Weekly Checkup

August 16, 2019

The State of the Individual Health Insurance Market

This week, the Centers for Medicare and Medicaid Services (CMS) released two reports detailing insurance coverage in the individual market: first, a snapshot of Affordable Care Act (ACA) exchange enrollment as of February, and second, an analysis of individual market enrollment trends both on and off the ACA exchanges. The key takeaway from the two reports is that the ACA exchanges show evidence of stabilizing, while trends in the broader individual market provide cause for concern.

Looking at the figures for the exchanges, the marketplace appears to be, at least on average, relatively settled. The total number of exchange enrollees who had signed up for a plan and paid their first month’s premium in February 2019 was 10.6 million, down just over 60,000 from February 2018—not a big drop. Eighty-seven percent of exchange enrollees received a premium subsidy, the same as in 2018, and 52 percent of enrollees were eligible for cost-sharing reduction (CSR) payments from insurers, compared to 53 percent in 2018—again, steady as she goes. Additionally, previous AAF analysis found that the average 2019 benchmark Silver plan premium was only 1 percent higher than the average 2018 benchmark plan premium. The lowest-cost 2019 Bronze plan premium in each rating area was also up an average of just 1 percent over 2018, though the lowest-cost Gold plan premium increased 14 percent on average between 2018 and 2019.

At the same time, total individual market coverage—including both people who purchase insurance outside of the exchange as well as through it—declined by 2.4 million from 2016 to 2018. This drop in overall individual market coverage is the result of individuals who do not qualify for premium subsidies leaving the individual market over that period. In response, CMS Administrator Seema Verma raised the alarm, saying, “People are fleeing the individual market. Obamacare is failing the American people, and the ongoing exodus of the unsubsidized population from the market proves that Obamacare’s sky-high premiums are unaffordable.”

Without a doubt it is true that rising premiums both on and off the exchanges are driving the exodus of unsubsidized Americans from the individual market. These premium hikes are due first—and primarily—to the ACA’s insurance market reforms and, more recently, to the Trump Administration’s decision to cease reimbursement to insurers for CSRs. At the same time, the data are a bit more complicated than it might first appear. For example, while there were 2.5 million fewer unsubsidized enrollees in the individual market as a whole in 2018 than in 2016, the number of unsubsidized enrollees through the ACA exchanges only dropped by 293,000 over that period. Additionally, according to the administration’s analysis there were still more unsubsidized individuals in the individual market in 2018 than there were in 2014, though just barely.

Overall, there were fewer enrollees in the individual market on and off exchange in 2018 than in any other year since 2014, but whether that decline will continue is harder to predict. The danger, of course, is that as there are fewer unsubsidized and comparatively healthier individuals in the market, there will be more upward pressure on premiums, which in turn would drive up federal subsidy spending. The Trump Administration has been moving to provide low-cost insurance options to individuals who don’t qualify for subsidies, but it’s too soon to see what effect those policy efforts will have. Overall, the reports paint a picture of an ACA marketplace that is mostly static, while trends in the broader individual market could potentially indicate future instability.

Chart Review

Ryan Haygood, Health Care Policy Intern

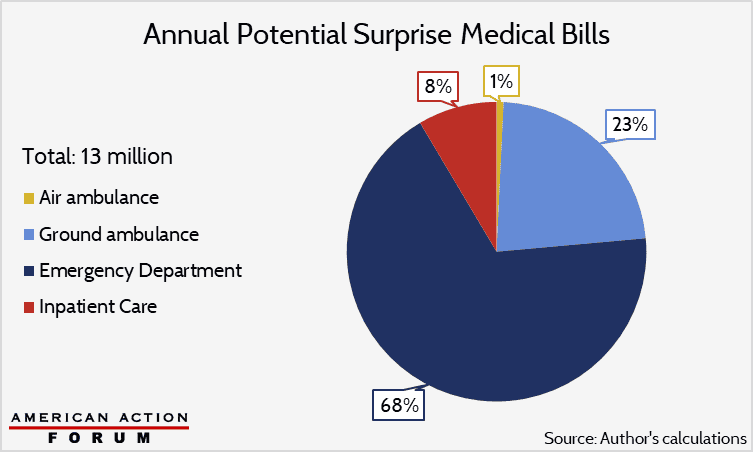

Last week, the Weekly Checkup highlighted Wyoming’s proposal to end surprise air ambulance bills, which cost much more than other types of surprise bills and occur on 69 percent of all trips – a higher fraction than in any other medical setting. Taking surprise billing as a whole, however, air ambulances account for just 1 percent of all such bills. The lion’s share comes from the emergency room: While only about one-fifth of ER visits may incur surprise bills, the ER is responsible for two-thirds of them by volume. The potential annual volume of surprise bills sits at about 13 million, according to my evaluation of them across four medical settings, using estimates of surprise–billing incidence from 2014 to 2017. Each “potential” case involves a high risk of receiving a surprise bill from an out-of-network provider, although the extent of balance billing (i.e. charging the patient the listed out-of-network price) for these services is difficult to estimate. Also hard to measure is the incidence of potential surprise bills, with a study out this week finding double the rate of ER and inpatient surprise billing found by others. My estimate uses the lower of these figures and also excludes potential bills from out-of-network facilities and neonatal care, making it a lower-bound approximation.

From Team Health

Daily Dish: Considering the Effects of a Medicare Buy-In

Health Care Policy Analyst Jonathan Keisling examines the consequences of implementing a Medicare Buy-In plan.

Worth a Look

The Atlantic: Lyme Disease Is Baffling, Even to Experts

Axios: The dire state of rural mental health care