Insight

February 19, 2026

401(k)-funded Down Payment: Making the Problem Worse

Executive Summary

- Americans name “affordability” as a top concern in public opinion polling, spurring policymakers to propose a plethora of initiatives to address the problem – among them an administration and congressional proposal to allow prospective buyers to access their 401(k)-retirement savings for a down payment on a home.

- Like many “affordability solutions,” however, both initiatives would boost demand without increasing supply, which could undermine housing affordability objectives by putting upward pressure on home prices, while posing a significant risk to long-term financial security.

- If policy makers are serious about addressing home affordability – in other words, lowering the cost of homes – they need to focus on the myriad federal and local policies that restrict housing supply.

Introduction

The issue of affordability is more than just the latest buzzword in Washington. It reflects enduring discontent among Americans that has pressured the Trump Administration and Congress to scramble to address the high cost of living.

A key topic in the affordability discussion is that homeownership appears increasingly out of reach for so many, particularly younger, individuals. In an attempt to address this concern, the White House and a member of Congress developed separate plans to allow prospective buyers to access their 401(k)-retirement savings for a down payment on a home without facing tax penalties.

Yet like many “affordability solutions,” these initiatives would boost demand, which could ultimately undermine housing affordability objectives by putting upward pressure on prices. Moreover, allowing households to draw upon retirement savings to purchase a home poses significant risks to long-term financial security that could leave purchasers overinvested in housing relative to other forms of wealth.

If policy makers are serious about addressing home affordability – in other words, lowering the cost of homes – they need to focus on increasing supply, and specifically the myriad federal and local policies – such as local zoning restrictions, federal immigration policy and tariffs – that raise construction costs and ultimately reduce supply.

Rising Cost of Home Ownership

Affordability is among Americans’ top economic concerns, according to recent Gallup polls. A poll conducted by Public Opinion Strategies on behalf of the National Association of Realtors (NAR) found that 52 percent of voters say housing affordability is a “very important voting issue,” while 85 percent call home ownership “an essential part of the American dream.” Yet the majority of Americans feel home ownership is out of reach, according to a 2024 survey from Citi. This concern has placed pressure on policymakers to respond.

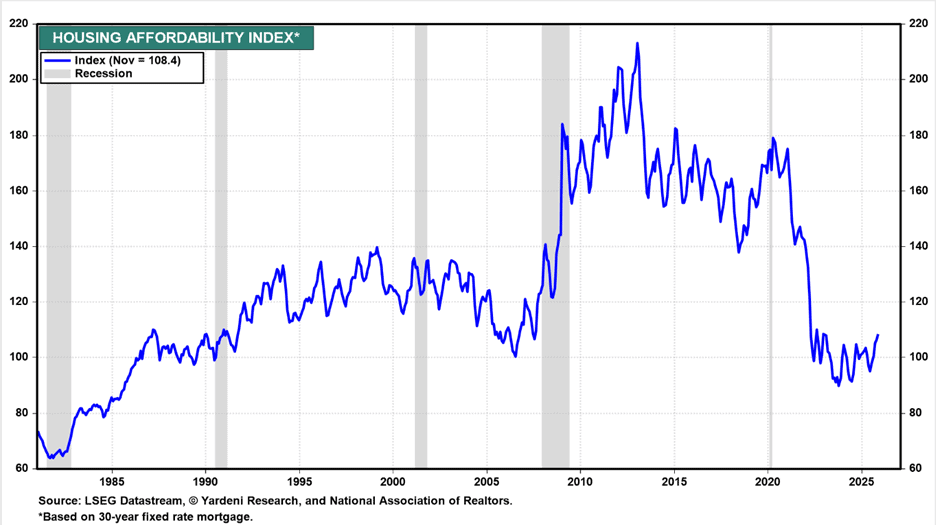

The data substantiate these claims. Data from Yardeni Research and NAR show that NAR’s housing affordability index – a measure of whether a typical family earns enough income to qualify for a mortgage loan on a median-priced, existing single-family home – plummeted in the years following the COVID-19 pandemic and remains near its lowest levels since just prior to the 2008–09 financial crisis (Figure 1).

