Testimony

February 15, 2023

Climate-related Economic Risks and Their Costs to the Federal Budget and the Global Economy

Testimony to the U.S. Senate, Committee on the Budget

*The views expressed here are my own and do not represent the position of the American Action Forum. I thank Gordon Gray, Sarah Hale, and Angela Kuck for their assistance.

Chairman Whitehouse, Ranking Member Grassley, and members of the Committee, thank you for the privilege of appearing today. In this short testimony, I want to make three key points:

- Climate change will increase future budget deficits, largely through reduced economic growth and tax revenues;

- The existing (baseline) budget outlook is profoundly anti-growth and represents a larger economic risk than climate change; and

- Addressing the budget outlook will make more manageable budgeting mitigation and adaptation policies that will feature large, up-front federal outlays.

Let me discuss each in turn.

Budget Impacts of Climate Change

Climate change will likely produce higher average temperatures, rising sea levels, and increasing extreme weather events. There will be some dramatic changes in particular regions and industries, and these will be reflected in dramatic changes in the financial structures backing those real economic activities.1

But from an aggregate macroeconomic and federal budgetary perspective, the impact of climate change will be to damage and reduce the value of agricultural land, infrastructure, and capital assets, as well as reduce the ability to supply labor. This will show up as lower measured economic activity and reduced collections of income taxes, payroll taxes, excise taxes, and other revenues. There will be impacts on the spending side of the budget, as well from the additional stresses climate change places on mandatory programs (e.g., the National Flood Insurance Program), and as Congress chooses to allocate additional discretionary resources.

In its recent survey, the Congressional Budget Office (CBO) concluded: “Drawing on studies that examine the historical relationship between regional output and regional temperature and precipitation, along with projections of future conditions, CBO has projected that, on net, climate change will lower the level of real (inflation-adjusted) gross domestic product (GDP) in 2051 by 1 percent from what it would have been if climatic conditions from 2021 to 2051 were the same as they were at the end of the 20th century. That figure is a central projection in a wide range of possible outcomes and does not reflect every channel by which climate change can affect GDP.”

To put this in perspective, a 1 percentage point decline in real GDP in 2051 is the equivalent of an annual growth rate in GDP that is lower by 0.034 percentage points. From a macro, aggregate perspective, the economic consequences of climate change over the next 30 years do not appear daunting.

The Economic Risks of the Budget Outlook

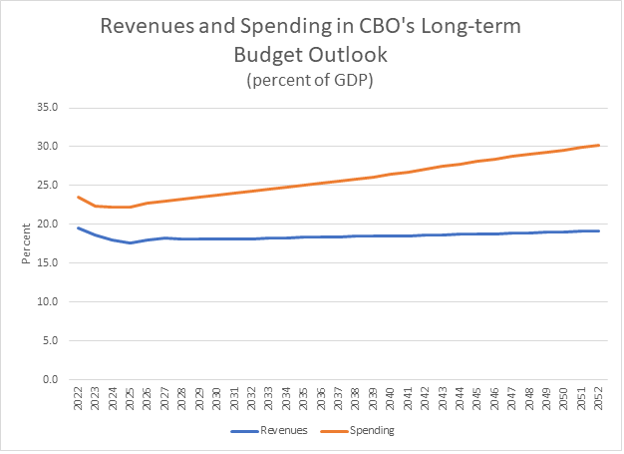

The same cannot be said for the economic consequences of the federal budget outlook. The chart (below) replicates the spending and revenues (as a percent of GDP) contained in the CBO’s most recent Long-Term Budget Outlook. The key feature is that spending rises much faster than revenues, leading to rising deficits.

