Insight

March 7, 2024

SEC Finalizes Mandatory Disclosures for Public Companies of Climate-change Risks

Executive Summary

- The Securities and Exchange Commission (SEC) has acted to finalize a rule that will require public companies to provide climate-related risk data in their disclosures for the first time.

- Following intense criticism from industry, the SEC has dropped the most controversial aspect of the rule: the requirement that disclosures cover not just the financial risks stemming from climate (itself notoriously difficult to model) but the emissions of all actors in their “value chain,” including suppliers and product end users.

- Even heavily neutered, it is not clear that the SEC rule is necessary given the current risk practices of public companies and preexisting disclosure requirements; it is also not clear that the proposed rule is within the SEC’s constitutional mandate, or that the disclosure requirements would create comparable data of sufficient quality to have value to investors or the general public.

Context

The SEC has voted to finalize a rule that will, for the first time, require public companies operating in the United States to provide climate-related information in both their registration statements and annual reporting. These disclosures will require businesses to provide information on the climate-related risks they face, their governance and risk management processes in place to mitigate those risks, and their greenhouse gas (GHG) emissions.

The SEC’s Proposal

The final rule will require public companies to disclose:

- Climate-related risks that have had or are reasonably likely to have a material impact on the registrant’s business strategy, results of operations, or financial condition;

- The actual and potential material impacts of any identified climate-related risks on the registrant’s strategy, business model, and outlook;

- If, as part of its strategy, a registrant has undertaken activities to mitigate or adapt to a material climate-related risk, a quantitative and qualitative description of material expenditures incurred and material impacts on financial estimates and assumptions that directly result from such mitigation or adaptation activities;

- Specified disclosures regarding a registrant’s activities, if any, to mitigate or adapt to a material climate-related risk including the use, if any, of transition plans, scenario analysis, or internal carbon prices;

- Any oversight by the board of directors of climate-related risks and any role by management in assessing and managing the registrant’s material climate-related risks;

- Any processes the registrant has for identifying, assessing, and managing material climate-related risks and, if the registrant is managing those risks, whether and how any such processes are integrated into the registrant’s overall risk management system or processes;

- Information about a registrant’s climate-related targets or goals, if any, that have materially affected or are reasonably likely to materially affect the registrant’s business, results of operations, or financial condition. Disclosures would include material expenditures and material impacts on financial estimates and assumptions as a direct result of the target or goal or actions taken to make progress toward meeting such target or goal.

In addition, the proposed rule would mandate that for certain aspects of the proposed requirements, most notably those sections related to GHG disclosures, public companies must obtain, over time, first “limited” and then “reasonable” “assurance” of the accuracy of the data provided. “Assurance” in this instance is guided by the attestation standards of global accountancy and ssuggests that data provided in these disclosures will eventually require third-party audit or consultation.

Changes to the SEC’s Original Proposal

First proposed in early 2022 (for the American Action Forum’s review of the rule, see here) the rule as voted on is unmistakably weaker, with several notable mandatory disclosure requirements instead reclassified as voluntary. The key change is that public companies will no longer be required to inform investors of their GHG emissions and the risks they face from weather events, both in and of themselves and the emissions of all actors in their “value chain,” including suppliers and product end users. Instead, large actors will be required to report the emissions they directly produce only if they themselves consider those emissions “material,” with the original requirements instead being a voluntary disclosure where material.

The SEC made other, less significant requirements less onerous. Companies will no longer be required to disclose the climate expertise of their boards. In other regards the proposal remains the same: smaller firms, the vast majority of all public companies in the United States, remain exempt from GHG emission disclosure; the SEC also resisted the urge to clarify or strengthen existing definitions of materiality.

Notably, while the initial stakeholder reaction to the rule was characterized by vocal criticism from the companies likely to be captured by the disclosure requirements, the significant watering-down of these requirements in the final rule has attracted criticism from environmental advocates for being insufficient to spur meaningful climate change. As a result, the final rule has been characterized, including by SEC commissioners, as “too lax by some and too strict by others.”