Figure 1. Housing Affordability Index

Source: Yardeni Research; lower index value indicates less affordability

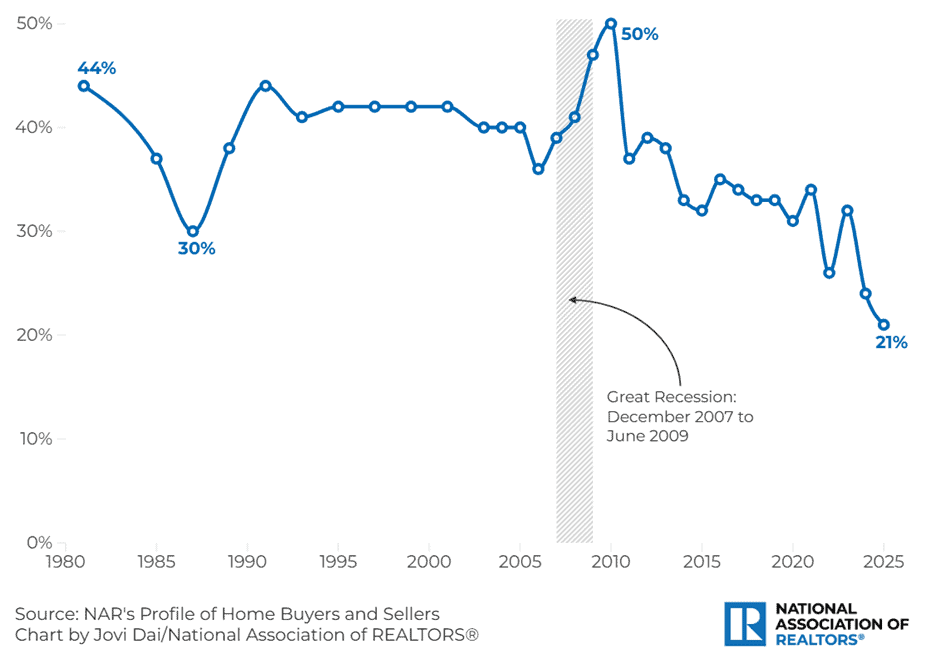

Affordability challenges are particularly dire for first-time home buyers. NAR data show that the first-time home buyer affordability index was 66.9 in Q3 2025 compared to the overall index of 101.0. In addition, NAR’s annual survey of home buyers and sellers who completed a transaction between July 2024 and June 2025 found that first-time home buyers made up just 21 percent of all buyers – an all-time low (Figure 2). Historically, first-time home buyers represented about 40 percent of home sales.

