Insight

December 7, 2017

Continuing Resolutions, the Budget Control Act, and the Outlook for Discretionary Spending

Executive Summary

- Funding the federal government at FY2017 levels would trigger a $4.8 billion sequester in January

- A comprehensive budget agreement remains elusive

- Simply allowing overall discretionary spending to rise to “pre-sequestration” levels would cost $91.2 billion in FY2018

Introduction

For the past four fiscal years, discretionary spending levels – the roughly one-third of federal spending controlled by Congress on an annual basis – have been set by two-year budget agreements that have provided relief against spending reductions imposed by the 2011 Budget Control Act (BCA). No such budget agreement is in place for FY2018, however, meaning that discretionary spending levels must adhere to the BCA’s lower spending. Instead, Congress has continued to fund the federal government through continuing resolutions (CRs) that essentially extend FY2017 spending levels, which are higher than allowed under the BCA, into FY2018. Any spending over the law’s limits will face sequestration in January unless Congress modifies the law. This paper identifies the interaction between current spending levels and the BCA, and provides an update on the outlook for discretionary spending in FY2018.

Continuing Resolutions

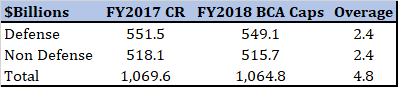

Congress has been unable to reach a discretionary spending agreement for FY2018 and, as a result, has funded the executive agencies through a CR, set to expire on December 9th. Congress will likely extend this funding through December 22nd and then again into next year. These CRs have essentially maintained funding levels enacted in FY2017. However, the spending caps set forth in the BCA for FY2018 are lower than those established for FY2017. Accordingly, merely extending FY2017 funding levels into next year would, all else being equal, precipitate a sequester of $4.8 billion – the amount by which the FY2017 funding levels, if continued into FY2018 through CRs, will exceed the FY2018 BCA caps.[1]

Table 1: FY 2017 Funding vs. FY2018 BCA Caps

This potential sequester will need to be addressed – either by reducing the funding in the CR itself or amending the BCA to accommodate this small increase – in the continuing resolution that Congress is likely to enact to maintain funding into next calendar year.

Amending the Budget Control Act

When the BCA was enacted, it imposed discretionary spending caps and required Congress to form a bipartisan committee (the Joint Select Committee on Deficit Reduction or “Super Committee”) to achieve a further $1.2 trillion in deficit savings. When this committee failed to deliver, a fallback mechanism in the BCA reduced the original discretionary spending caps even further to the current levels (see Table 2 below). All of the subsequent budget agreements have restored some, but not all, of the funding reduced by this fallback mechanism. Table 2 identifies the amount by which the FY2018 caps were reduced as a result of the Super Committee’s failure. Simply restoring these spending levels to the levels originally set forth in the BCA (before the Super Committee’s failure) would cost $91.2 billion in FY2018.

Table 2: BCA Caps for FY2018 Before and After Sequestration

Congress has largely been unable to amend the BCA except in the context of multi-year budget agreements that provide relief against the BCA caps. The primary sticking points between Republicans and Democrats in these agreements have been the ratio of defense and non-defense increases and budgetary offsets to the increases. President Obama and congressional Democrats had previously insisted on a dollar-for-dollar match for defense and non-defense discretionary spending above the original BCA caps.

President Trump pledged to increase defense funding during his campaign, a commitment reflected in the administration’s FY2018 Budget.[2] The House and Senate have also passed, and the president signed, the National Defense Authorization Act for Fiscal Year 2018 (NDAA) that authorizes a base defense funding level of $626.4 billion for FY2018 – $77.3 billion above the $549.1 billion defense cap set forth by the BCA and above even the original BCA cap.[3] However, the NDAA merely authorizes this level of spending – it does not change the BCA caps – meaning that if Congress were to appropriate this level of funding without amending the BCA to accommodate the increase, the entire $77.3 billion in higher funding would be canceled through sequestration.

The president’s budget assumes significantly reduced non-defense discretionary spending levels in addition to the defense increases, which would likely be impossible to enact over Democratic opposition in the Senate. Congressional Democrats, particularly in the Senate, are unwilling to allow an increase in the BCA caps to accommodate higher defense spending without a related increase in non-defense discretionary spending. Accordingly, any budget agreement that sought to increase defense spending levels would not only discard these proposed non-defense spending reductions, but would almost certainly include non-defense discretionary spending increases. Moreover, Congress has not identified or agreed upon offsets to accommodate the increased spending.

Conclusion

A comprehensive budget agreement making good on the president’s commitment to increase defense funding remains elusive. Congress has been content to fund the executive agencies with short-term CRs at FY2017 spending levels, yet even this incremental approach cannot continue without consequence as the CRs provide more funding than current law allows for FY2018. Ultimately, Congress will need to provide stable and adequate funding for the national defense and other federal functions. The current approach is unsustainable.

[1] https://www.cbo.gov/system/files/115th-congress-2017-2018/costestimate/hr601asenacted.pdf

[2] For a more complete assessment of the outlook on defense funding, see: https://www.americanactionforum.org/research/outlook-defense-spending-fy2018/

[3] http://docs.house.gov/billsthisweek/20171113/HRPT-115-HR2810.pdf