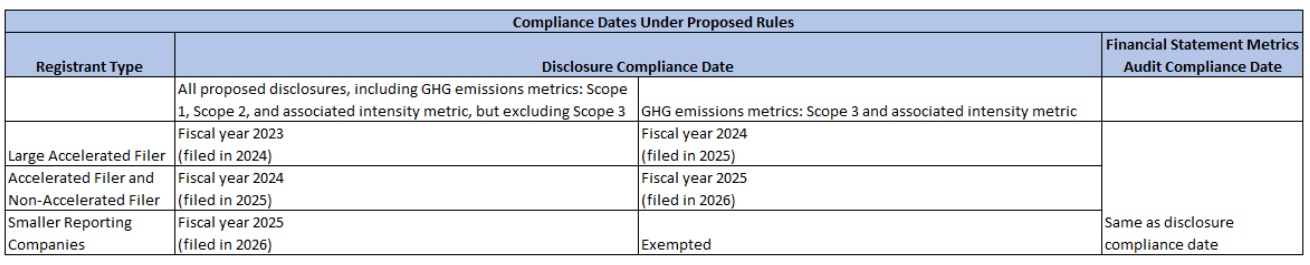

Timeline and Accommodations

The proposed rule provides phase-in timelines for public companies depending on their “filer status,” ranging from large accelerated filers to smaller reporting companies. Operating under the assumption that the proposed rule would be adopted in December 2022, compliance – first with part and then with all the proposed requirements – would be necessary between fiscal years 2023 and 2025, with the various “assurance” requirements in force in following years.

Source: SEC Final Rule

As per normal procedure, the rule will become effective 60 days after being posted in the Federal Register. Despite its weakened form, the final rule is expected to see significant court challenges.

Analysis

Who is this for?

While the intended beneficiary of the SEC’s proposed rule is clearly the public in furthering the Biden Administration’s social goals relating to climate change, the SEC in the proposed rule goes to considerable lengths to name-check groups of concerned investors demanding not simply that public firms disclose climate-related risks but that governments mandate these requirements (most notably the Glasgow Financial Alliance for Net Zero, a coalition of over 450 firms from 45 countries managing assets over $130 million). A public company’s investors and shareholders quite rightly exert broad control over the direction and goals of a company, and in coordinated effort tend to have their demands met.

This makes the SEC’s proposed rule largely unnecessary: Where public company investors demand climate-related disclosures, they do so and have the power to have their needs met, with no government involvement required. It is for this reason thousands of companies already disclose their emissions and reduction targets under voluntary standards set by their own industries. The SEC proposed rule noted two particular examples – the Task Force on Climate-Related Financial Disclosures and the Greenhouse Gas Protocol – but it is not clear that the existence of standards without the SEC is as strong an argument for its involvement as the SEC appears to think it is. It is worth noting, however, the recent trend of several large public companies withdrawing from international ESG coordination efforts.

Certainly the United States is considered to trail its international colleagues, particularly the European Union, in the implementation of disclosure standards on climate-related risk. As is often the case with financial services regulation, European practices strongly influence U.S. regulatory developments. Therefore, the United States will very likely end up with ESG standards in some form, but the implementation of these standards and understanding the differences between U.S. and international markets will remain key.

Perhaps the most interesting fundamental question is whether the SEC’s proposed rule even represents an additional disclosure requirement. Companies are already required to disclose any material information in their risk assessments, and this can and does already include, for many companies, data related to climate-related risks. In essence, the proposed rule may simply duplicate existing requirements.

How useful would the proposed rule be?

The SEC’s stated goal is to codify existing practices with a view to consistency and comparability. While these are goals shared by the investor community when it looks at the quality of the available data, realizing this dream represents a significant challenge, particularly as the quality of climate-related risk data remains poor. Climate science itself suffers from a wide range of assumptions and estimates, competing methodologies and definitional issues, and the financial models predicated on these can and do achieve wildly different results on the same input data. Garbage data in means garbage data out.

