Insight

June 15, 2026

High Jet Fuel Premium Changing U.S. Refiners’ Priority

Executive Summary

- The closure of the Strait of Hormuz for over 100 days has disrupted 20 percent of global petroleum supply, driving up U.S. Gulf Coast jet fuel spot prices by 110 percent year over year by mid-May 2026, while U.S. gasoline prices rose 40 percent over the same period.

- In response to this increased premium on jet fuel relative to gasoline, U.S. refiners have adjusted their refining processes to maximize jet fuel production to capture the high margins.

- If the recently announced U.S.-Iran agreement leads to a near-term reopening of the strait, it would allow Persian Gulf petroleum exports to resume and stabilize global markets; alternatively, an extended closure will keep crude oil high, prompting U.S. refiners to continue prioritizing high-margin jet fuel exports to Europe and Asia.

Introduction

Since the start of the Iran conflict, the de facto closure of the Strait of Hormuz for over 100 days has disrupted 20 percent of global petroleum supply, triggering massive price spikes across petroleum products; this energy shock drove up U.S. Gulf Coast jet fuel spot prices by 110 percent year over year by mid-May 2026, while U.S. gasoline prices rose 40 percent over the same period.

Since the U.S. refiners have developed to produce more gasoline than jet fuel, the sudden supply constraints have disproportionately pushed up jet fuel refining margins. U.S. jet fuel crack spread (a measure of the profitability of a petroleum product) surged to a peak of $74 per barrel in March, exceeding gasoline by more than $40 per barrel. In response, U.S. refiners have adjusted their refining processes to maximize jet fuel production and increased output to over 2 million barrels per day.

As the U.S. domestic jet fuel supply climbed above average, the additional supply of jet fuel was mostly exported to Asia and Europe to mitigate the severe shortages. This shift has also created a temporary domestic surplus of gasoline components, as refining crude oil into jet fuel inevitably yields gasoline as a byproduct. The glut of gasoline components does not necessarily lead to lower gas prices at the pump, however, as refiners are constrained by available capacity to blend them into motor gasoline.

On June 14, 2026, President Trump announced that the United States has reached an initial deal with Iran to end the Middle East conflict. As of the publication date, the official signing of the deal is scheduled for June 19 in Switzerland. Official details of the agreement have yet to be released, and it’s unclear whether the deal will lead to the full reopening of the Strait of Hormuz.

The future trajectory of U.S. jet fuel and gasoline prices and refining margins will largely depend on the duration of the Middle East conflict and shifting consumer demand. A near-term reopening of the strait will allow Persian Gulf exports to resume and stabilize global markets, whereas an extended closure will keep crude oil high, prompting U.S. refiners to continue prioritizing high-margin jet fuel exports to Europe and Asia.

The Global Oil Disruption

The Strait of Hormuz, a global oil chokepoint, has been effectively closed for more than 100 days since the start of the Iran conflict. The closure of the strait has disrupted about 20 percent of global petroleum consumption at 20 million barrels per day (mbd) shipping from major Persian Gulf oil producing countries to the rest of the world. A previous American Action Forum (AAF) insight provided an analysis of the global energy shock and its short- and long-term implications.

The global oil disruption has led to spikes in prices of crude oil, which in turn are pushing up prices of petroleum products such as jet fuel and gasoline. Brent—a global oil price benchmark—is expected to stay at about $105 per barrel in June and July, compared to the price point around $70 a barrel prior to the Iran conflict.

Despite the unprecedented global energy disruption, crude oil prices have not (so far) skyrocketed as expected by many experts. This relative restraint is due to driven several factors as explained in this AAF analysis, including workarounds via bypass oil pipelines through Saudi Arabia and the United Arab Emirates, reduction in global demand, and drawdowns of global oil inventories. Additionally, the U.S. military has been escorting some ships through the strait recently, allowing about 100 million barrels of oil to reach the global market. Most important, China, as a top global oil consumer, has been slashing its oil imports by at least 30 percent since May, which provides a substantial buffer for the global oil market.