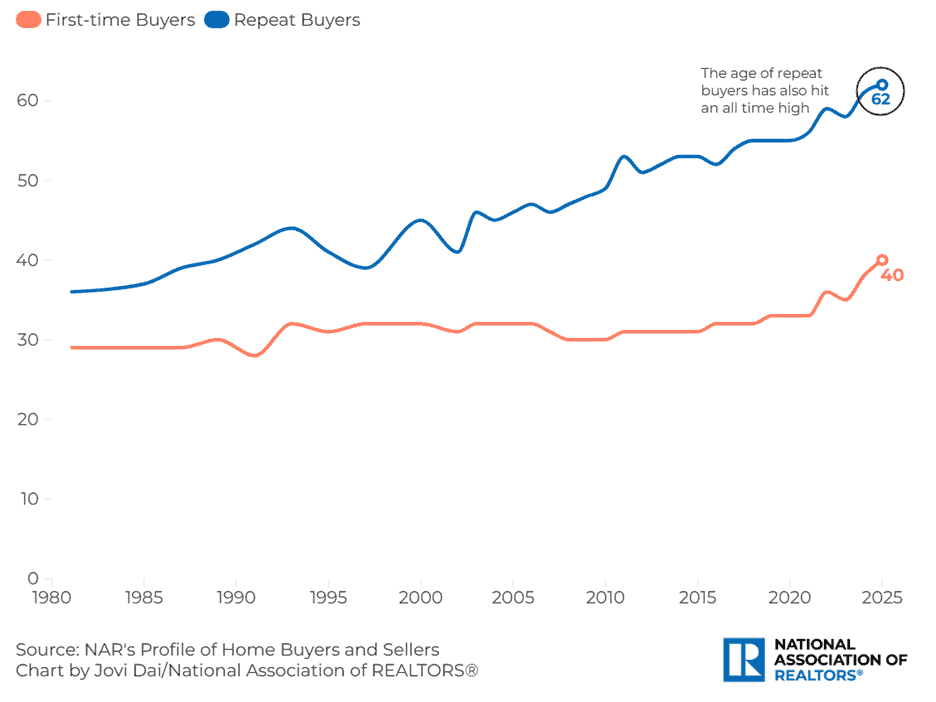

At the same time, the median age of first-time buyers climbed to 40, also an all-time high. Between 1987–2015, the median age of a first-time home buyer fluctuated between 28–31 years old before rising steadily in recent years (Figure 3).

Figure 2. Share of First-time Home Buyers

Source: National Association of Realtors

Figure 3. Median Age of Home Buyers

Source: National Association of Realtors

NAR also reported that the median down payment reached 10 percent in 2025, matching the level last reached in 1989 and up from 7 percent in 2020. A down payment of 10 percent on the median price of an existing single-family home would translate to about $43,000 in Q3 2025, or just over $36,000 for a starter home.

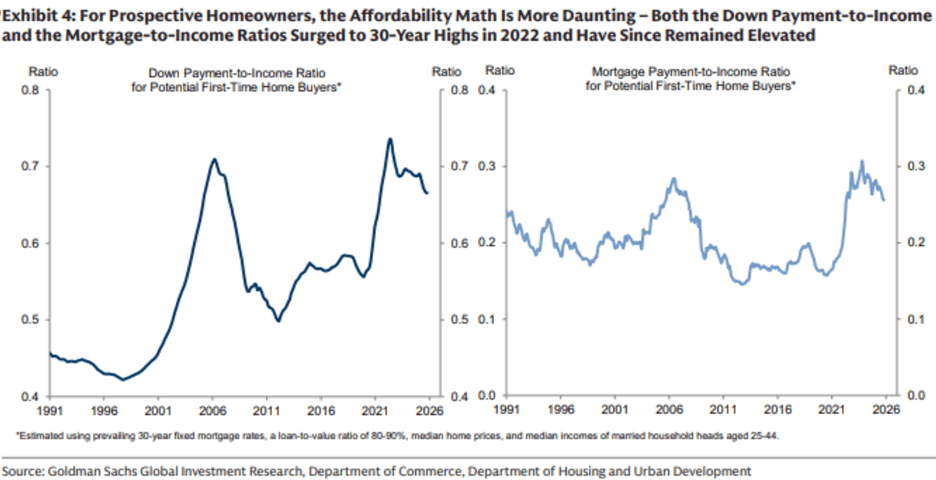

A recent Goldman Sachs analysis found that both the down payment-to-income and the mortgage-to-income ratios surged to 30-year highs in 2022 and have remained elevated. The firm noted that “for young married couples considering buying their first home, the average down payment is now 70% of their annual household income (vs. 58% in 2019 and 45% in 2000), and the first-year mortgage payment is about 25% (vs. 18% in 2019 and 20% in 2000).”

Source: Atlas Capital

National Economic Council Director Hassett acknowledged these trends, stating that “The typical monthly payment about doubled for an ordinary family buying an ordinary home. And the down payment they needed to buy a home went from about $15,000, to about $32,000.”

Down Payment Funds and Retirement Savings

Source of Funds

According to NAR’s annual survey, 26 percent of buyers used financial assets – 401(k)s, IRAs or stocks – for down payments. Among first-time home buyers, 59 percent relied on personal savings, and 22 percent received help from relatives or friends through a gift or a loan.

White House and Congressional Plans

Director Hassett initially announced that the administration was exploring a policy that would allow potential buyers to tap their 401(k) to make a down payment on a home. The proposal was quickly abandoned, however, after President Trump conveyed skepticism, stating “I’m not a huge fan.”

