The Daily Dish

March 18, 2022

Inflation and Supply Responses

Inflation is the hot economic topic, and there is a keen interest in finding the silver bullet that tames inflation quickly and easily. In principle, it is easy to find the silver bullet: just dramatically expand supply. With greater supply there is (by definition) more of the good that is suddenly so valuable and, because there is more to go around, the upward pressure on price per unit diminishes. Voila! Inflation is tamed.

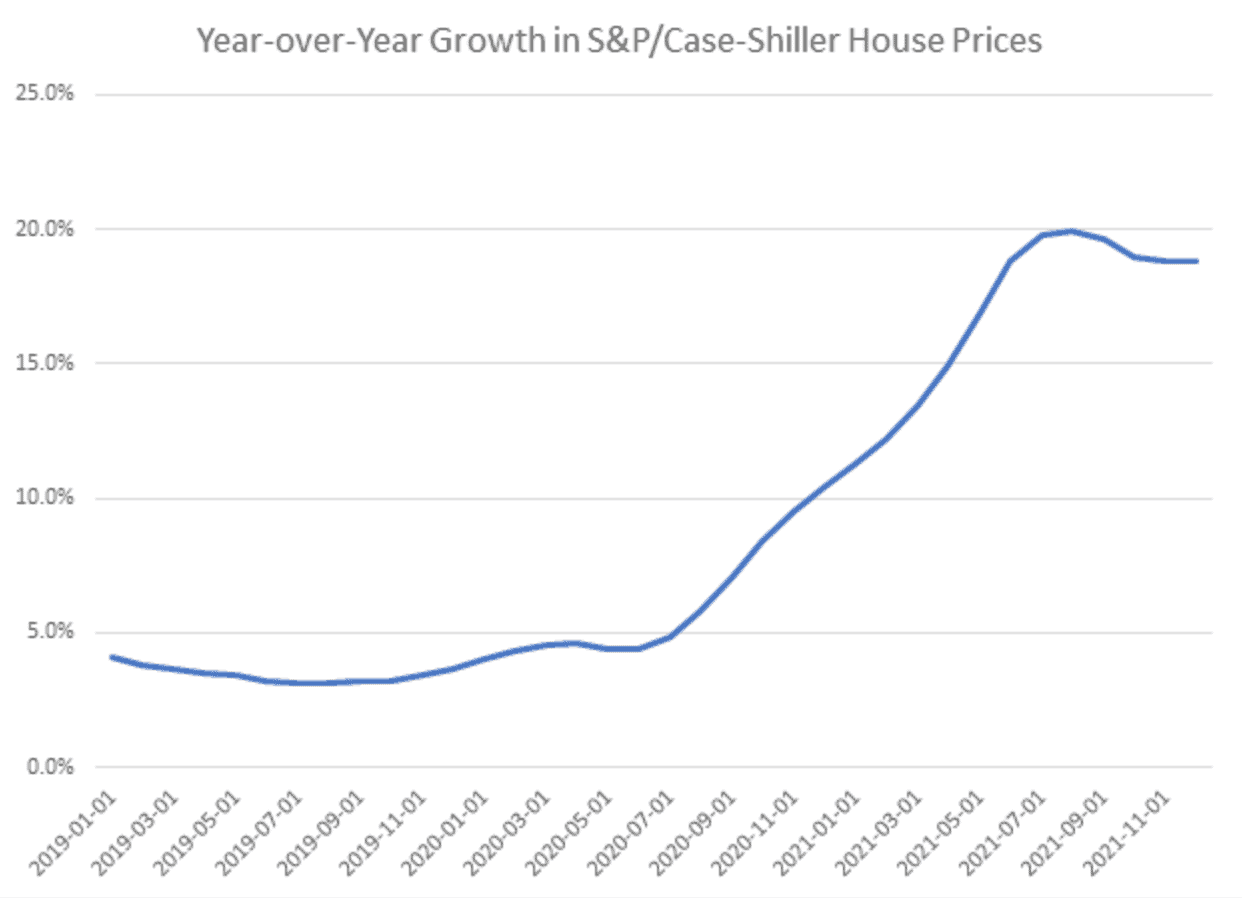

In practice, this is essentially impossible to do. Consider housing. Inflation on shelter costs – which are about one-third of the Consumer Price Index – has risen from 1.6 percent in January 2021 to 4.7 percent at present. That’s a very importantpart of the inflation problem, and it reflects the very sharp rise in housing prices. The year-over-year growth in the nationwide S&P/Case-Shiller house price index is shown in the graph below, and the dramatic run-up in 2021 is obvious.

Ok. Those high prices should be an incentive for homebuilders to construct more units of housing. And they were. As seen below, there was an enormous boom in housing starts (orange line) and housing completions during mid-2021. Starts tailed off but remained up 10 percent year over year. Completions were a bit weaker.

So, qualitatively, this is exactly what one would hope for in order to tame the house-price inflation. Unfortunately, the impact is trivial. Even with the boom in starts, the total stock of housing units is up by only 0.2 percent in the final quarter of 2021.

The moral is that it is hard to move substantially the supply capacity of a large economy like that of the United States, either for a big industry like housing or the economy as a whole. As a result, controlling inflation requires slowing the growth of demand. For housing markets, mortgage interest rates topped 4 percent for the first time since 2019. That should begin to diminish demand and tame price pressures. For the economy as a whole, the Fed has embarked on a regime of higher interest rates in order to get inflation under control.

The risk, of course, is that the Fed can overdo it and cause growth to cease or turn negative. This is the dilemma of inflation-fighting: Supply-side policies are unambiguously good news, but too small to matter much quickly, while demand-side policies will work but run the risk of working too well.

Fact of the Day

Since January 1, the federal government has published rules that imposed $3.2 billion in total net cost savings and 12.4 million hours of net annual paperwork burden increases.