Insight

March 6, 2026

CBO Projects Troubling Long-Term Budget Outlook

Executive Summary

- The Congressional Budget Office has released a new set of budget projections that show the long-term budget outlook has deteriorated since March 2025, largely due to higher spending and lower revenue projections.

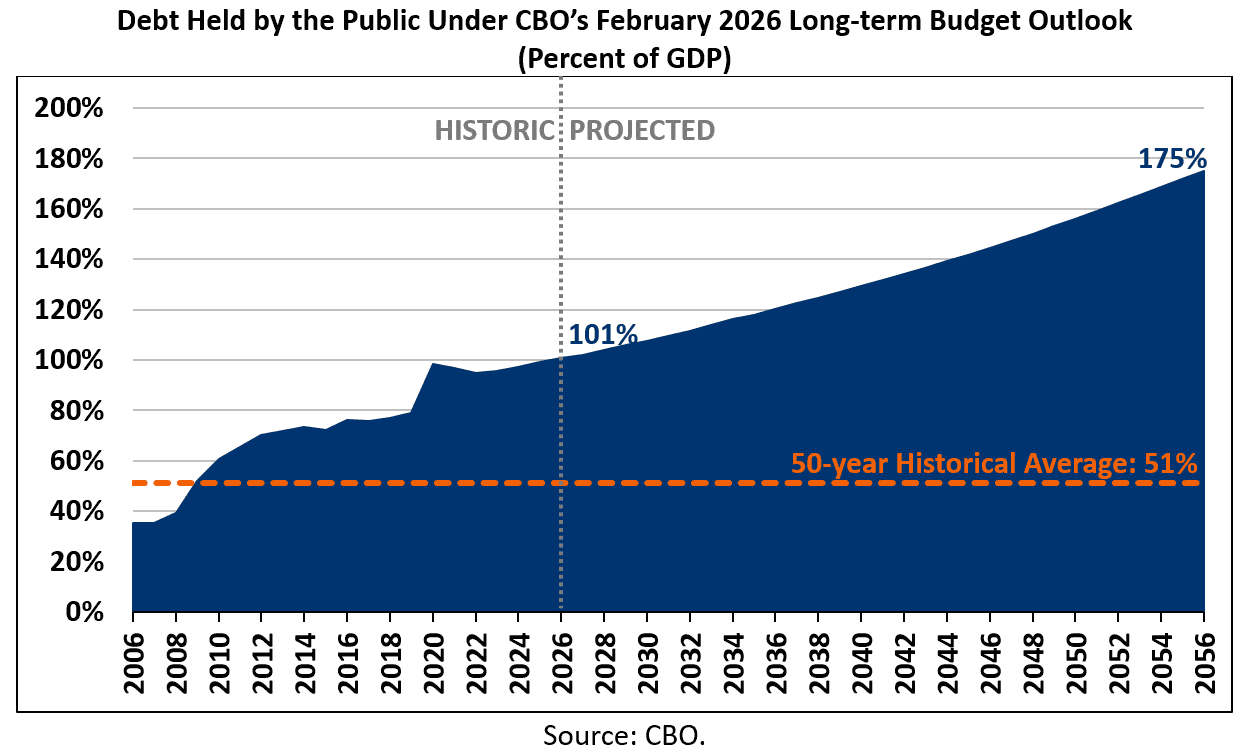

- It estimates federal debt held by the public will rise from 101 percent of gross domestic product (GDP) at the end of fiscal year (FY) 2026 to 175 percent of GDP by the end of FY 2056 under current law – more than three times the 50-year historical average; meanwhile, budget deficits will grow rapidly, increasing from 5.8 percent of GDP in FY 2026 to 9.1 percent of GDP in FY 2056 – more than twice the historical average.

