Insight

April 4, 2018

Rediscovering Rescissions

Executive Summary

- Under what is known as the rescission process, the president may temporarily withhold, or impound, funding for discretionary spending programs, and submit to Congress a request to cancel funding for those programs.

- If Congress chooses to act on the president’s rescission request, it considers the spending cuts under expedited, or filibuster-proof procedures.

- If Congress does not act within 45 days of continuous session the president must spend the impounded funds.

- Since 1974, the president has proposed 1,178 rescissions, totaling $76,022,349,690. Of these, Congress has accepted 461, totaling $25,006,704,717.

- The process has not been used since FY2000.

When President Trump signed the Consolidated Appropriations Act of 2018, he called on Congress to provide him with the line-item veto. Presumably, President Trump was referring to the same authority that Congress provided to President Clinton under the Line-Item Veto Act of 1996, which granted the president the authority to cancel new discretionary spending, new direct spending, and new “limited tax benefits.” [1] The Supreme Court ruled that the Line-Item Veto Act was unconstitutional. However, current law enshrined in the Congressional Budget and Impoundment Control Act of 1974, already provides the executive branch with limited authority to temporarily suspend, or “impound,” discretionary spending, and subject to the approval of Congress, permanently cancel that spending. This process, known as rescission, was a fairly common occurrence throughout the 70s, 80s, and 90s, but has not been employed formally since FY2000. News reports suggest the Trump Administration may be considering sending a rescission request to Congress. Rescissions could play a role in more meaningfully engaging the executive and legislative branches in a public debate on the nation’s budget priorities but are inadequate to meaningfully address the nation’s mounting fiscal challenges. Moreover, if employed to undermine tenuous political comprises, it could worsen rather than improve the environment for meaningful fiscal reforms.

Rescission Authority

The Congressional Budget and Impoundment Control Act of 1974 (hereinafter referred to as the Budget Act) set forth the modern federal budget process, including those procedures used to develop the president’s budget request, the congressional budget process, and the process of budget execution whereby the executive branch apportions and spends the funding provided to it by Congress. The Budget Act reflects the primacy of the Congress in establishing the fiscal policy of the United States and was borne out of mounting tension between the legislative and executive branches of government that culminated during the Nixon Administration. President Nixon sought to expand the use of impoundment, or the withholding of appropriated funds, to include certain domestic programs.[2] Congress enacted the Budget Act which, among other provisions, imposed new restrictions on the president’s authority to impound appropriated funds.

Currently, the president has two forms of impoundment authority in statute: deferrals, or temporary impoundments, and rescissions, which are permanent cancellations of budget authority. The deferral authority granted by the Budget Act has been circumscribed by the courts and is not the focus of this analysis. Rescissions, on the other hand, remain a viable means for the executive branch to impound, and with the concurrence of Congress, permanently cancel discretionary spending.

Rescission Process for the Executive Branch

Under current law, the president may propose the impoundment of budget authority if he or she determines that the funding is not necessary to carry out the intended purpose of the program for which it is provided or simply if the president believes the cancellation would be sound fiscal policy. Upon that determination, the president may impound that budget authority and must submit to Congress a special message that includes:

- the amount of budget authority which the president proposes to be rescinded or which is to be so reserved;

- any account, department, or establishment of the government to which such budget authority is available for obligation, and the specific project or governmental functions involved;

- the reasons why the budget authority should be rescinded or is to be so reserved;

- to the maximum extent practicable, the estimated fiscal, economic, and budgetary effect of the proposed rescission or of the reservation; and

- all facts, circumstances, and considerations relating to or bearing upon the proposed rescission or the reservation and the decision to affect the proposed rescission or the reservation, and to the maximum extent practicable, the estimated effect of the proposed rescission or the reservation upon the objects, purposes, and programs for which the budget authority is provided.[3]

If Congress takes no action within 45 days of continuous session, the president must make the impounded funds available for obligation.[4]

Consideration of a Rescission Request in Congress

Upon receipt of a special message from the executive branch, Congress may consider a rescission bill, which rescinds in whole or in part the budget authority that the president requests. This rescission bill is referred to the appropriate committee, such as the Committee on Appropriations. If after 25 days, the relevant committee has not reported the rescission bill to the floor of the respective house of Congress, members may enter a motion to discharge the bill from the relevant committee if one-fifth of the members of the respective house of Congress support the motion. The rescission bill also receives expedited consideration on the floor of both the House and the Senate.[5] It is important to note, debate of a rescission bill in the Senate is limited to 10 hours, meaning it cannot be filibustered.

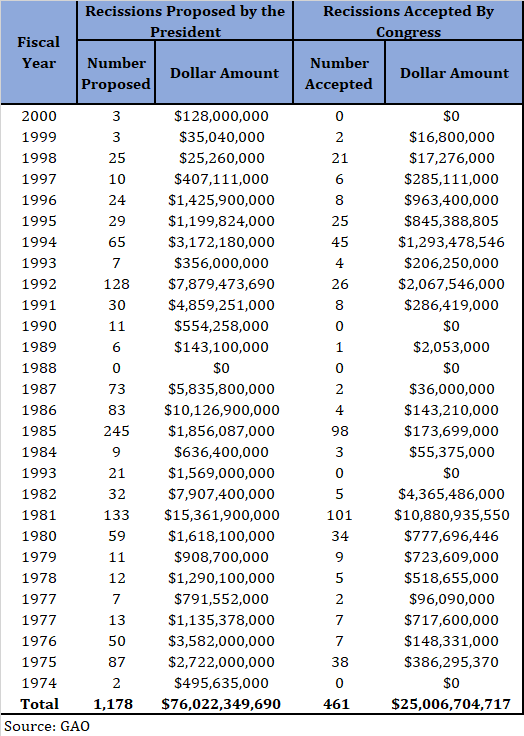

Historical Use of Rescission Authority

Since 1974, the president has proposed 1,178 rescissions, totaling $76,022,349,690. Of these, Congress has accepted 461, totaling $25,006,704,717.

However, no president since Clinton, who proposed three rescissions in FY2000, has proposed a formal rescission package to Congress. The highest number of rescission requests in a single year occurred during the Reagan Administration in FY1985, with 245, while the lowest number of rescission requests (prior to the abandonment of the process after FY2000) also occurred under President Reagan in FY1988, when there were no requests. Other than in FY1988, there has been at least two rescission requests per fiscal year since 1974 and prior to FY2001.

Conclusion

The rescission process is an underutilized budget process tool that has the virtue of engaging the legislative and executive branches in addressing the national fisc. To a large degree, these branches of government do not routinely grapple, either in opposition or jointly, with fiscal policy matters beyond annual spending bills. Rescission authority is confined to the funding contained within these discretionary spending bills, so it is not an expansive budgetary tool, and its capacity to fundamentally alter the nation’s fiscal outlook should not be overstated.

[1] President Clinton exercised it 82 times to cancel outlays and limited tax benefits of an estimated $937 million over the period 1998-2002. Congress and lower courts reversed $368 million in cancellations before the Act was overturned completely.

[2] For more history, see McMurtry, Virginia A. “Item Veto and Expanded Impoundment Proposals: History and Current Status,” Congressional Research Service, RL33635, June 18, 2010

[4] This definition excludes recesses for longer than 3 days and can in practice amount t0 60 or more calendar days. See McMurty, Op. Cit. pg. 3

[5] 2 U.S. Code § 688 – Procedure in House of Representatives and Senate