On June 14, 2026, President Trump announced that the United States has reached an initial deal with Iran to end the Middle East conflict. As of the publication date, the official signing of the deal is scheduled for June 19. President Trump noted in his announcement that “I hereby fully authorize the toll free opening of the Strait of Hormuz, and, simultaneously herewith, authorize the immediate removal of the United States Naval blockade.” Official details of the agreement have not been released, and it’s unclear whether the deal will lead to the full reopening of the Strait of Hormuz in the near term.

U.S. Refineries Are Producing More Jet Fuel To Capture Higher Margins

Higher crude oil prices are pushing up prices of jet fuels and gasoline

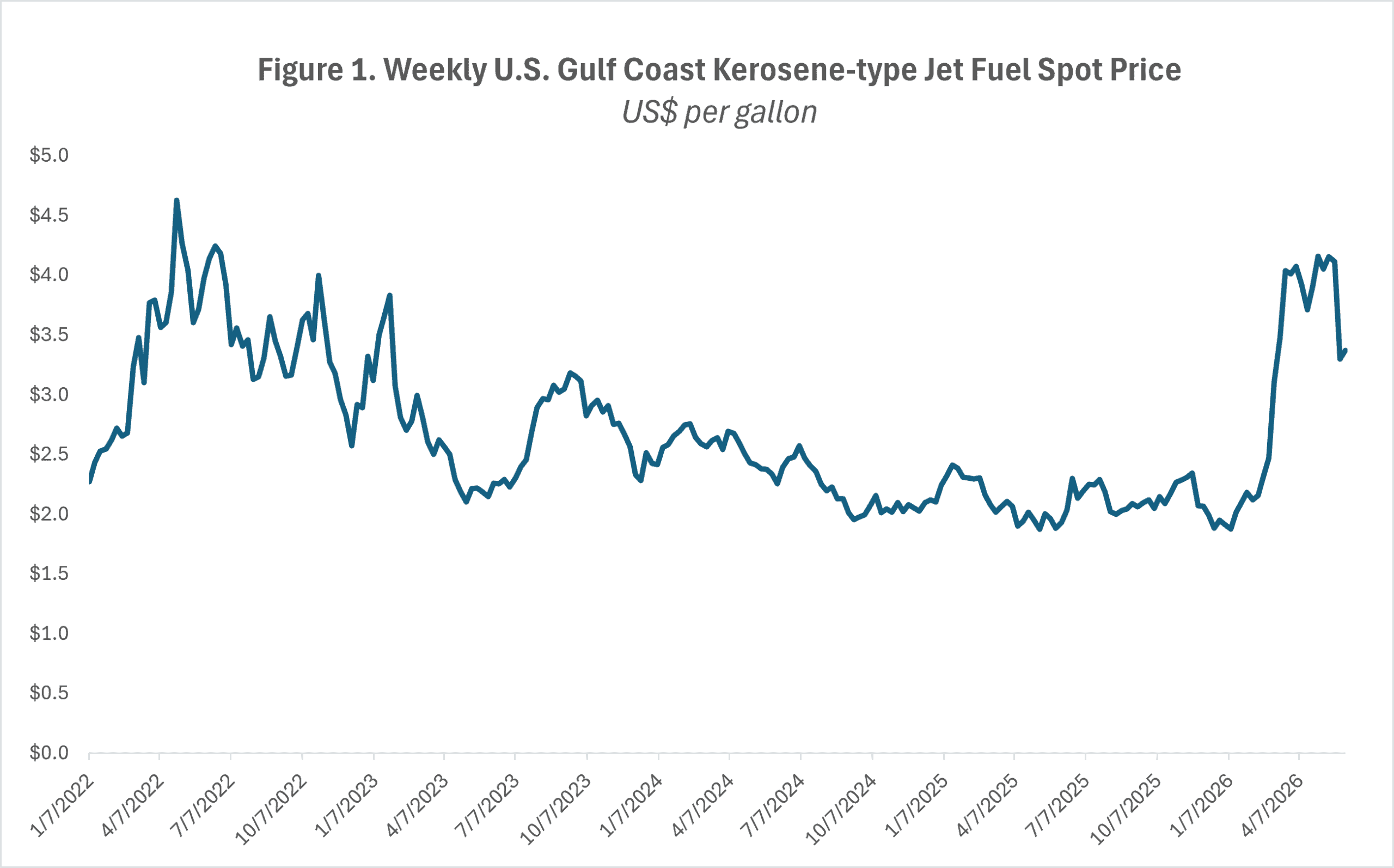

As shown in Figure 1, U.S. Gulf Coast jet fuel spot prices increased by 82 percent from an average of $2.30 per gallon in the week of February 20 (before the Iran conflict) to as high as $4.20 per gallon in the week of May 15. Comparing the same week of May 15 in 2025 and 2026, U.S. Gulf Coast jet fuel spot prices more than doubled this year, rising by 110 percent.

