Weekly Checkup

October 30, 2020

Would a President Biden Fix Medicare’s Cash Shortfall?

Earlier this year, the Medicare Trustees reported, for the second year in a row, that Medicare’s Hospital Insurance Trust Fund (Part A) will become insolvent in 2026. More recently, the Congressional Budget Office (CBO) projected that the economic contraction instigated by the COVID-19 pandemic has accelerated the timeframe, and Medicare Part A will reach insolvency by 2024. If corrective action is going to be taken to shore up the Medicare program, it will need to happen on the watch of whoever wins next week’s election. Joe Biden may be particularly well positioned to address this problem, but his calls for lowering the Medicare eligibility age from 65 to 60 suggest he’s not inclined to take on the challenge.

While Congress and the next administration will have to act in the next four years, this reckoning has been long coming. Apart from 1966 and 1974, Medicare has spent more on benefits than it has taken in through premiums and payroll taxes every year of its existence. Medicare’s cumulative cash shortfall since enactment is $5.5 trillion, and its shortfall in 2019 was 40 percent of the overall deficit. While the problem is mounting, President Trump has been explicit since announcing his 2016 campaign that he will not undertake any changes to the Medicare program aimed at shoring up its finances.

A theoretical President Biden, however, might be uniquely positioned to lead Medicare reform efforts. It seems almost certain that Biden would not seek a second term as president if he prevails next week. Turning 78 a few weeks after the election, Mr. Biden will already be by far our oldest incoming president. And the former vice president has promoted himself as a transitional figure, providing stability and a return to norms while paving the way for a new generation of Democratic political leaders. Biden would not have the pressure of facing primary or general-election voters again, nor given his relative age and financial situation would he need to be particularly worried about post-presidential employment. Hard choices—in the form of benefit changes, increased revenue, or more likely both—will need to be made no matter how policymakers choose to address Medicare’s financing, and it’s likely that both ends of the political spectrum would be unhappy with any compromise that addresses the challenge. Similar to the way John Boehner sought to “clear the decks” of controversial issues facing Congress before handing over the Speaker’s gavel to Paul Ryan, Biden could see his role as taking the hits to protect the next round of Democratic leaders from having to make those hard choices on entitlements. In effect, addressing long-term entitlement financing could be an “only Nixon could go to China” moment for Biden if he wanted it.

Unfortunately, candidate Biden has shown no inclination to face reality when it comes to Medicare. At a time when some have called for increasing the Medicare eligibility age to account for both increasing lifespans and the program’s increasing costs, Biden is promising to lower the Medicare eligibility age to 60. Lowering the Medicare age is consistent with Biden’s focus, and that of Democrats broadly, on increasing insurance coverage rather than reducing health care costs. Ironically, however, lowering the Medicare age is unlikely to do much to reduce the number of uninsured. Of the 22.7 million people who would be newly eligible for Medicare under Biden’s proposal, only 1.7 million are currently uninsured. Almost all of the increase in the Medicare population would come from people shifting from other types of coverage. In addition to driving up Medicare costs and accelerating Part A insolvency, moving people from private insurance coverage to Medicare will impact health care providers who are paid less by Medicare.

Whoever wins next week’s election, the game of entitlement-spending hot potato is going to end on his watch. President Trump, the self-proclaimed King of Debt, has given every indication he’ll ignore the problem by just taking on more debt. A President Biden would have an opportunity to rise to the challenge, but so far he appears inclined to follow Trump’s lead, with a little more spending tacked on while he’s at it.

