Weekly Checkup

February 5, 2021

Evaluating a COBRA Subsidy Now

Back in the early months of the COVID-19 lockdown orders, there was well-founded concern about the insurance status of the 22 million workers who lost jobs between mid-March and mid-April. At the time, the idea of subsidizing COBRA premiums was floated as a way of keeping these workers from losing their health insurance coverage on top of losing their jobs. Now the idea is once again gaining traction, having been proposed by President Biden as part of his $1.9 trillion “American Recovery Plan.” The idea might have had merit originally, but circumstances have changed, so it’s worth considering when COBRA subsidies might or might not make sense.

COBRA is a transitional insurance program that allows employees to continue with their existing employer-sponsored insurance (ESI) plan after job loss for between 18 and 36 months in most cases. The catch is that the former employee must pay both the employee and employer shares of the premium. As a result, COBRA provides continuity, but it also can be prohibitively expensive.

Back in April 2020, I argued in the Weekly Checkup that a COBRA subsidy might be a good idea. It seemed to me that amid staggering job loss and a rapidly expanding public health crisis, keeping people in their existing insurance and provider networks made a lot of sense, and a COBRA subsidy would have helped to accomplish that goal. As it turns out, the vast majority of those who lost their insurance as a result of pandemic-related job loss ended up having access to other ESI coverage through family members, or to subsidized coverage through Medicaid and the Affordable Care Act (ACA). But even still, it seemed less than ideal to have recently unemployed individuals struggling to navigate new provider networks amid a pandemic. Additionally, much of the job loss was anticipated to be temporary. Switching insurance coverage only to switch back a few months later seemed burdensome and unnecessary. A temporary subsidy that would have made it affordable for people to stay in their existing ESI plan through the end of 2020 seemed sensible. Speaker Pelosi did include a subsidy of COBRA premiums retroactive to March 1, 2020, through January 31, 2021, as part of the Health and Economic Recovery Omnibus Emergency Solutions (HEROES) Act in May, but that legislation was never enacted.

Now President Biden is calling for a COBRA subsidy, but the ground has shifted and the policy makes less sense than it did last year. For one thing, unemployment has shrunk since the initial layoffs. Certainly, people are still losing jobs because of the pandemic, but at nowhere near the levels seen earlier, so the risk of a large group of people losing ESI is much less than it was last year. Also, people who are still unemployed at this point are unlikely to be going back to their old jobs. It makes sense for those individuals to transition to another form of coverage. Further, if their COBRA premiums were a significant financial burden, they could have accessed subsidized ACA coverage in the aftermath of their job loss, or during the end of year open enrollment period that just closed in December—a normal time to transition from one insurance plan to another. If they’re still paying COBRA premiums and are only now finding it to be untenable, the Biden Administration is offering another open enrollment period starting later this month.

But if the Democrats want to enact a COBRA subsidy, how large should it be? While House Democrats previously proposed a 100 percent subsidy, in 2009 the federal government provided a temporary COBRA subsidy of 65 percent, and for his part Biden has not specified a percentage. It seems to me that subsidies for COBRA should not exceed what an individual or family would receive if they purchased coverage through the ACA marketplace. Competing federal subsidies of various amounts are inefficient and unfair.

Ultimately, it’s just not clear that the same need for a COBRA subsidy exists now that might have existed last year. Instead, this feels like a residual policy idea, still hanging on from last year because no one has stopped to reevaluate it.

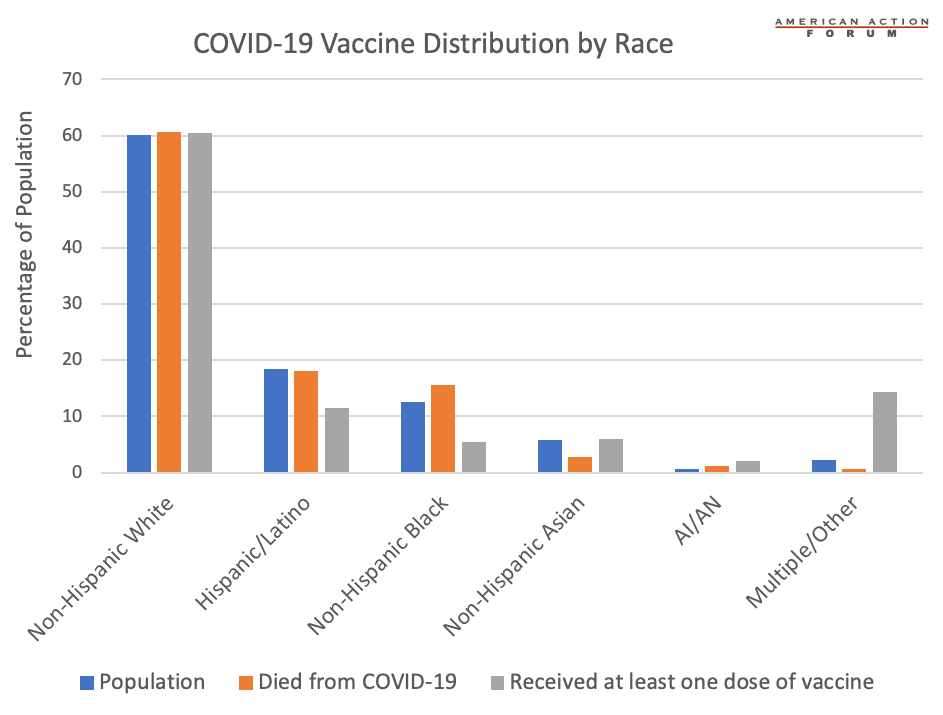

Chart Review: COVID-19 Vaccine Distribution by Race

Alexis Williams, Human Welfare Policy Intern

Many have noted the disparate impact the coronavirus pandemic has had on communities of color, and early data suggest there may also be unequal distribution of the vaccine among some minority populations. As shown in the chart, two minority groups, Hispanic/Latino and Non-Hispanic Blacks, are proportionately underrepresented in the vaccine distribution, while Non-Hispanic Asians and American Indians and Alaska Natives (AI/AN) have received the vaccine at rates in line with or higher than their proportion of the population. This discrepancy between the groups is likely in part because Asian-Americans make up a relatively high number of hospital workers, who were the first to receive the vaccine. That said, 16 percent of health care workers are Non-Hispanic Blacks, a rate higher than their proportion of the population and their share of COVID-19 deaths. Moreover, Black women make up a high percentage of staff in long-term care facilities (26 percent) and therefore should have been among the first to receive the vaccine, but only 5.4 percent of vaccine recipients to date are Non-Hispanic Blacks. Surveys suggest that Black Americans are skeptical about the safety and efficacy of the vaccine, which could lead them to decline it. Nevertheless, some of these discrepancies are likely accounted for in the second-highest category, “Multiple/Other.” These data do not account for vaccinations given after the first month and only include racial data for 52 percent of individuals vaccinated.

Sources: Centers for Disease Control and Prevention Morbidity and Mortality Weekly Report and National Center for Health Statistics

Worth a Look

Wall Street Journal: Hospitals Suffer New Wave of Hacking Attempts

Reuters: Britain explores mixed COVID vaccine shots as variants threaten