Prices have come down to about $3.40 per gallon in the week of June 5 (discussion below). Driven by the conflict with Iran, the peak jet fuel spot price of $4.20 per gallon nearly matched the historic high of $4.60 per gallon seen in 2022, when Russia’s invasion of Ukraine triggered a massive global energy shock.

Source: Energy Information Administration

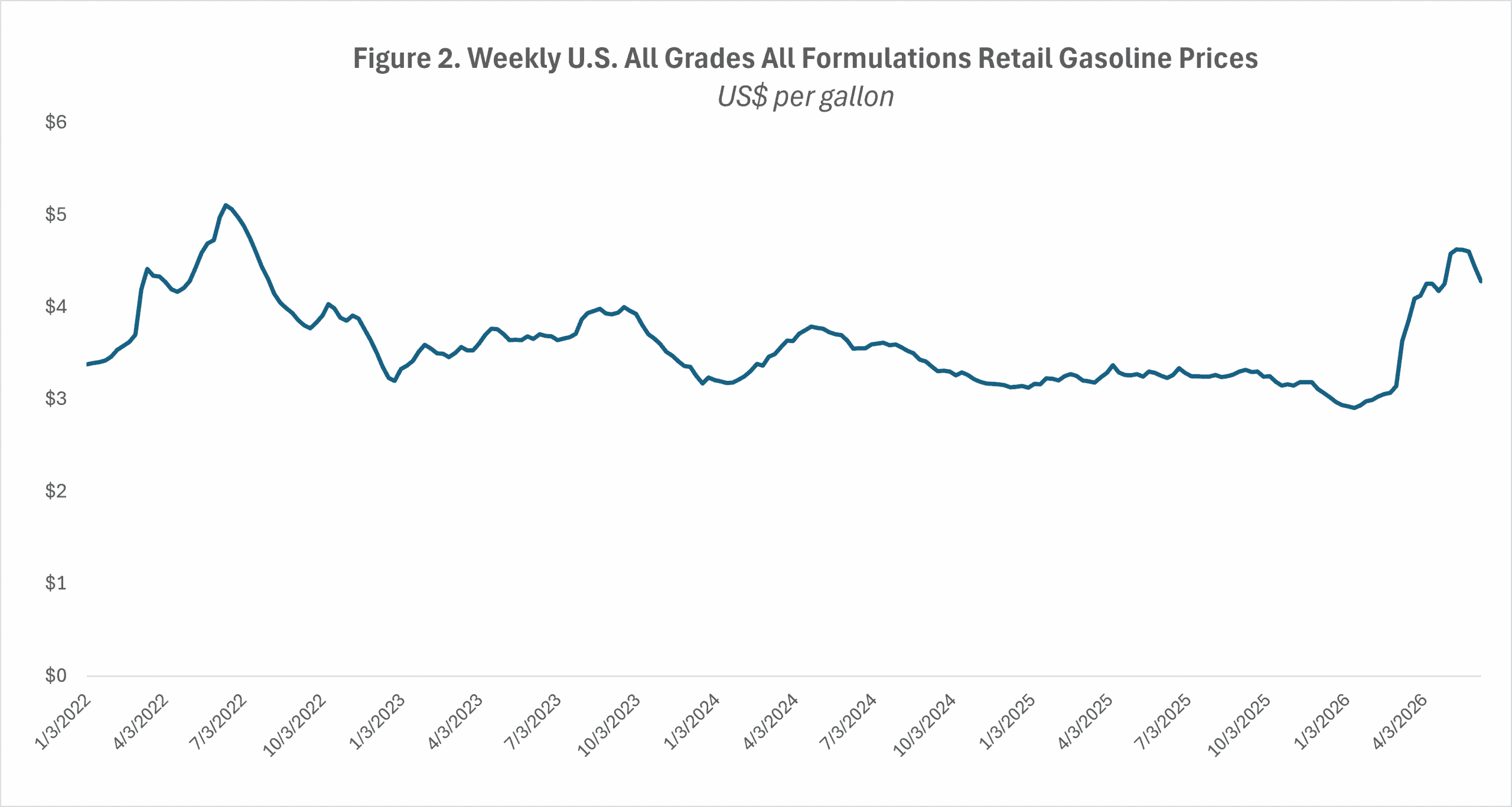

U.S. average retail gasoline prices rose to as high as $4.60 per gallon in May 2026, and decreased slightly to an average of $4.30 per gallon in the beginning of June (Figure 2). This was about a 40-percent increase from May 2025 to May 2026. The spikes in U.S. gasoline prices following the Iran conflict almost reached the historic high levels of about $5.00 per gallon in June 2022 after Russia invaded Ukraine.

Source: Energy Information Administration (EIA)

