Insight

October 29, 2024

CBO Analyzes Policy to Raise Social Security’s Retirement Age

Executive Summary

- Under current law, Social Security’s normal retirement age (NRA) is 67, though seniors can start claiming benefits at the early eligibility age of 62 or as late as age 70, with monthly Social Security benefits adjusted upward or downward based on the age at which benefits are initially claimed.

- In a recent letter, the Congressional Budget Office (CBO) analyzed the effects of increasing the NRA from 67 to 69 on seniors’ benefits and Social Security’s finances; it found that raising the NRA would reduce lifetime Social Security benefits for all beneficiaries affected by the policy change and slow Social Security spending, but it would not extend the life of the program’s trust funds.

- CBO’s analysis shows that raising the full retirement age is not enough on its own to meaningfully improve Social Security’s finances, support productive aging, or ensure strong economic growth; a combination of revenue and benefit changes will ultimately be needed.

Introduction

Under current law, Social Security’s normal retirement age (NRA) – also known as the full retirement age – is 67, though seniors can start claiming benefits at the early eligibility age (EEA) of 62 or as late as age 70, with monthly Social Security benefits adjusted upward or downward based on the age at which benefits are initially claimed.

The Congressional Budget Office’s (CBO) recent long-term Social Security projections estimated that the theoretically combined Social Security trust funds (Old-Age and Survivors Insurance and Disability Insurance) – which currently pay monthly benefits to 65 million retired workers, their spouses and children, and their survivors, as well as disabled workers – are projected to exhaust their reserves and become insolvent by the end of fiscal year (FY) 2034. That means the combined trust funds will run out when today’s 57-year-olds reach the NRA or 67 and today’s youngest retirees – those retiring at the EEA of 62 – turn 72. At that point, the law calls for an immediate 23-percent across-the-board benefit cut for all beneficiaries regardless of age, income, or need.

Restoring solvency to Social Security will likely require a combination of revenue and benefit changes. Raising the NRA is one of many possible reforms that should be on the table. In a recent letter, CBO analyzed the effects of raising the NRA from 67 to 69 on seniors’ benefits and Social Security’s finances. It found that increasing the NRA would reduce lifetime Social Security benefits for all beneficiaries affected by the policy change and slow Social Security spending, but it would not extend the life of the program’s trust funds. In addition, the policy change would not meaningfully improve Social Security’s finances, support productive aging, or ensure strong economic growth; a combination of revenue and benefit changes will ultimately be needed.

A Policy to Raise the Full Retirement Age

CBO analyzed the effects of a policy change that would gradually increase the NRA from 67 to 69. For workers born in 1965, the NRA would be 67 years and three months and would increase by three months per birth year until it reached 69 for workers born in 1972 and later. The EEA would remain at 62, while the age at which workers can delay claiming Social Security benefits would increase from 70 to 72. A worker’s reduction in benefits for claiming them more than three years in advance of their NRA would remain at 5 percent per year.

CBO found that workers claiming benefits before their NRA would see a larger reduction in their monthly benefits under the policy change than under current law. As an example, under current law, the monthly benefits for workers born in 1972 would be reduced by 30 percent if they claimed benefits at the EEA of 62 instead of their NRA of 72. Under the policy change, their benefits would be reduced by 40 percent if they claimed benefits at the EEA instead of the NRA of 69. Workers claiming benefits after their NRA would see a larger increase in their monthly benefits.

How Would Raising the Retirement Age Affect Workers’ Social Security Benefits?

CBO analyzed the effects that raising the NRA from 67 to 69 would have on Social Security retirement benefits by looking at the average annual benefits a worker would receive if they claimed benefits at age 65 and average lifetime Social Security benefits measured as a percentage of average lifetime earnings.