While the White House has, for now, discarded the idea, Representative John McGuire (R-VA) introduced the Home Savings Act that would amend the Internal Revenue Code to permit tax free withdrawals from a 401(k) when the funds are used for a down payment or closing costs on a primary residence. The plan would also allow the same penalty-free withdrawal and allow the individual to gift those funds to a relative, exempt from gift tax, provided the relative uses the money for a down payment or closing costs on a primary residence.

401(k)s

A 401(k) – named for the section of the tax code that created it – is an employer-sponsored retirement savings plan that receives preferential tax treatment. These plans allow employees to contribute part of each paycheck into the retirement account and invest the assets. Moreover, employers can make contributions to these accounts to supplement retirement savings. Unlike regular brokerage accounts, traditional 401(k)s allow you to make pre-tax contributions. These contributions, and all the gains, are taxed once the funds are withdrawn in retirement. There is also a Roth 401(k), in which after-tax dollars are contributed to the account and withdrawals during retirement are tax free.

Under existing law, there are several options for individuals to use both types of 401(k) savings as a down payment. According to Northwestern Mutual, an individual could take a 401(k) distribution. This would require the individual pay income tax on any pre-tax dollars, and, if that person is younger than 59 ½, it is likely to be deemed an early withdrawal and subject to an additional 10 percent penalty. It is possible to withdraw only contributions from the Roth 401(k) without prompting taxes and penalties.

Another option would be to take a 401(k) loan. An individual may be able to borrow up to $50,000 or 50 percent of the vested value of the account, whichever is less. This maximum is outlined in Internal Revenue Code 72, but plan-specific loan amounts can often be less. In this scenario, the borrower would have to repay the loan, plus interest. Borrowing from a 401(k) does not trigger early withdrawal penalties or income taxes under most conditions.

Alternatively, individuals seeking to use 401(k) savings to pay for a down payment on a home could take a hardship withdrawal – which the IRS defines as an emergency removal to cover “an immediate and heavy financial need,” according to Rocket Mortgage. A hardship is determined by one’s employer. These withdrawals are subject to the 10-percent early withdrawal penalty and income tax.

Are 401(k) Funds Even Enough?

NAR data showed that first-time home buyers face down payment requirements of approximately $36,000–$43,000. Data from Vanguard, however, suggest existing 401(k) balances may be insufficient to cover these costs using current withdrawal options. The median 401(k) balance for those between 35–44 – roughly the median age of a first-time home buyer – was just under $40,000.

Using the loan option previously discussed, an individual could borrow $20,000 (50 percent of the account value), assuming full vesting. A full distribution of $40,000 would incur about $9,600 in federal taxes (assuming the 24-percent tax bracket), and a $4,000 early withdrawal penalty, leaving only $26,400 available for a down payment.

The Home Savings Act would mitigate some of this shortfall by exempting a qualified 401(k) distribution from gross income. In other words, the distribution would not be taxed. The bill does not exempt such distributions from the early withdrawal penalty.

Tradeoffs and Alternatives

Tradeoffs

Given current statistics on 401(k) balances and down payment requirements, the proposal is unlikely to meaningfully help individuals overcome the down payment hurdle. Moreover, it represents yet another demand-side solution. Fueling demand without increasing supply will only push home prices higher, further exacerbating the housing affordability problem.

The proposal also carries federal budgetary and individual-level tradeoffs. Allowing pre-tax contributions to be withdrawn tax-free would reduce federal revenues. At the individual level, potential homeowners would face a choice between drawing down retirement savings to purchase a home, which could weaken long-term financial security, and delaying a home purchase.