The SEC proposal represents two unique data challenges. The first is the difficulty in assessing GHG emissions along an entire supply chain. While the updated rule makes this a discretionary rather than necessary requirement, this does not change the difficulty. The second is the reliance on the accounting concept of materiality, itself a somewhat subjective measure on which to hang an entire disclosure framework, as businesses will be required to decide for themselves what is material to whom, dooming comparability from inception. Both these questions are made immeasurably more complex by the proposed requirement that businesses assess these over the long term with timeframes that could span decades.

Of course, simply having an SEC disclosure requirement and data formats will likely encourage data standards in climate-related risk to improve, but this process will likely take years before investors – the target beneficiary of the rule – will make investment decisions based solely on climate data reported. This also puts a significant burden on the SEC to both determine and provide guidance on the standards and scenarios it itself will require of reporting companies in an effort to obtain standardization. Allowing businesses themselves to make these judgments as to the appropriateness of models and scenarios (while making it difficult to compare) was certainly the easier path the SEC neglected to take.

What are the potential costs?

As with any landmark regulatory framework, achieving compliance will be a costly effort, with a paperwork burden of about 15 million hours and an additional $5 billion in regulatory costs for public companies per year (note that these values have decreased by 10 million hours and $1.5 billion in costs with the program changes to the final rule). As always, these costs will inevitably be passed on to the consumer and discourage new business entrants and companies going public.

In addition to the obvious and upfront costs, businesses will have to be wary of new legal exposure as disclosure requirements make them liable to the SEC – and potentially investors and the public – for the data they provide (concerning even in an industry where good quality data is available). These concerns are somewhat obviated by the existence of a regulatory safe harbor, but these rarely provide exhaustive coverage. The requirement that public companies receive assurances for their disclosures will also create a new ancillary climate-related audit industry that will drive up compliance costs.

What does this mean for the SEC?

The SEC proposed rule raises significant concerns as to the constitutionality of such a sweeping new framework and expansion of its responsibilities. Requiring public companies to disclose non-material data (progress on climate-related goals, for instance) could violate those companies’ First Amendment rights, and by the government’s own standards the rule may not pass the strict scrutiny test demonstrating either a “compelling governmental interest” or that the rule has been tailored as narrowly as possible to meet this interest.

Even if the courts decide that the expansion of the SEC’s role is constitutional, the new direction for the agency represents time, effort, and expense that would divert agency attention away from its traditional duties. Perhaps most compelling, the SEC is not the government agency tasked with climate-change and environmental protection. Requiring, for instance, GHG emission disclosures would necessitate the SEC to achieve a high level of knowledge and understanding of environmental science; this would be an enormous undertaking for a goal that may not be consistent with the agency’s mandate and may undercut the SEC’s credibility in its core mission. In a similar vein, the original requirement for Scope 3 emissions disclosures as drafted would have required public companies to obtain information from private companies in their value chain, indirectly bringing privately held companies within the regulatory scope of the SEC.

More broadly, the use of government agencies to advance certain social and political goals raises questions as to picking regulatory winners and losers and interfering with the economic investment of capital, necessarily distorting the market to meet these goals. What other social ills might tangentially involved agencies seek to address?

Conclusions

In attempting to enhance and make comparable disclosure practices that in many cases already exist, the SEC’s proposed rule raises serious questions ranging from constitutionality to even the basic necessity of a regulatory land-grab that seeks to tell businesses not only what they must do but also how they must address climate change. In what amounts to a desire to influence capital allocation decisions on the basis of political and social ends, the SEC arrogates a brand-new mission statement to itself – policing climate change – that it has neither the knowledge base nor likely the constitutional mandate to perform. This is hardly a convincing platform on which to construct a new disclosure regime that is already largely being adhered to voluntarily, would be extraordinarily costly, and most important, not be of sufficient quality to drive investor decisions for years to come.