up 157 percent from the same month a year ago. Through October, employers have announced just under 1.1 million job cuts, a 65-percent increase over the first 10 months of 2024.

ADP reported that private employers added 42,000 jobs in October, the first monthly gain since July. Data for September – which is the reference period in Thursday’s jobs report – showed that the private sector shed 29,000 jobs.

Expectations for the September report, initially planned for publication on October 3, remain the same as the original forecast. Expect topline payroll growth of 48,000. The unemployment rate is likely to tick up to 4.4 percent while growth in average hourly earnings increases 0.3 percent, or 11 cents, for an annual gain of 3.7 percent.

The October report, whenever we get it, will be incomplete. While the topline payroll number will be published, the unemployment rate will not because the data were never collected.

Update: The Bureau of Labor Statistics (BLS) announced that it would not publish an October 2025 Employment Situation release. The agency noted that the Current Employment Statistics survey (the payroll survey) for October will be published with the November 2025 data, now scheduled for Tuesday, December 16. BLS confirmed that the household data will not be retroactively collected. The agency note and updated release calendar can be found here.

Fact of the Day

Data from the Census Bureau’s 2023 American Housing Survey showed there were 133 million occupied housing units, split between owner-occupied 65 percent and renter-occupied 35 percent.