Insight

May 4, 2026

AI Data Center Power Surge: Shifting Trends Toward Natural Gas

Executive Summary

- Rapid growth in artificial intelligence (AI) data center power demand is driving a resurgence in fossil fuel investment, highlighted by the 2026 approval of massive natural gas projects in Texas and Pennsylvania; these developments pose challenges to carbon-free energy targets as utilities prioritize grid reliability to support 24/7 AI workloads.

- While renewable energy continues to dominate total planned capacity, there has been an increase in natural gas planned capacity from 11.1 percent in 2024 to 18.1 percent in 2026—notably, planned non-renewable additions surged by 71 percent from 2025–2026, while renewable growth flattened to just 2 percent over the same period.

- Despite higher carbon intensity, natural gas maintains a significant competitive edge due to lower grid-connection costs and higher project completion rates; from 2017–2022, natural gas interconnection costs averaged $24/kilowatt (kW), less than one-tenth the cost of solar ($253/kW) and offshore wind ($335/kW)—as renewable projects face greater geographical and infrastructure hurdles.

Introduction

Rapid growth in artificial intelligence (AI) data center power demand is driving a resurgence in fossil fuel investment. This is highlighted by the 2026 approval of massive natural gas projects in Texas and Pennsylvania. These developments pose challenges to carbon-free energy targets as utilities prioritize grid reliability to support continuous AI workloads.

While renewable energy continues to dominate total planned capacity, there has been an increase in natural gas planned capacity from 11.1 percent in 2024 to 18.1 percent in 2026. Notably, planned non-renewable additions surged by 71 percent from 2025–2026, while renewable growth flattened to just 2 percent over the same period.

Despite higher carbon intensity, natural gas maintains a significant competitive edge due to lower grid-connection costs and higher project completion rates. From 2017–2022, natural gas interconnection costs averaged $24/kilowatt(kW), more than 10 times lower than solar ($253/kW) and offshore wind ($335/kW), as renewable projects face greater geographical and infrastructure hurdles.

AI Data Center Electricity Demand

AI data centers are driving electricity demand growth across the country, requiring substantial energy to support AI workloads and advanced cooling infrastructure. The Department of Energy (DOE) estimated that data centers accounted for about 4.4 percent of total U.S. electricity consumption in 2023, and are expected to reach 6.7–12 percent by 2028.

The demand for power is expected to continue rising sharply due to a range of factors, including the increase in data centers over the next decade. Grid-power demand from data centers is expected to nearly triple by 2030. This rapid load growth has direct implications for the power sector, and meeting this demand will require significant additions to generation capacity.

While the DOE has characterized this data center growth as an opportunity to accelerate the clean energy transition, citing in practice, it is increasingly difficult to maintain reliable electricity supply while prioritizing carbon-free targets. For example, a previous American Action Forum (AAF) analysis examined the difficulty of reaching Virginia’s clean energy mandates while maintaining service reliability for customers. Virginia’s largest utility company, Dominion Energy, estimated that reaching a carbon-free electricity portfolio by 2045 would be impossible without invoking the exemption provision in the law to retain some fossil fuel generation sources.

Recent Power Generation Announcements

Recent new power plant announcements suggest that fossil fuels are playing a significant role in meeting this growing demand for power. In early 2026, several large-scale natural gas power projects have been approved. For example, in January, Pacifico Energy’s GW Ranch in West Texas became the largest approved gas power project in the country when the Texas Commission on Environmental Quality granted an air permit of up to 7.7 gigawatts (GW) of generation by natural gas turbines to power a private grid supporting data centers. Similarly, just last month, NextEra also secured approval for two large natural gas plants in Texas and Pennsylvania with a combined 10 GW of power to be connected to their respective regional transmission grids.

At the same time, there are continued announcements of renewable power purchase agreements (PPA) to satisfy data centers’ electricity demand, such as Meta announcing a PPA with MN8 Energy, a renewable energy company, for 80 megawatts (MW) of solar energy and Google partnering with TotalEnergies for 1 GW of solar capacity.

Natural gas power plants, while more carbon-intensive than renewable energy sources, can run continuously to generate electricity. Renewable energy sources, despite their zero-emission features, can only run intermittently. Investments in fossil fuels and renewable energy sources raise questions about how data centers are shaping power generation mixes.

