Testimony

November 19, 2024

Testimony on: Building on the Success of the TCJA: The 2025 Tax Policy Debate

Chairman Heinrich, Vice Chairman Schweikert, and members of the committee, thank you for the privilege of appearing today to discuss the tax and fiscal policy issues surrounding the sunset of a large portion of the 2017 Tax Cuts and Jobs Act (TCJA) at the end of 2025. I would like to make three main points:

- The United States has two major economic policy challenges: too-slow trend economic growth and a large and unsustainably growing federal debt.

- TCJA has a strong record of success as pro-growth tax policy, but 2025 is an opportunity to continue the process of tax reform, strengthening the growth incentives in the tax code.

- At a minimum, the 2025 legislation should not make the fiscal trajectory worse than under current policy; at best, it could both strengthen growth and lower projected deficits.

Let me discuss these in turn.

The Policy Problems

The U.S. economy has a poor growth record in the 21st century. From 1960 to 2000, per capita gross domestic product (GDP) growth averaged 2.3 percent annually. Since then, it has declined to 1.4 percent. This rough estimate of the standard of living once doubled every 30 years. In the 21st century, it is predicted to take 51 years. There should be a renewed policy focus on raising the trend rate of economic growth.

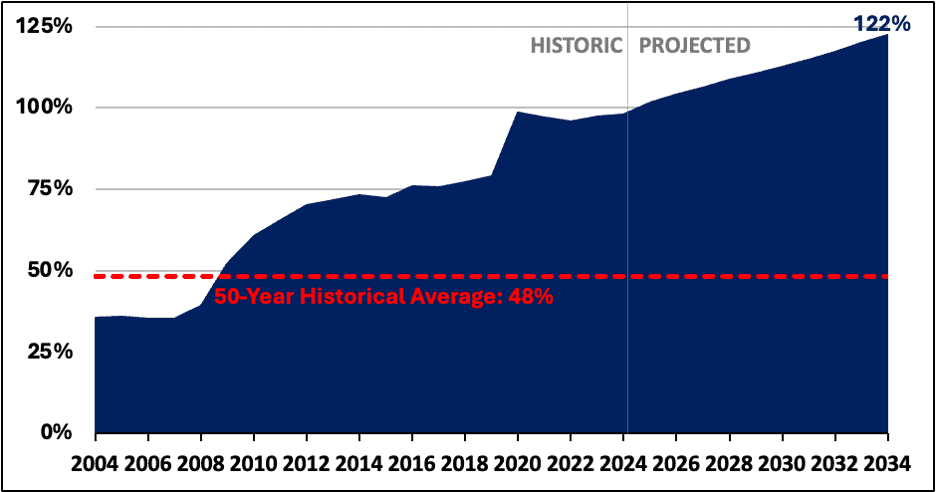

The federal government has a debt problem. The Congressional Budget Office (CBO) projects that federal debt held by the public will rise from 98 percent of GDP at the end of fiscal year (FY) 2024 to a new record of 106.2 percent of GDP by the end of 2027. It will grow further to 122 percent of GDP by the end of 2034 and continue to rise over the long term. The national debt has grown such that the cost of servicing it was the second-largest government expenditure this past fiscal year. The nation’s accumulation of debt has largely been the result of unique crises and a structural deficit. The failure to do the hard work of deficit reduction has put the United States at risk of being unable to meet future fiscal and economic challenges.

Debt Held by the Public Under Current Law (Percent of GDP)

Source: CBO.

The Role of the TCJA

The TCJA has a proven record of supporting faster growth. Before 2017, the United States was saddled with the highest corporate-tax rate at 35 percent and clung to a “worldwide” system of taxation, by which U.S. companies were taxed at home and abroad, while competitors began to adopt a single-tax territorial system.

In practice, this meant that if a U.S. company and a German company competed in Sweden, the German one would pay only Swedish tax. Its American competitor would pay both the Swedish tax and the U.S. tax, topping up its bill to 35 percent. But there was a perverse incentive: The company could defer paying the difference if it didn’t repatriate its profit back to the United States. To remain competitive, companies locked trillions of dollars in profits offshore. Worse, if a U.S. firm became involved in a cross-border merger or acquisition, its fiduciary responsibilities would dictate that its headquarters be moved out of the high-tax United States, a transaction known as an inversion.

Workers knew that punishing dynamic well. Thousands of them were left behind as their companies’ leadership, struggling to compete, packed up and moved away. The TCJA sought to arrest this decline by freeing corporations from the obligation to pay U.S. taxes on overseas earnings and by allowing them to write off more of the cost of new equipment, machinery, software, and buildings.

Each of these provisions was intended to increase American firms’ competitiveness and increase workers’ well-being. They succeeded. The United States suffered the exodus of 33 companies between 2005 and 2015. As the Tax Policy Center reports, there have been no major tax-motivated inversions since the TCJA was enacted in 2017.

Along with moving toward a more territorial system, the TCJA’s rate cuts drew more investment, research, and intellectual property back to the United States. Each dollar of corporate-tax reduction has been estimated to increase economic production by 44 cents. The TCJA stimulated U.S. investment by 20 percent among companies experiencing the average tax change. For workers, the 9 percent increase in inflation-adjusted earnings between Jan. 1, 2018, and Dec. 31, 2020, was the fastest growth since the government began publishing data in 1979.

The Role of 2025 Tax Policy

The goal in 2025 should not be to merely renew or extend the TCJA. Rather, 2025 is the opportunity for additional tax reform to enhance the incentives to invest, innovate, and allocate capital efficiently. The general rule for doing so is to make the tax base as broad as possible, while keeping tax rates as low as possible.

