Insight

October 13, 2016

Tax Topics: Employees and Independent Contractors in the Sharing Economy

Summary

- Many workers in the sharing economy are classified as independent contractors

- Worker classification involves important legal and tax consequence at both the firm and individual business level – most conspicuously that firms nominally pay half of employees’ payroll taxes

- Despite the important tax distinctions between employees and individual contractors, the independent contractor classification is more a function of worker flexibility than tax considerations

Introduction

The rapid growth of the sharing or “gig” economy reflects broad popularity among consumers and service providers, but also reveals public challenges. Existing laws apply unevenly to these disruptive industries by virtue of the employment status of their employees. The status of independent vs. fully employed drivers, for example, has emerged as a recurrent topic, contrasting taxi companies with “sharing economy” businesses such as Uber and Lyft. The debate essentially boils down to the extent to which providers of services in the “gig” or sharing economy arrangements are employees of an intermediary entity, such as Uber or Lyft. This classification carries significant legal and economic consequences, as labor and tax law divide sharply between employees (even part time) and independent contractors. Beyond broader labor law implications, the employment status of taxi drivers has ample ramifications in terms of employment taxation. This primer examines this distinction for tax purposes and considers its implications for participants in the sharing economy.

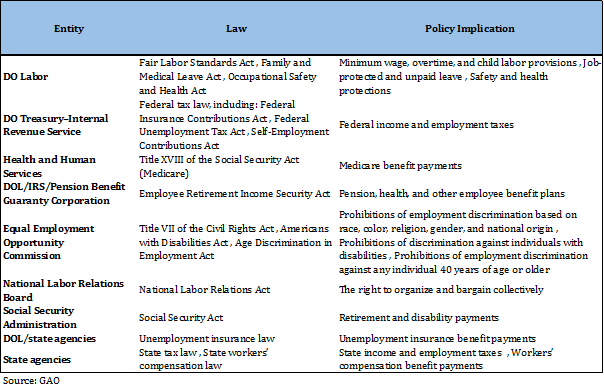

Employment Classification

A host of employment statutes, including tax laws, hinge on the classification of a worker as an employee of a firm or as an independent contractor.[1]

Table 1: Implications of Employee Classification

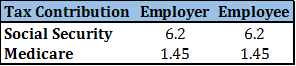

The tax implications of employment classification are considerable. Under federal law, employers incur a tax liability for employees in the form of certain payroll taxes, as well as the obligation to withhold federal income tax for which employees are liable. Federal payroll taxes consist of the Federal Insurance Contributions Act (FICA) and the Federal Unemployment Tax Act (FUTA) taxes, which are withheld by the employer. FICA taxes (Social Security and Medicare insurance) are divided between employer and employee, and amount to 15.3 percent of the first $118,500 of an employee’s pay.[2]

Table 2: Composition of FICA Taxes (%)

Added to FICA is the FUTA tax, which provides revenue for the unemployment insurance (UI) system. This tax is a payroll tax paid entirely by the employer and amounts to 6 percent of the first $7,000 of an employee’s income. Employers may claim a 5.4 percent credit against payments made to state unemployment funds through state unemployment taxes (SUTA) taxes, reducing the net federal tax to 0.6 percent. Note that benefit payments under the UI system are financed by SUTA taxes, with the federal levy generally collected for administrative costs, and certain extended benefit payments.

Employers also withhold federal income tax, though unlike FICA and FUTA taxes, employers do not have a direct income tax liability on employee wages. However, federal income tax withholding does create an administrative burden. In addition to these federal tax obligations, employers also provide health and other tax-preferred benefits that incur both direct and indirect costs on employers. According to the Bureau of Labor Statistics, 31 percent of total employee costs for employers was in the form of non-wage benefits.[3]

Self-employed independent contractor

Labor law allows for classification of certain workers as independent contractors if their work patterns meet several tests. However, these tests vary across federal statutes, resulting in some circumstances whereby workers are classified as employees for the purposes of labor law but an independent contractor for another statute.[4] The test for the IRS determination of worker classification, for example, is based on 20 separate characteristics.[5] What constitutes an independent contractor defies easy explanation. Despite these definitional challenges, independent contractors can broadly be viewed as engaged in flexible, part time labor, and are typical of workers participating in the sharing economy.[6]