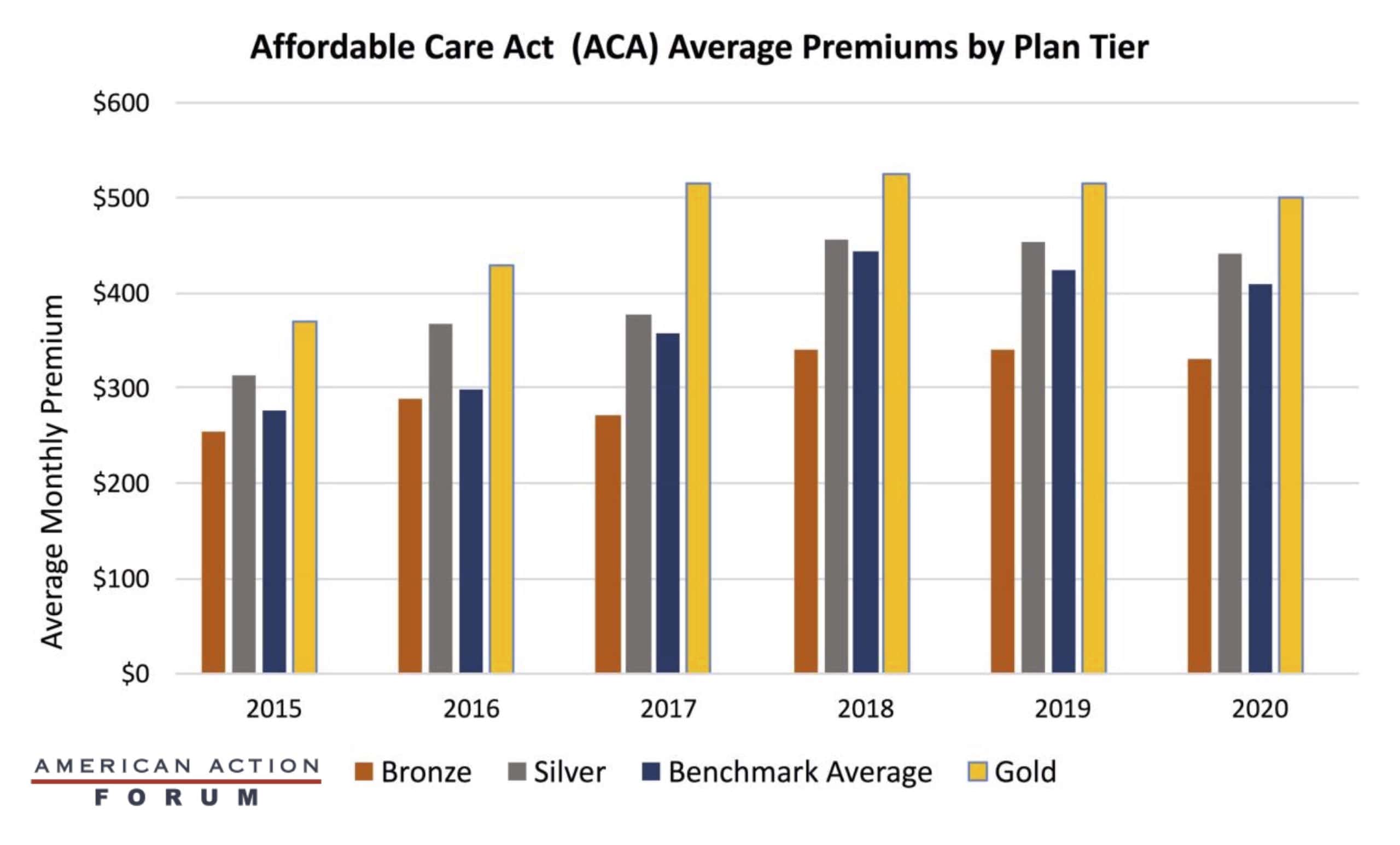

Chart Review: Premium Trends Under the Affordable Care Act

Julia Demeester, Health Care Policy Intern

The Affordable Care Act (ACA) was intended to reduce the cost of health insurance coverage for individuals who qualify, but as the chart below shows, prices have struggled to become more affordable. Premiums steadily increased between 2015 and 2018, but they then began to drop in 2019 and 2020 and are expected to follow the same trend for 2021. While a number of factors have contributed to the stabilization of premiums, it is notable that the ACA marketplaces have stabilized during the Trump Administration, as Christopher Holt noted last week. More competition could drive down prices this coming plan year: The Centers for Medicare & Medicaid Services expects that more insurers will participate during this plan year.

Data from the Kaiser Family Foundation (tiers and benchmarks) and HealthCare.gov

Worth a Look

FierceHealthcare: Trump administration finalizes rule forcing payers to post negotiated rates, cost-sharing data

New York Times: Death Rates Have Dropped for Seriously Ill Covid Patients