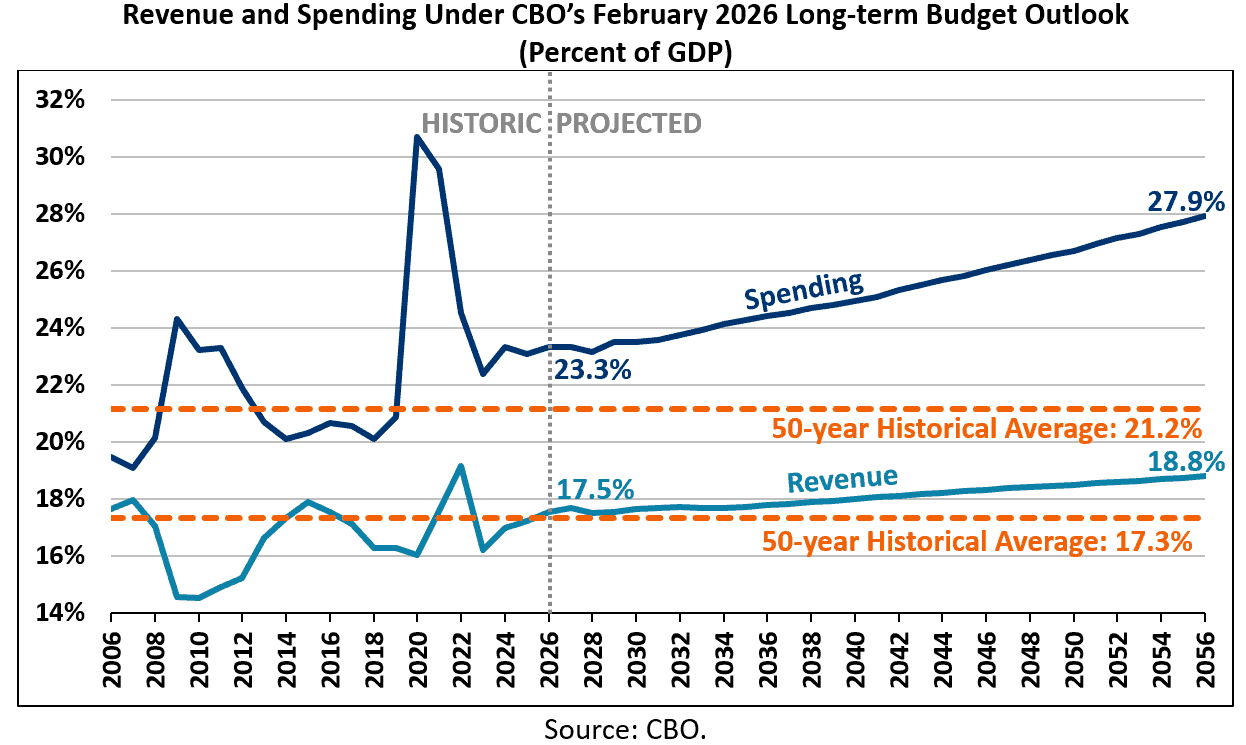

- Spending will continue to outpace revenue, rising from 23.3 percent of GDP in FY 2026 to 27.9 percent of GDP in FY 2056, while revenue will grow from 17.5 percent of GDP to 18.8 percent of GDP.

Introduction

The Congressional Budget Office (CBO) has released a new set of long-term budget projections that update is March 2025 Long-term Budget Outlook to account for subsequent legislation and executive actions and recent trends in economic growth, inflation, interest rates, demographics and other factors. Overall, CBO’s long-term budget outlook has deteriorated since March 2025, largely due to higher spending and lower revenue projections.

