Weekly Checkup

June 14, 2019

Reviewing the Trump Administration’s Health Insurance Actions

This week the Trump Administration finalized a rule expanding the allowable uses for Health Reimbursement Arrangements (HRAs). This rule is the third action—following a rulemaking on Association Health Plans (AHPs) and Short-Term Limited-Duration Insurance Plans (STLDIs)—coming out of the president’s October 2017 executive order “Promoting Healthcare Choice and Competition Across the United States.” Over a year and a half after the executive order was issued, this week’s action provides a good opportunity to review the effort.

First, the administration finalized a rule just shy of a year ago expanding the use of AHPs. Prior to the rulemaking, membership in a given AHP was limited to businesses in the same industry. AHPs allow various groups to join together, potentially across state lines, for the purpose of getting a better deal on health insurance. At the time, supporters of the Affordable Care Act (ACA) criticized the rule as an attempt to undermine the law’s health-insurance marketplace. These concerns appear to have been overstated, as between January and March of this year more than 30 new AHPs were established, covering at least 30,000 beneficiaries with little to no appreciable effect on enrollment in the ACA marketplace. The AHP effort hit a snag in March, however, when a U.S. District Court blocked most of the rulemaking on the grounds that it was an “end-run around” the ACA. The Department of Labor has appealed the ruling, and in the meantime the newly established AHPs are blocked from taking on new enrollees and no further AHPs can be formed.

Also last summer, the Trump Administration finalized rulemaking expanding the availability of STLDIs. Traditionally, STLDIs provide temporary coverage for individuals who have a short break in health insurance. Because these plans are outside of the ACA’s regulatory framework, however, they don’t have to conform to the ACA’s rules regarding benefit design and coverage requirements. They also aren’t subject to the ACA’s guaranteed issue requirements or the ban on preexisting condition exclusions. The Obama Administration restricted STLDIs to a duration of less than three months, and insurers were barred from renewing them when they expired. The Trump Administration allowed STLDIs to be issued for up to 364 days. Additionally, and importantly, STLDIs are now renewable—at the discretion of the issuer—for up to 36 months. Once again, outraged supporters of the ACA claimed this rulemaking was aimed at undermining the ACA marketplace, and once again the policy change does not appear to have had a negative impact on the ACA marketplace.

Now, the Trump Administration has finalized this rulemaking expanding HRAs. Before the ACA, HRAs allowed employees to use tax-preferred dollars to purchase individual market insurance or a la carte health care services; the ACA outlawed most uses of HRAs. The new rule allows employees to use HRA funds to purchase ACA-compliant individual market insurance and contains stipulations intended to prevent employers from moving less healthy employees onto the individual market. Of note, the Treasury Department’s modeling indicates that as many as 7 to 8 million individuals could enter the ACA marketplace over the next decade as a result of this rule and finds that if the health status of these individuals tracks that of the rest of the group market, the impact could be a 3 percent decrease in marketplace premiums.

Each of these proposals are still early in their rollout, and the AHP changes could still ultimately be thwarted by the courts. But the potential for these policy changes to positively impact choice and premiums is clear, and the predicted negative impacts have yet to materialize. Only time will tell, but if the administration’s goal is to increase coverage while reducing costs, for now it looks to be on the right track.

Chart Review

Ryan Haygood, Health Care Policy Intern

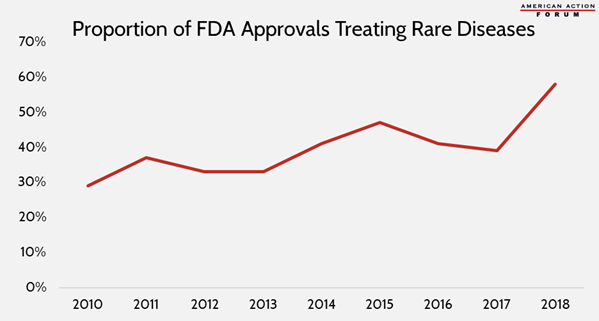

The Orphan Drug Act of 1983 began a reorientation of U.S. drug development toward smaller target populations by incentivizing and financing therapies for rare diseases (those affecting 200,000 people or fewer). Despite a relatively high development success rate of 26 percent, they often come with extraordinary price tags of hundreds of thousands of dollars per patient—partially because, by definition, there are few beneficiaries over which to spread the high cost of development. Interest in rare disease development has swelled even further in recent years, with orphan drugs making up 59 percent of FDA approvals in 2018. These trends are likely to progress as next-generation biotherapeutics, including gene and cell therapy, begin coming to market—although the FDA approved a gene therapy for the first time only in 2017, 269 such drugs are now in late-stage development, up from just 120 in 2015.

From Team Health

The AAF Exchange – Ep. 04: Drug Pricing in the United States

In AAF’s Podcast, Christopher Holt explains what factors impact drug pricing and analyzes the various proposals to lower drug prices.

The Impact of Shifting Rebates to Catastrophic Coverage in Medicare Part D

AAF’s Deputy Director of Health Care Policy Tara O’Neill Hayes examines how shifting drug rebates to the catastrophic phase of insurance would affect different stakeholders.

Worth a Look

The Atlantic: The Worst Patients in the World

Axios: Study: Medical marijuana may not help alleviate opioid crisis