U.S. refiners are maximizing jet fuel production to capture higher margins

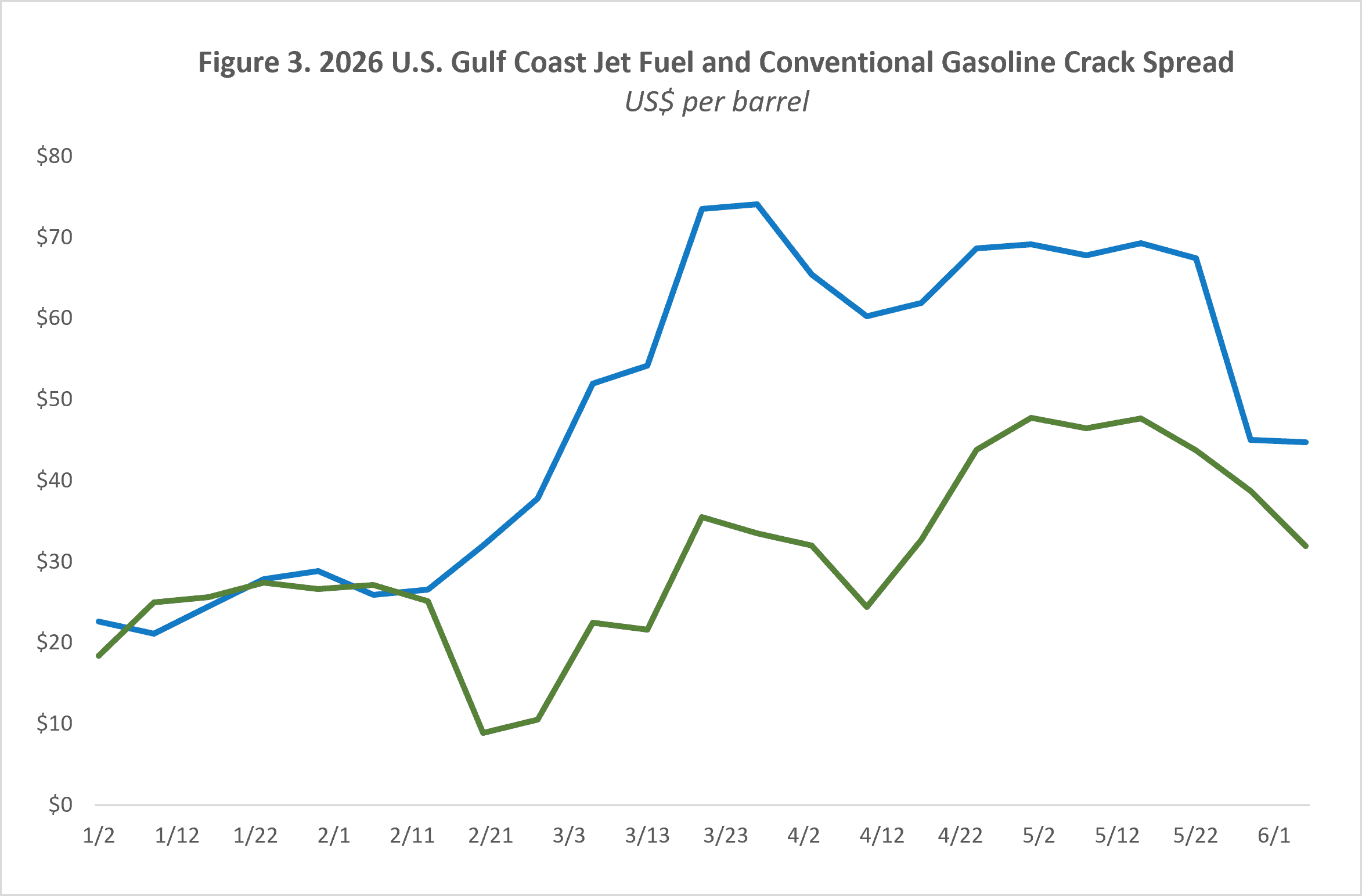

In the oil industry, crack spread is the price difference between a barrel of crude oil and the refined petroleum products (gasoline, jet fuel, or diesel) it can yield. It is an important indicator of a refinery’s profitability measure. Typically, three barrels of U.S. crude oil can yield two barrels of gasoline and one barrel of distillate (jet fuel or diesel). This is called the 3:2:1 crack spread. Since U.S. refining has developed to produce more gasoline than jet fuel, the sudden supply constraints have disproportionately pushed up jet fuel refining margins.

As shown in Figure 3, U.S. Gulf Coast jet fuel crack spread closely tracked the gasoline crack spread prior to the outbreak of the Iran conflict. Following the escalation, however, jet fuel prices far outpaced gasoline prices between March and May. The jet fuel crack spread surged to a peak of $74 per barrel in March, contrasting sharply with gasoline margins, which reached as high as $35 per barrel in the same month. By the week of March 27, the jet fuel crack spread exceeded that of gasoline by more than $40 per barrel, highlighting the substantially higher profitability of aviation fuel production relative to motor gasoline.

Source: EIA, author’s analysis.

In response to the jet fuel’s higher prices and profit margins, U.S. refiners have been maximizing their jet fuel production to capture the additional profits. U.S. jet fuel production increased from an average of 1.7 million barrels per day in February to over 2 million barrels per day in the week ending May 1.

To yield more jet fuel from a barrel of crude oil, refiners adjust the refining process in a way that produces more naphtha. Since it is not possible to yield jet fuel from a barrel of crude oil without producing some amount of naphtha, increased jet fuel production inherently increases the supply of this gasoline component in the U.S. market. This glut does not necessarily lead to lower gasoline pump prices, however, as refiners face capacity limits that prevent them from being blended into motor gasoline.