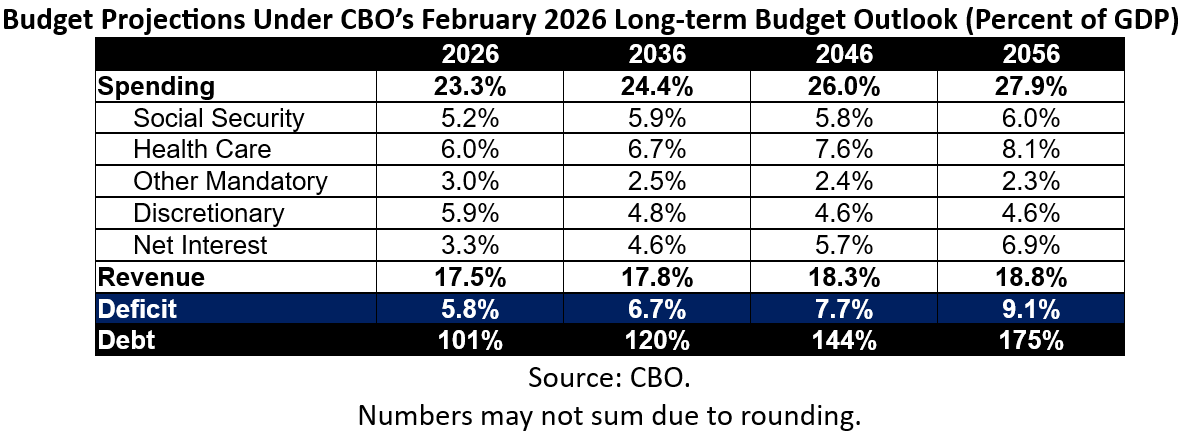

Specifically, CBO projects that spending will continue to outpace revenue, rising from 23.3 percent of GDP in FY 2026 to 27.9 percent of GDP in FY 2056. For comparison, the 50-year historical average for spending is 21.2 percent of GDP. Notably, CBO projects spending on net interest to eclipse spending on Social Security by FY 2048, making net interest the single-largest government expenditure. Revenue will grow from 17.5 percent of GDP to 18.8 percent of GDP. The 50-year historical average for revenue is 17.3 percent of GDP.

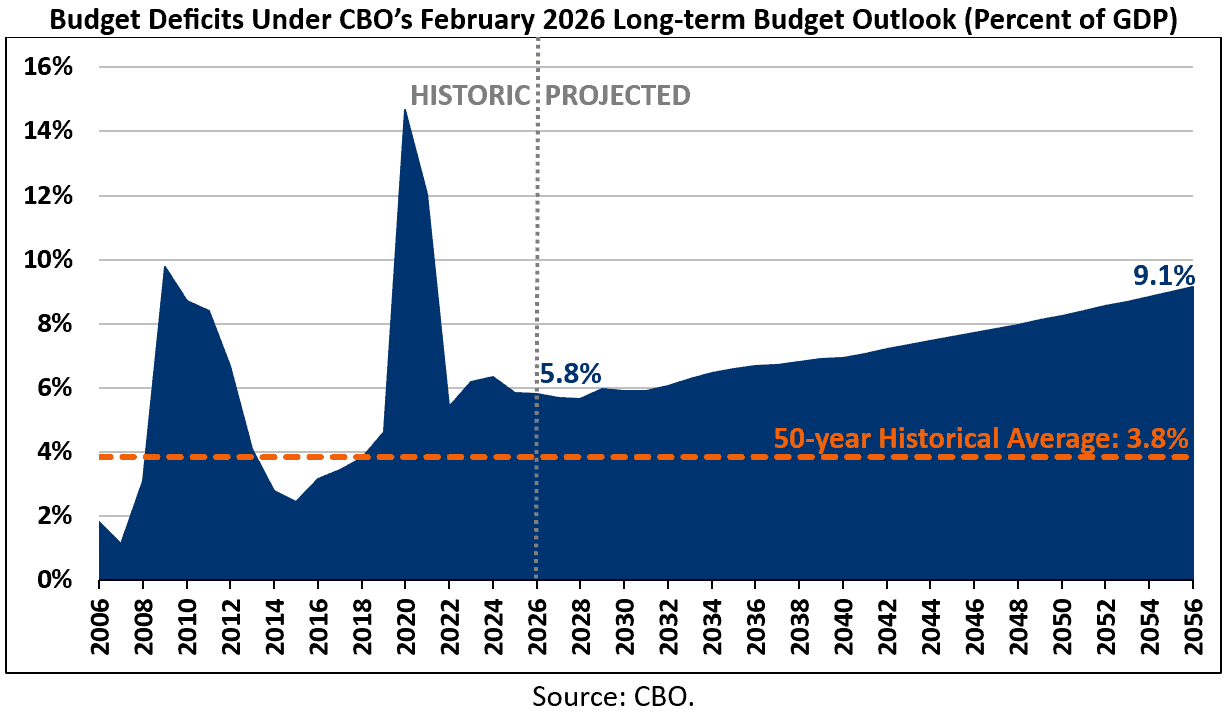

CBO projects budget deficits to grow rapidly, increasing from 5.8 percent of GDP in FY 2026 to 9.1 percent of GDP in FY 2056 – more than twice the historical average of 3.8 percent of GDP, and higher than at any time in modern history outside of World War II, the Great Recession, and the COVID-19 pandemic.

Finally, CBO estimates federal debt held by the public will rise from 101 percent of GDP at the end of FY 2026 to 175 percent of GDP by the end of FY 2056 under current law – more than three times the 50-year historical average.

The Long-term Budget Outlook by the Numbers

Revenue

CBO projects that total federal revenue collections will rise from 17.5 percent of GDP ($5.6 trillion) in FY 2026 to 17.8 percent of GDP ($8.3 trillion) in FY 2036, 18.3 percent of GDP ($12.4 trillion) in FY 2046, and 18.8 percent of GDP ($18.0 trillion) in FY 2056. For comparison, the 50-year historical average for revenue is 17.3 percent of GDP.

