Weekly Checkup

October 25, 2019

Parsing the Competing Narratives on the Affordable Care Act

This week the Administrator for the Centers for Medicare and Medicaid Services (CMS), Seema Verma, appeared before the House Energy and Commerce (E&C) Committee to discuss — what else? — the Affordable Care Act (ACA). The occasion was open enrollment beginning on November 1 for 2020 plan-year insurance sold through the ACA’s insurance exchanges. Once again, the law’s supporters and opponents are arguing about that now age-old question: Is the Trump Administration gutting or saving Obamacare?

If the question is straightforward, the competing narratives from the left and right are not. Yes, ACA supporters want to make the case that President Trump has been waging war on the ACA, seeking to undercut it at every turn. But they still want to argue that, despite the president’s efforts, the law is fundamentally sound—in need of improvement and expansion, certainly, but in no way fatally flawed. The Trump Administration is also making two somewhat divergent arguments. On the one hand, officials argue that under the president’s stewardship, the market created by the law is improving: Premiums are coming down and competition is increasing. On the other hand, the president continues to rail against what he argues is a flawed law and failing policy. So, what’s the reality?

Start by considering the data. In advance of the E&C hearing, CMS released some details on what the ACA market will look like in the 38 states that utilize the federally facilitated marketplace. Premiums for the benchmark Silver plan will decrease on average by 4 percent, compared to an average decrease last year of 1 percent. AAF’s analysis of Silver benchmark premiums for all 50 states and the District of Columbia found that premiums increased on average by just 1 percent in 2019, but premium data for states not using the federally facilitated marketplace is not fully available yet. Additionally, in those same 38 states the number of insurers offering coverage has increased from 155 in 2019 to 175 in 2020, and the average enrollee will be able to choose from 3 to 4 different insurers in 2020, compared to 2 to 3 in 2019. In 2020 only 12 percent of enrollees will have access to only 1 insurer, down from 20 percent in 2019.

In other words, the data on the whole indicate that competition is increasing and premiums have decreased for the second straight year. Prior to 2019, double-digit premium increases were the norm. Of course, averages mask variation: In Delaware benchmark premiums will decrease by 20 percent, while enrollees in Indiana will see a 13 percent increase. Still, it is clear that the Trump Administration has overseen a period of stabilization and even slight improvement in the ACA marketplace.

At the same time, the administration has taken actions to create an individual marketplace in line with the president’s policy objectives of choice and competition, promoting short-term limited-duration insurance plans (STLDIs), expanding access to association health plans, and ending cost-sharing reduction (CSR) payments to insurers. Some of these policies—such as ending CSR payments—have had dramatic negative impacts on premiums, but most of the administration’s policies aimed at expanding choice and offering lower cost options have had minimal effect on the health of the marketplace either way. Supporters of the ACA may oppose STLDIs on principle, but the argument that they’ve hurt the individual market or undermined the ACA falls flat so far.

Still, there is also the question of whether the Trump Administration’s actions are aimed at undercutting the ACA. Again, signals are mixed here. The Justice Department’s decision not to defend the law clearly aims at its complete dismantling, and the president himself still openly supports repeal. It is inarguable that the Trump Administration is seeking to overturn the ACA. That said, the data indicate that CMS’s management of the individual market under President Trump has been effective and has not had a detrimental impact on the marketplace (with the exception of the CSR decision). Both sides care about improving the individual market. The fight is about who gets credit.

Chart Review

Jonathan Keisling, Health Care Policy Analyst

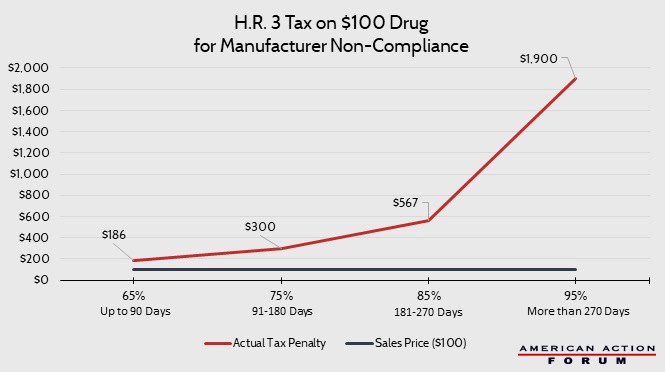

H.R. 3, “The Lower Drug Costs Now Act of 2019,” requires manufacturers to negotiate the price of certain drugs with the Secretary of Health and Human Services, and if the manufacturer does not comply, the bill would impose an excise tax on the sales of the manufacturer. This tax has been portrayed as equaling a percentage of sales that ranged from 65 percent for the first 90 days of non-compliance to 95 percent for any period greater than 270 days. These rates, however, do not accurately reflect the penalty that will be assessed. These rates are proportions that are then used to determine the actual tax rates. These rates range from 186 percent of sales for the first 90 days of non-compliance to 1,900 percent of sales after 270 days of non-compliance.

Worth a Look

Modern Healthcare: UPS and CVS launch new drone delivery deal

New York Times: Two Strains of Polio Are Gone, but the End of the Disease Is Still Far Off