Insight

March 8, 2017

On Regulatory Reform, the Big Rules Move the Administrative State

Since 2009, regulators have published roughly $900 billion in long-term regulatory costs. During that time, there have been 700 major rules. However, not every major rule is created equal. Year after year, it’s the high-impact or billion-dollar rules that drive the regulatory state. In a typical year, the three largest rules can impose the vast majority of regulatory burdens. Enacting regulatory reform that addresses just a handful of the largest measures can go a long way toward trimming a substantial portion of all regulatory costs.

Top-Heavy Regulatory World

Given the scope of regulatory costs, one might assume the 700 major rules issued since 2009 are on equal-footing. However, regulatory burdens are heterogenous in nature. Plotting just the ten largest rules since that time yields more than $403 billion in total costs or 44 percent of the overall total. In other words, 1.4 percent of the major rules generate 44 percent of the total regulatory burden.

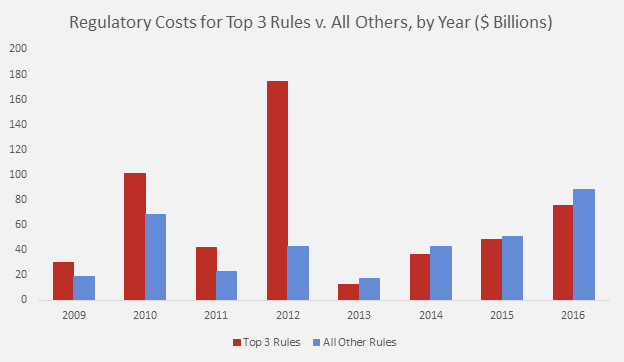

This trend largely continues with each annual snapshot. For example, in 2009, regulators published $48 billion in total costs. The top three largest measures produced $29.8 billion in total costs, or 61.5 percent of total costs. With 84 major regulations that year, 3.5 percent of major rules produced three-fifths of the regulatory costs in 2009.

A year later, 2010, was no different. That year, regulators published $169 billion in total costs. Yet, the top three largest rules produced more than $100 billion in long-term burdens or 59.6 percent of overall costs. Once again, just three percent of major rules produced nearly three-fifths of the regulatory burdens that year.

For a broader overview, the graph below compares the three largest rules in every year to the rest of the regulatory slate. It’s obvious the regulatory world is top-heavy, where a majority of costs and benefits are concentrated in three or four measures.

These trends are also more pronounced at the independent agency level, dominated by the financial regulators (Securities and Exchange Commission (SEC), Federal Reserve, and Commodity Futures Trading Commission (CFTC)). For example, since 2009 SEC has published $18.3 billion in regulatory costs, but $9.4 billion, or more than half, is courtesy of its three most expensive measures. Likewise, CFTC has published $9 billion in burdens since that time and its top three rules impose $6.3 billion in total costs. Whether it’s independent agencies, financial regulators, or environmental rules, the regulatory world is typically dominated by just a few substantive measures.

Reform

Congress has sought to address this issue in a variety of ways. Perhaps the most popular, and comprehensive, proposal is the “Regulatory Accountability Act” (H.R. 5). The House has passed H.R. 5 numerous times, including earlier this year, but the bill has languished in the Senate. Broadly, the legislation would address these billion-dollar rules by creating a new category of “high impact” regulations that would receive more scrutiny.

A high-impact rule is defined as a measure that would cost the economy $1 billion or more, cause a major increase in prices, adversely effect competition or employment, or significantly impact multiple sectors of the economy. Broadly, this mirrors the current definition of a “major rule,” but instead of a $100 million threshold for “annual effect,” H.R. 5 amends it to $1 billion in “annual costs.”

What’s the universe for this new category? President Obama issued 26 billion-dollar rules during his tenure, 3.25 annually. For President Bush, this figure was smaller, at 1.6 per year. It’s safe to assume if President Trump regulates more like President Bush, this high-impact classification will apply one or two times per year.

For rules that are classified as high-impact, the bill requires agencies to publish an advanced notice of proposed rulemaking, hold a public hearing before the adoption of the measure, provide a record of decision, and postpone the implementation of a billion-dollar rule until “final disposition of all actions seeking judicial review.” The latter step is important because with quick implementation deadlines, the sunk costs of a rulemaking generally accumulate well before courts weigh in on the legality of the rule. Winning in court can often prove to be a pyrrhic victory, with implementation nearly over before a final court verdict.

Although critics will complain that H.R. 5 might slow down the regulatory process, there are some billion-dollar rules that don’t take an entire administration to complete. For example, there were two billion-dollar rules from the Obama Administration where final publication in the Federal Register occurred before initial publication in the Unified Agenda. In other words, there was little advanced notice that a billion-dollar rule was imminent. In addition, there were three additional high-impact rules that had a rulemaking life (from initial publication in the Unified Agenda to final publication in the Federal Register) less than one year. “Liquidity Coverage Ratio,” “Amendments to Regulation SHO,” and “CAFE for MY 2011” took on average just 322 days to complete. In fact, the median time for a billion-dollar rule from the Obama Administration took less than two years complete. H.R. 5 aims to bring greater scrutiny to some of the most consequential regulations in history.

Conclusion

Although there is plenty of attention paid to the number of major rules or the total number of pages published in the Federal Register, through the forest, it’s best not to lose sight of the trees: high-impact rules that cost $1 billion or more. Although there are only two to three annually, they often impose the majority of regulatory costs and some move quickly through the process. It’s no surprise Congress has chosen to examine these measures in their regulatory reform portfolio.