Spending

CBO projects that total federal spending will rise from 23.3 percent of GDP ($7.4 trillion) in FY 2026 to 24.4 percent of GDP ($11.4 trillion) in FY 2036, 26.0 percent of GDP ($17.6 trillion) in FY 2046, and 27.9 percent of GDP ($26.7 trillion) in FY 2056. For comparison, the 50-year historical average for spending is 21.2 percent of GDP.

The projected growth in long-term spending is driven by rising interest payments on the national debt and growing Social Security and health care spending. CBO estimates that interest costs will increase substantially over the next three decades, growing from 3.3 percent of GDP ($1.0 trillion) in FY 2026 to 6.9 percent of GDP ($6.6 trillion) by FY 2056. Meanwhile, spending on Social Security and the major health care programs (Medicare, Medicaid, the Children’s Health Insurance Program, and Affordable Care Act premium tax credits) will grow from 11.2 percent of GDP ($3.6 trillion) in FY 2026 to 14.1 percent of GDP ($13.5 trillion) by FY 2026. Other spending, including smaller mandatory programs and defense and nondefense discretionary programs, will fall as a share of the economy, from 6.9 percent of GDP in FY 2026 to 7.0 percent of GDP by FY 2056.

Net interest will eclipse spending on Social Security by FY 2048, making net interest the single-largest government expenditure.

Deficits

CBO projects that the budget deficit will grow from 5.8 percent of GDP ($1.9 trillion) in FY 2026 to 6.7 percent of GDP ($3.1 trillion) in FY 2036, 7.7 percent of GDP ($5.2 trillion) in FY 2046, and 9.1 percent of GDP ($8.7 trillion) in FY 2056. For comparison, the budget deficit has averaged 3.8 percent of GDP over the past 50 years.

At 9.1 percent of GDP, the deficit in FY 2056 will be more than twice the 50-year average and higher than at any time in modern history outside of World War II, the Great Recession, and the COVID-19 pandemic.

Debt

CBO projects that federal debt held by the public will rise from 101 percent of GDP at the end of FY 2026 to a new record of 108 percent of GDP by the end of FY 2030. It will continue to rise to 120 percent of GDP by the end of FY 2036, 144 percent of GDP by the end of FY 2046, and 175 percent of GDP by the end of FY 2056. For comparison, debt held by the public has averaged 51 percent of GDP over the past 50 years, so debt-to-GDP in FY 2056 will be more than three-times the historical average. Between FY 2026 and 2056, debt will increase by $135.4 trillion, from $32.1 trillion to $167.5 trillion.

Trust Funds

CBO projects that the Highway Trust Fund will exhaust its reserves by FY 2028, the Social Security Old-Age and Survivors Insurance trust fund by FY 2032, and the Medicare Hospital Insurance trust fund by FY 2040. The Social Security Disability Insurance trust fund will remain solvent at least through FY 2056.

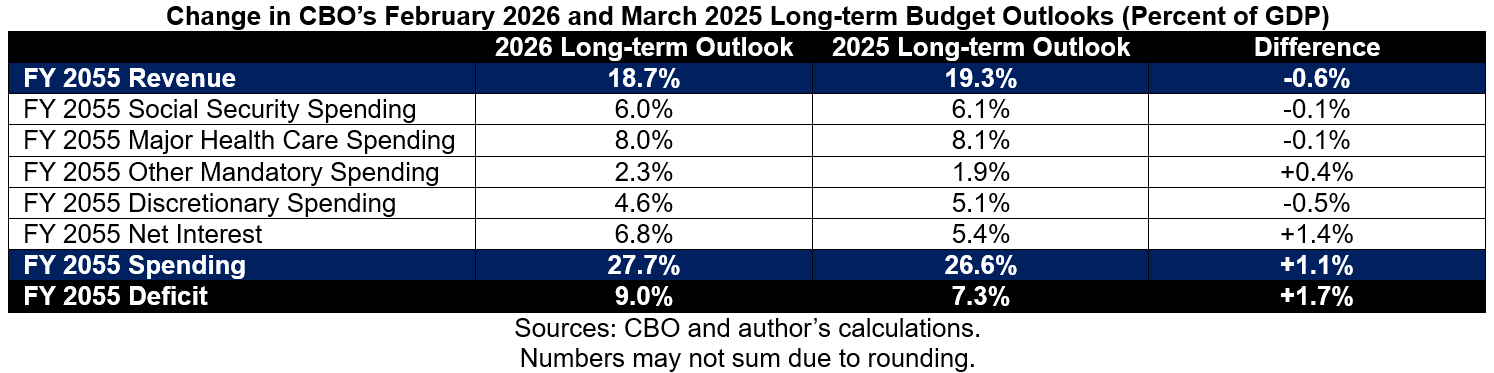

What’s Changed?