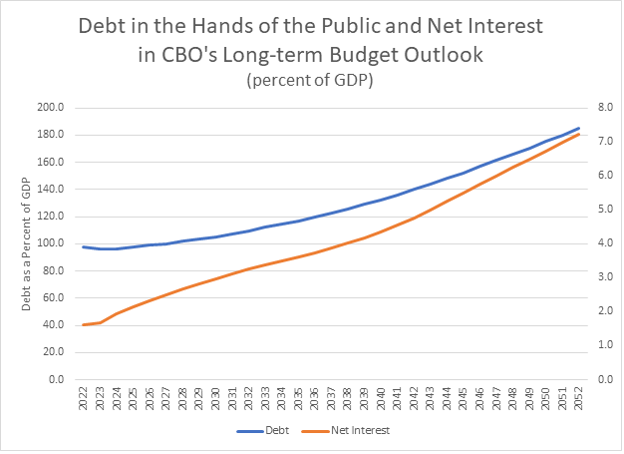

This manifests as rising debt in the hands of the public (graph below, left scale) and rising net interest costs (right scale) as time passes. Clearly, debt rising toward 200 percent of GDP, and net interest rising toward 8 percent of GDP, is ultimately unsustainable. Eventually the inability of the federal government to exercise effective governance over its borrowing needs will shake faith of capital markets and a sovereign debt crisis will ensue.

While mechanically correct, this scenario is not the most likely or most threatening. The economic damage of fiscal irresponsibility is likely large and much more immediate. A relatively large literature stemming from the research of Carmen Reinhart and Kenneth Rogoff indicates that when gross government debt (as a percent of GDP) gets large enough (in their work, exceeds 90 percent) median growth is roughly 1 percentage point lower annually than for comparable countries with lower debt burdens.2 With its large federal gross debt, the United States is likely already paying a growth penalty and, even if not fully 1 percentage point annually, this dwarfs the economic threat posed by climate change.

The Mechanisms of Slower Growth

What channels produce slower growth? The key insight is that debt is issued to allow the federal government to attract capital away from the private sector. In its recent review of the impact of infrastructure spending on the economy, CBO noted that an additional dollar’s worth of private fixed capital increases real potential GDP by 9.8 cents (net of depreciation), while for public capital the net effect is an increase of 9.2 cents. So, if the debt shifts spending from private to public capital, the overall effect is a loss in productivity and growth.

But that is the best-case scenario. The vast majority of deficit-financed spending is for programs (e.g., Social Security and Medicare) that subsidize consumption and not public investment. In this case, the productivity effect is zero and the loss is the full 9.8 cents per dollar of borrowing.

Of note, the same losses in productivity would occur if the dollars were shifted from private investment to the federal budget using tax policy. Hence, any strategy for reducing deficits and debt that relies significantly on tax increases will do little to improve economic performance.

For this reason, the essence of a better strategy to address the fiscal future is to pair entitlement reform with tax reform, thereby controlling the underlying source of debt explosion and supporting the most rapid pace of economic growth possible.

Addressing the Outlook Makes Budgeting Climate Change Policies More Manageable

The key aspect of federal policies to mitigate greenhouse gas emissions or adapt to climate change is that they require large, up-front federal spending (or tax credits or regulation). Especially given the abject nature of the federal fiscal outlook, the outlays needed for pathways to net-zero emissions in the next 10–15 years are impossibly expensive.

For example, the American Action Forum published research on how much it would cost to get to 100 percent renewable power over 10 years. That study found that merely installing the required renewable capacity — in the form of solar, wind, hydroelectric, and storage — would cost $5.7 trillion.3 The assumptions under which these costs were calculated were very optimistic and other studies have found a need for investment of a comparable magnitude. It is not obvious how much of this investment would be on the federal budget, but the existing budgetary woes would hamstring any serious effort at mitigating and adapting to climate change.

This is one example of a more general problem. Given that mandatory spending constitutes 70 percent of the federal budget, there is no room for significant additional discretionary outlays – precisely the type of spending where the federal government can finance infrastructure, education, national security, and other investments in the nation’s future.

Thank you and I look forward to your questions.