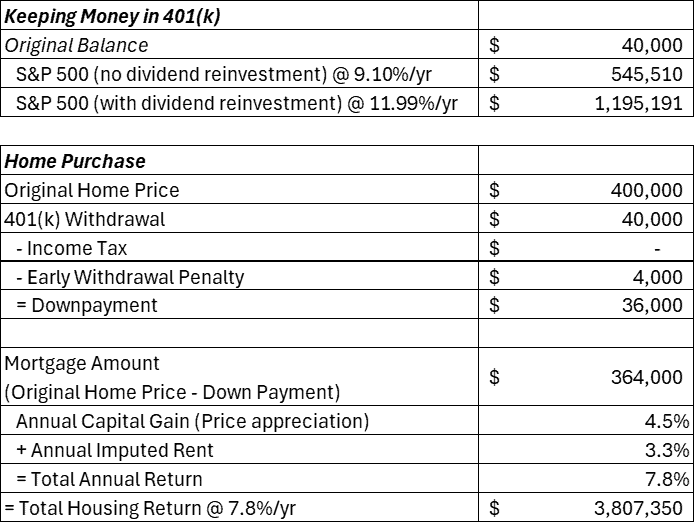

Historical returns of the S&P 500 – a stock market index that tracks the performance of 500 of the largest publicly traded companies – averaged 9.10 percent per year over the past 50 years excluding dividend reinvestment, or 11.99 percent when dividends are reinvested. By comparison, the S&P Cotality Case-Shiller U.S. national home price index showed just a 4.5-percent average increase in home prices since 1988. Yet home price appreciation is only one component of total housing returns. Owners’ equivalent rent – which is a measure of the amount of money a homeowner would have to pay to rent to substitute for the home – must also be considered. The Bureau of Labor Statistics reports that the owners’ equivalent rent of a primary residence has averaged roughly 3.3 percent per year since 1988.

To put these returns into perspective, consider a simplified example assuming a $36,000 down payment on a $400,000 home. This calculation excludes taxes on the sale of a home and in-retirement withdrawals from a traditional 401(k), and is calculated over a 30-year horizon.

The example shows that the annual rate of return of the S&P 500 – both with and without dividend reinvestment – generally outpaces the annual rate of return on a home purchase. Yet leverage – purchasing a $400,000 asset with just $40,000 – can produce a larger total dollar return relative to the initial investment. While this may make housing appear to be a superior investment, retirees cannot “eat their house.” In other words, using 401(k) funds for a down payment substitutes highly liquid assets for an illiquid home. Housing cannot readily provide the cash flow needed for daily expenses.

Concentrating too much wealth in housing introduces significant diversification risk. Home prices fluctuate across local markets, and a sudden decline in home prices could sharply reduce household wealth. Additionally, holding too much wealth in housing exposes homeowners to increased costs, including rising property taxes, insurance premiums, and maintenance expenses, which tend to increase as home prices appreciate.

Alternatives

Rather than changing the existing tax code governing 401(k) accounts – which could ultimately change its intended purpose – Congress could create an entirely new savings vehicle specifically for down payments. Legislation introduced by Representatives Suhas Subramanyam (D-VA) and Ashley Hinson (R-IA) seeks to do just that. The First Home Savings Opportunity Act establishes tax-deductible first-time home buyer savings accounts. The bill would allow participants to contribute up to $10,000 per year tax-free ($20,000 for joint filers) to a savings account. These funds would be used exclusively for a down payment and closing costs on a first home.

This approach, however, introduces a second tax benefit for owner-occupied housing. Selling a home already receives preferential treatment on the capital gains tax. Single filers can exclude up to $250,000 and married couples up to $500,000 upon the sale of a primary residence. This exemption would now be coupled with a similar treatment at the front-end of the housing transaction.

More broadly, current policy prescriptions largely stimulate demand. Policymakers would likely make more impactful progress on housing affordability by addressing supply-side constraints. Local zoning restrictions, immigration policy, and tariffs all raise construction costs that are ultimately passed on to home buyers.

Conclusion

Proposals that allow access to 401(k) retirement savings for home down payments come with significant long-term risk to the financial well-being of individuals. Moreover, these proposals are part of a growing list to address housing affordability from the demand-side of the equation.

Rather than diminish the integrity of retirement plans such as the 401(k), Congress – if it absolutely must focus on increasing demand – would do better to create a new savings vehicle to help prospective home buyers save for a down payment.

Likely more effective, however, would be for Congress to help stimulate the supply of housing by reevaluating current policies that increase the cost of construction and ultimately decrease the supply of homes.