There are also some very specific and clear potential improvements. For example, it would be useful to make permanent the expensing of investments and research and development expenditures. TCJA had such a regime in place, but it had to be phased-out due to budgetary considerations. Full expensing would remove a tax consideration from the choice among wages, investment in skills, investment in physical capital, and investment in innovation. This sort of neutrality is the objective of good tax policy.

Another important issue is the relative taxation of the return to capital in the corporate and pass-thru entities (S-corporations, limited liability corporations, partnerships, and so forth.) Since more than half of business income is taxed as pass-thru income, it is a central part of the U.S. approach to taxing business income.

The good news is that the corporation income tax provisions from TCJA are permanent. Thus, while they might be tweaked, they are largely successful and need little attention. Instead, the focus should be on providing comparable tax treatment to pass-thru income so that there is the same effective marginal tax rate on the return to capital invested in the corporate sector and the pass-thru sector.

What would that look like? Suppose a dollar invested in the corporate sector earns a return, r, which is then taxed at the corporation income tax rate, t (currently 21 percent). The after-tax dollars are then distributed to shareholders as either dividends or capital gains and taxed at the preferential rate, m (currently 20 percent). This is shown on the right side of the table (below).

| Pass-Thru | Corporation | |

| Initial Investment | $1 | $1 |

| Taxable Return to Capital |

ae |

r |

| Return After Business-level Tax |

ae |

r(1-m) |

| Return After Individual-level Tax |

ae(1-t) |

r(1-m) (1-t) |

Consider, now, a pass-thru entity. Suppose it earns e on each dollar invested. For purposes of calculating taxes, assign a share of the earnings, a, as the return to capital investment, which are then taxed at the preferential tax rate just like distributions from corporations. Comparing the computations in the left and right columns the after-tax returns to the $1 investment are identical when:

ae(1-t) = r(1-m) (1-t).

Solving implies that the administratively set share (a) be set according to:

a = (r/e)(1-m).

Notice, however, that total return (e) for the pass-thru is the sum of return to capital (r) and return to labor (l), so this is just:

a = (r/(r+l))(1-m).

In words, the key parameter, a, is simply the after-corporate-tax share of capital in income.

To get a feel for magnitudes, use the conventional assumption that the share of capital is 0.3 and the corporate tax rate is 0.21. If so, the key value is a = 0.237. This approach dramatically simplifies pass-thru taxation. Simply take 23.7 percent of the overall earnings and tax it at the dividends and capital gains rate of 20 percent.

The main advantage to this approach is economic efficiency, with the tax code no longer distorting the choice between corporate and non-corporate investments. The return to pass-thru capital investments is taxed at a single rate, scaled to be comparable to the overall tax on corporate investments. In contrast, the current system provides a 20 percent deduction, which translates into a different tax rate for each tax bracket, with none guaranteed to match the after-tax return from the corporate sector.

The idea sketched above is far from a complete proposal, but it demonstrates that there are alternatives approaches that could be on the table in 2025. Given the economic circumstances – sub-par trend growth and high federal debt – a premium should be placed on efficient, pro-growth tax systems.

Tax Policy in 2025 and the Debt Challenge

Policymakers must be cognizant of the debt challenge in the tax deliberations next year. Indeed, the overall goal should be to quickly stabilize the debt relative to GDP, and then put the debt/GDP ratio on a negative trajectory. To do so would eliminate fears that the U.S. federal government cannot control its fiscal future and take off the table any possibility of crisis over international reliance on the dollar. (See here for one approach to this challenge.)

It is equally important, however, for policymakers to recognize that there is no real, permanent solution to the debt threat without serious attention to spending reforms.

Here is the budgetary arithmetic. Over the next 10 years, the CBO baseline indicates that Social Security and Medicare will account for $36 trillion of the $71 trillion of non-interest spending – more than 50 percent from those two programs alone. So, the notion that that one cannot touch those two key pieces of the social safety net and make real progress on the deficits and debt is numerically baseless.

Moreover, these programs grow very rapidly. CBO anticipates that Social Security spending will grow at an average annual rate of 5.5 percent, while Medicare will average 7.0 percent. In contrast, revenue typically grows at the rate of the nominal economy. If the United States averages 2.0 percent real growth and inflation hits the 2.0 percent target, then revenue will grow at 4.0 percent per year. (The actual growth in the CBO baseline is 4.3 percent.)

There’s the problem: Social Security spending is projected to grow at 5.5 percent and Medicare spending at 7.0 percent versus revenue at 4.0 percent.

In short, the demands of the largest federal spending programs are outstripping the resources to fund them by a greater margin every year. Now, it would be possible to close the gap with a large tax increase (putting at risk the goal of better growth), but having done so, what would happen? The two largest entitlement programs would continue to grow at 5.5 and 7.0 percent and revenue would still grow at 4.0 percent. The gap would widen each year, and the deficits and debt would re-appear and increase. Again, there is no solution to the federal debt challenge without serious spending reforms.

What, then, should be the budgetary framework for the 2025 debate? At the very minimum, the legislation should not worsen the fiscal outlook. This amounts to using a current-policy baseline and making sure that the legislation is revenue neutral. As a practical matter, it means that any deviation from a straight-up extension of the TCJA must be paid for.

At the other end of the spectrum, the gold standard for a bill would be a pro-growth reform that is deficit neutral relative to a current-law baseline. This is the gold standard for two reasons. First, it provides the greatest progress toward the fiscal goals. Aso, if the reform is undertaken using reconciliation procedures (as it appears it will be), then the deficit neutrality would mean that the tax reforms could be permanent, and thus more effective.

Thank you and I look forward to your questions.