Most of the additional U.S. jet fuel production was exported to foreign markets – including Europe and Asia – as U.S. inventories were 7 percent higher than the 2021– 2025 average.

Additionally, jet fuel prices were traded at higher levels in March and April compared to U.S. Gulf Coast prices due to the significant fuel shortage in Europe and Asia as they relied heavily on jet fuel exports from the Gulf region prior to the Iran conflict.

By the end of May, as shown in Figure 3, U.S. jet fuel and gasoline’s crack spreads dropped drastically and their difference narrowed. This is mostly driven by the increased supply from U.S. refiners’ increased production and a reduction in demand. As concerns of a looming jet fuel shortage have eased, U.S. jet fuel prices have fallen in early June, as shown in Figure 1.

Looking Forward

Going forward, the trajectory of U.S. gasoline and jet fuel prices as well as their respective crack spreads will largely depend on the duration of the Middle East conflict and shifting consumer demand.

If the strait is reopened over the next few weeks following the signing of the U.S.-Iran agreement, big oil producing countries in the Persian Gulf region would slowly resume exports to the global oil market, eventually leading to lower U.S. gasoline and jet fuel prices. Refining margins of the two fuels will converge as the market recalibrates. Conversely, if the strait remains closed for several more months, persistent global supply constraints will drive crude oil higher, pushing U.S. jet fuel and gasoline prices up. Under this extended disruption, U.S. refiners will continue to chase high-margin jet fuel export pull from Europe and Asia while managing an accumulating surplus of domestic gasoline components.