Impact on Power Generation Mix

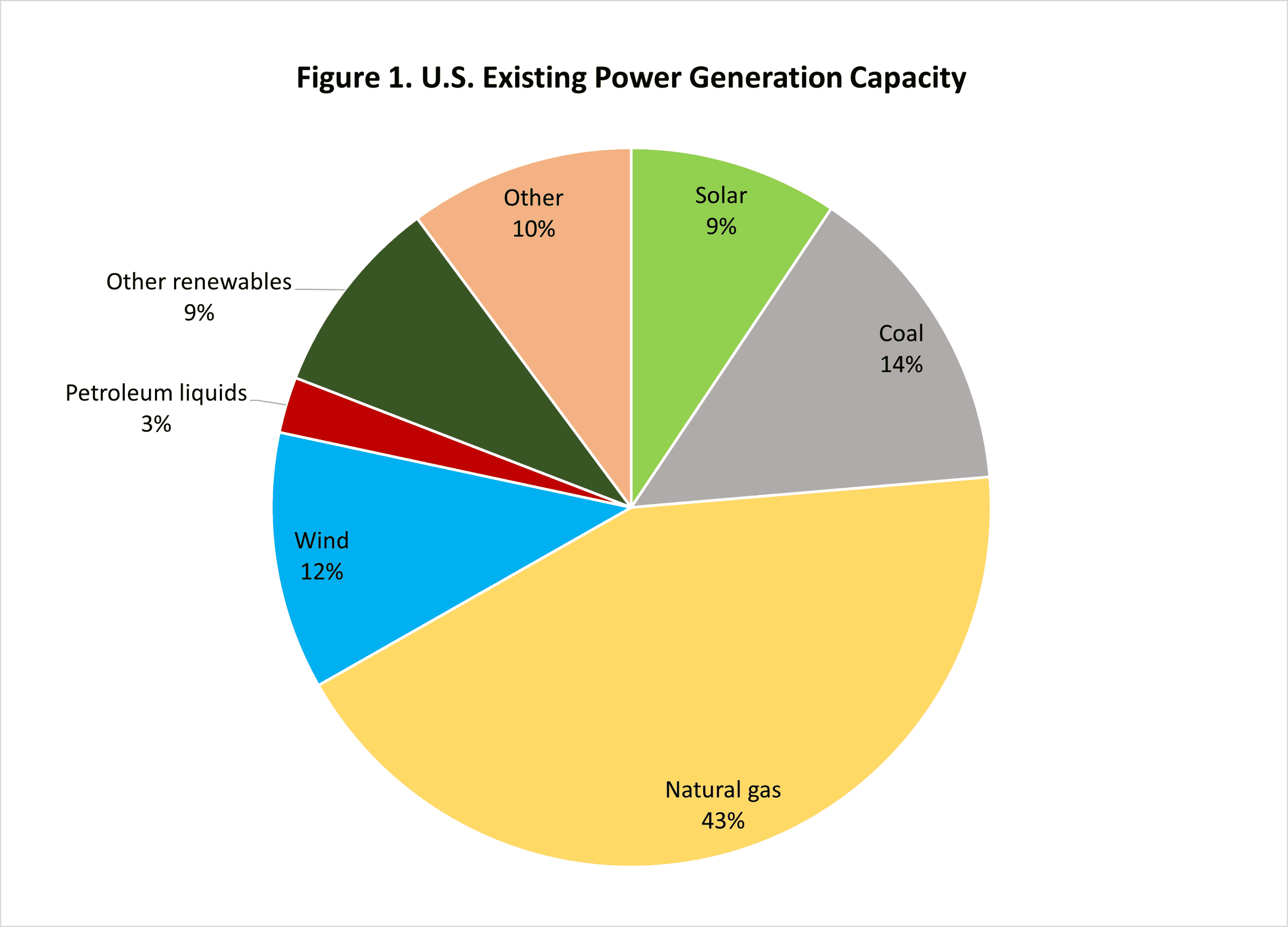

Existing mix of power generation capacity

Currently, the nameplate capacity, or the maximum output of generators in the country, is dominated by natural gas, accounting for 43 percent of total capacity, as depicted in Figure 1. This is followed by coal (14 percent) and wind (12 percent).