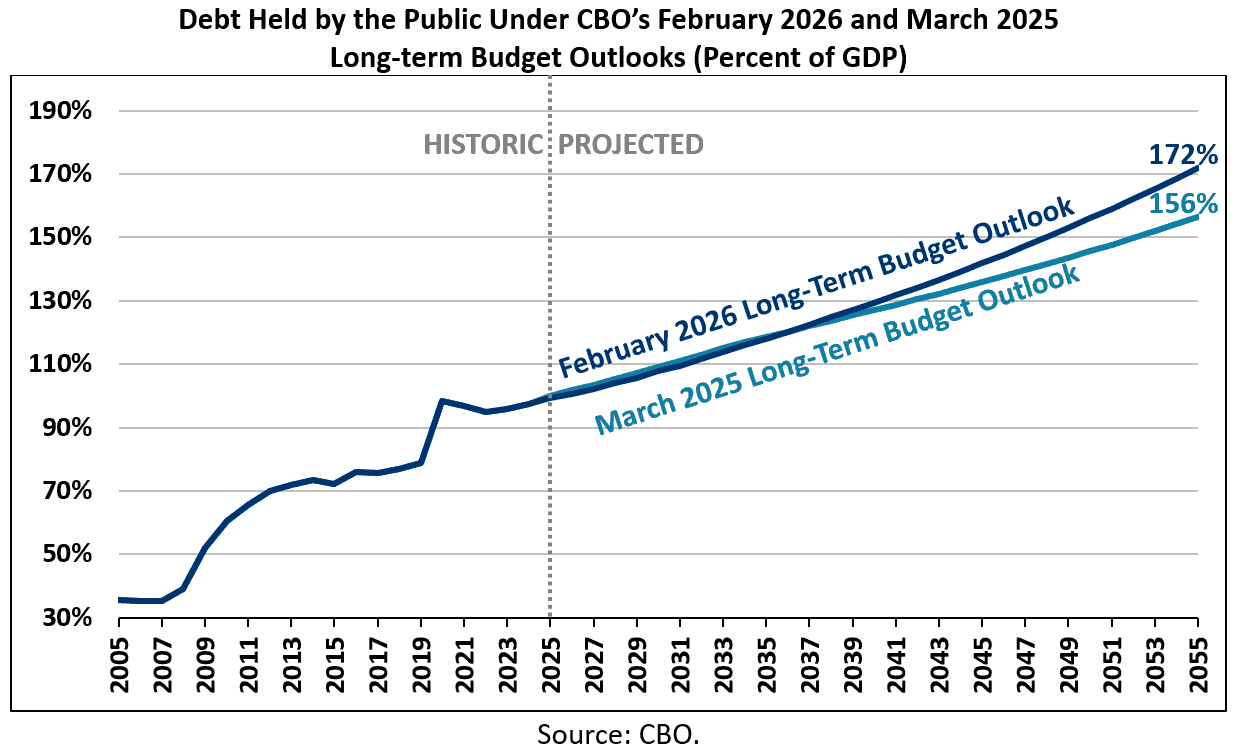

The long-term budget outlook has deteriorated since CBO’s March 2025 Long-term Budget Outlook. CBO now projects the budget deficit to grow to 9.0 percent of GDP by the end of FY 2055, which is 1.7 percentage points of GDP above its March projection of 7.3 percent of GDP. Meanwhile, federal debt held by the public is projected to rise to 172 percent of GDP by the end of FY 2055, 16 percentage points of GDP above the 156 percent of GDP that CBO projected in March.

CBO’s higher projections of long-term deficits and debt are largely due to a combination of higher spending and lower revenue projections. CBO estimates that in FY 2055 spending will be 1.1 percentage points of GDP higher and revenue 0.6 percentage points of GDP lower. The higher spending projection is driven by a 0.4 percentage point of GDP increase in other mandatory spending and a 1.4 percentage point of GDP increase in net interest payments. These figures are slightly offset by a 0.5 percentage point of GDP decrease in projected discretionary spending, and a 0.1 percentage point of GDP decrease each in projected Social Security and health care spending.