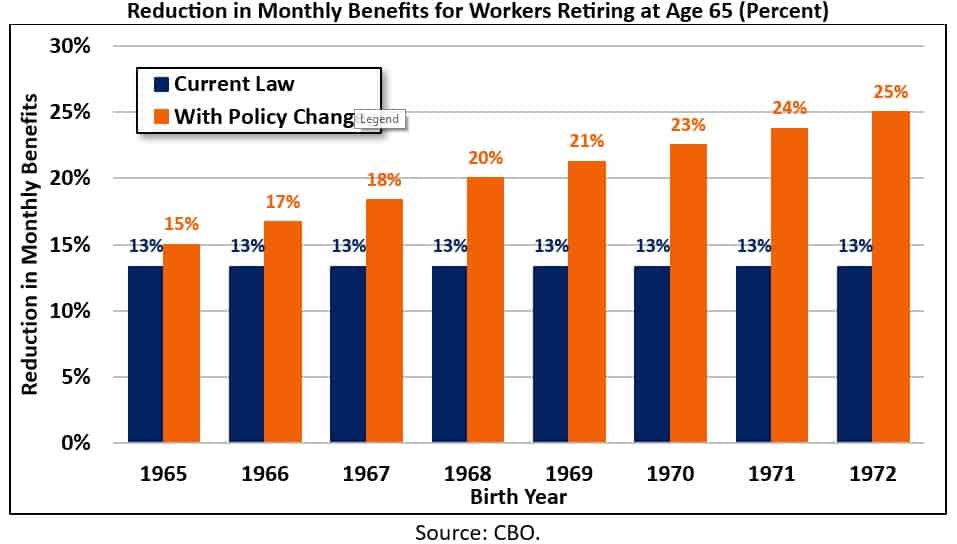

Workers born before 1965 would see no change in their Social Security benefits. Workers born in 1965 who claim benefits at age 65 (instead of their NRA of 67 years and three months) would receive monthly benefits that are 15 percent less than those they’d receive at their NRA. Workers born in 1972 who claim benefits at age 65 (instead of their NRA of 69) would receive monthly benefits that are 25 percent less than those they’d receive at their NRA.

For workers born in the 1960s (those aged 55 to 64 today) who claim benefits at age 65 instead of their NRA would receive average monthly Social Security benefits that are 3 percent lower with the higher full retirement age than under current law. The reduction in average monthly benefits reflects workers who would be unaffected by the policy change (those born before 1965) and workers who would be affected by the policy change (those born between 1965 and 1969). Workers born in the 1970s (those aged 45 to 54 today) and the 1980s (those aged 35 to 44 today) would each receive 13 percent less average monthly benefits than under current law. These effects would be similar for workers with different lifetime incomes as well as for men and women.

All workers born after 1965 would be affected by the policy change, and the total amount of Social Security benefits they would receive during their lifetimes would equal a smaller percentage of their lifetime earnings, on average, than under current law. For workers born in the 1960s, their average lifetime benefits would equal 12.5 percent of their average lifetime earnings, compared to 12.7 percent under current law – a 2-percent reduction. For those born in the 1970s, their lifetime benefits would equal 11.6 percent of their lifetime earnings, compared to 12.7 percent under current law – an 8-percent decrease. And for workers born in the 1980s, their lifetime benefits would equal 11.3 percent of their lifetime earnings, compared to 12.3 percent under current law – an-8 percent decline.

Workers at the high end of the lifetime earnings distribution would see a larger decline in their lifetime benefits than low-income earners. Men and women would see similar changes in their lifetime benefits.

Of note, CBO’s findings are subject to uncertainty; the agency notes that it is unclear how an increase in the NRA would impact workers’ decisions on when to claim Social Security benefits.

How Would Raising the Retirement Age Affect Social Security’s Finances?

Increasing the NRA from 67 to 69 would reduce Social Security spending and the program’s 75-year actuarial imbalance. Under current law, CBO projects that program spending will total 5.9 percent of gross domestic product (GDP) in 2054 and 6.7 percent of GDP in 2098. Raising the NRA from 67 to 69 would reduce Social Security spending to 5.4 percent of GDP in 2054 and 6.2 percent of GDP in 2098. Spending would fall because average benefits would be lower, and more workers would choose to claim benefits at the NRA rather than the EEA.

Under current law, CBO estimates that Social Security faces a 75-year actuarial imbalance of 1.5 percent of GDP, or 4.3 percent of taxable payroll. Raising the retirement age would reduce it to 1.1 percent of GDP, or 3.3 percent of taxable payroll. That’s a 24-percent reduction in Social Security’s 75-year actuarial imbalance as both a percentage of GDP and taxable payroll.

Raising the retirement age would not extend the solvency of the theoretically combined Social Security trust funds. Even with the policy change, the theoretically combined trust funds would still exhaust their reserves and become insolvent by the end of FY 2034 under CBO’s projections.

Conclusion

As CBO shows, raising Social Security’s full retirement age from 67 to 69 is not enough on its own to meaningfully improve the program’s finances, support productive aging, or ensure strong economic growth. While it is one possible policy solution, a combination of revenue and benefit changes will ultimately be needed to improve Social Security’s financial outlook.