Unlike employees, independent contractors are not subject to employer-level tax withholding. Rather, independent contractors are responsible for paying estimated income taxes on a quarterly basis directly to the IRS.[7] More consequentially, independent contractors are responsible for paying the full federal and state income taxes under the Self-Employed Contributions Act (SECA). The tax rate is equivalent to the combined employer-employee FICA rate of 15.3 percent (12.4 percent towards Social Security, and 2.9 percent towards Medicare) on the first $118,500 of income.[8] Unlike employees, independent contractors are not typically covered by unemployment insurance or workers’ compensation taxes.[9]

Assessing the Tax Considerations for “Gig” Economy Workers

On its face it might appear as though independent contractors are worse off than similarly situated employees for tax purposes: they bear the full brunt of payroll taxes and are precluded from receiving unemployment benefits, which are borne by employers anyway. This would be a misreading of the true burden, or incidence of taxation. Tax liability does not necessarily reflect the true burden of taxation. So, while FICA and FUTA taxes are nominally assessed on employers, in part for the purpose of FICA taxes and entirely with respect to FUTA taxes, the true economic burden, or incidence, is actually passed on to employees in the form of lower wages.[10] Thus, to the extent that an employer must pay payroll taxes, the employer reduces compensation costs accordingly. A comparison of wages for Uber drivers and Taxi drivers bears this out. According to one study, in nearly all markets surveyed, hourly earnings of Uber’s driver-partners exceeded those of taxi drivers and chauffeurs, with an average hourly earnings premium of more than $6.[11]

Some commenters observe that companies such as Uber and Lyft partner with independent contractor drivers to avoid these taxes. The broad consensus of the economics literature reveals that these taxes are passed on by employers, and the tax implications are largely irrelevant. Rather, the prevailing considerations for classifying gig economy partners relates to flexibility and other non-tax considerations. Survey results suggest that the flexibility to control one’s own schedule is highly valued among gig-economy participants, specifically drivers.[12] Indeed, for the vast majority of these workers, driving for Uber or Lyft is a part time endeavor, with 80 percent of Lyft drivers working less than 15 hours per week and half of all Uber drivers working less than 10 hours per week.[13]

Conclusion

The basic economics of worker classification have less to do with employer tax considerations than we often assume. With respect to worker classification and the “gig” economy, there are important tax distinctions between employees and independent contractors. These distinctions reflect the nexus of tax obligations, specifically with respect to payroll taxes and the administration of income tax withholding. While these distinctions may appear to favor firms that rely on independent contractors, and would suggest firms that utilize independent contract labor are avoiding costs, the economics suggest otherwise. Rather, independent contractors’ role in the sharing economy isn’t about taxes, but instead reflects the fluid on-demand nature of both “gig” economy consumers and service providers.

[1] http://www.gao.gov/new.items/d06656.pdf

[2] https://www.irs.gov/pub/irs-pdf/p15.pdf; note that the $118,500 “cap” is subject to annual revision

[3] http://www.bls.gov/news.release/ecec.nr0.htm

[4] https://www.aei.org/wp-content/uploads/2012/08/-the-role-of-independent-contractors-in-the-us-economy_123302207143.pdf

[5] https://www.irs.gov/pub/irs-utl/x-26-07.pdf

[6] For a more thorough examination of the role of independent contractors in the sharing economy see: https://www.americanactionforum.org/research/independent-contractors-and-the-emerging-gig-economy/

[7] https://www.irs.gov/individuals/self-employed

[8] https://www.irs.gov/businesses/small-businesses-self-employed/self-employment-tax-social-security-and-medicare-taxes

[9] https://www.aei.org/wp-content/uploads/2012/08/-the-role-of-independent-contractors-in-the-us-economy_123302207143.pdf

[10] https://www.cbo.gov/sites/default/files/114th-congress-2015-2016/reports/51361-HouseholdIncomeFedTaxes.pdf: “reflects a consensus among economists. See Don Fullerton and Gilbert E. Metcalf, “Tax Incidence,” in Alan J. Auerbach and Martin Feldstein, eds., Handbook of Public Economics, vol. 4 (Elsevier, 2002), pp. 1787–1872”

[11] https://irs.princeton.edu/sites/irs/files/An%20Analysis%20of%20the%20Labor%20Market%20for%20Uber%E2%80%99s%20Driver-Partners%20in%20the%20United%20States%20587.pdf

[12] http://economics21.org/sites/e21/files/HouseEducationWorkforceTestimony-1.pdf

[13] Ibid.