Source: Energy Information Administration

Note: This chart depicts total nameplate capacity, which is the theoretical maximum output of generators.

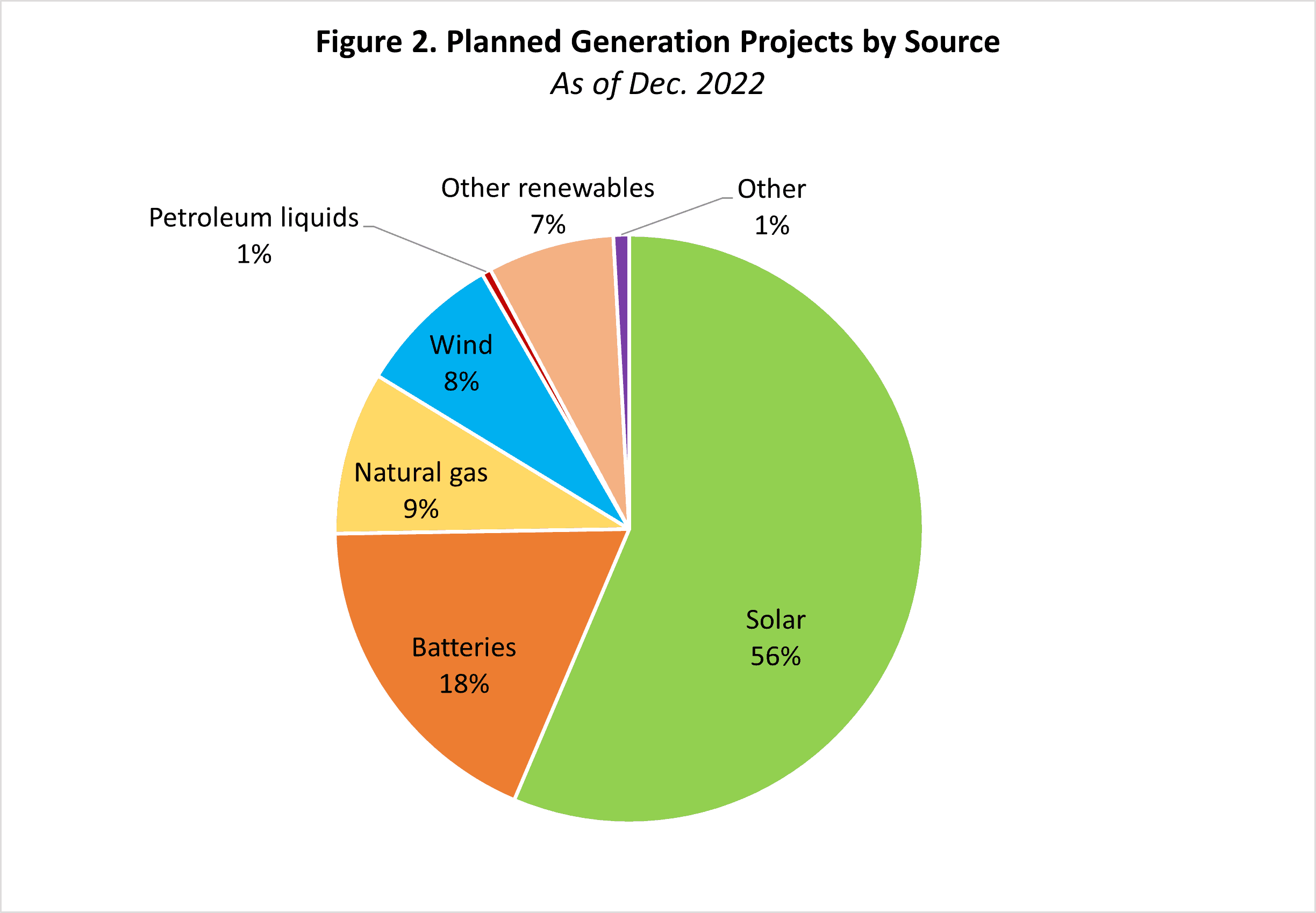

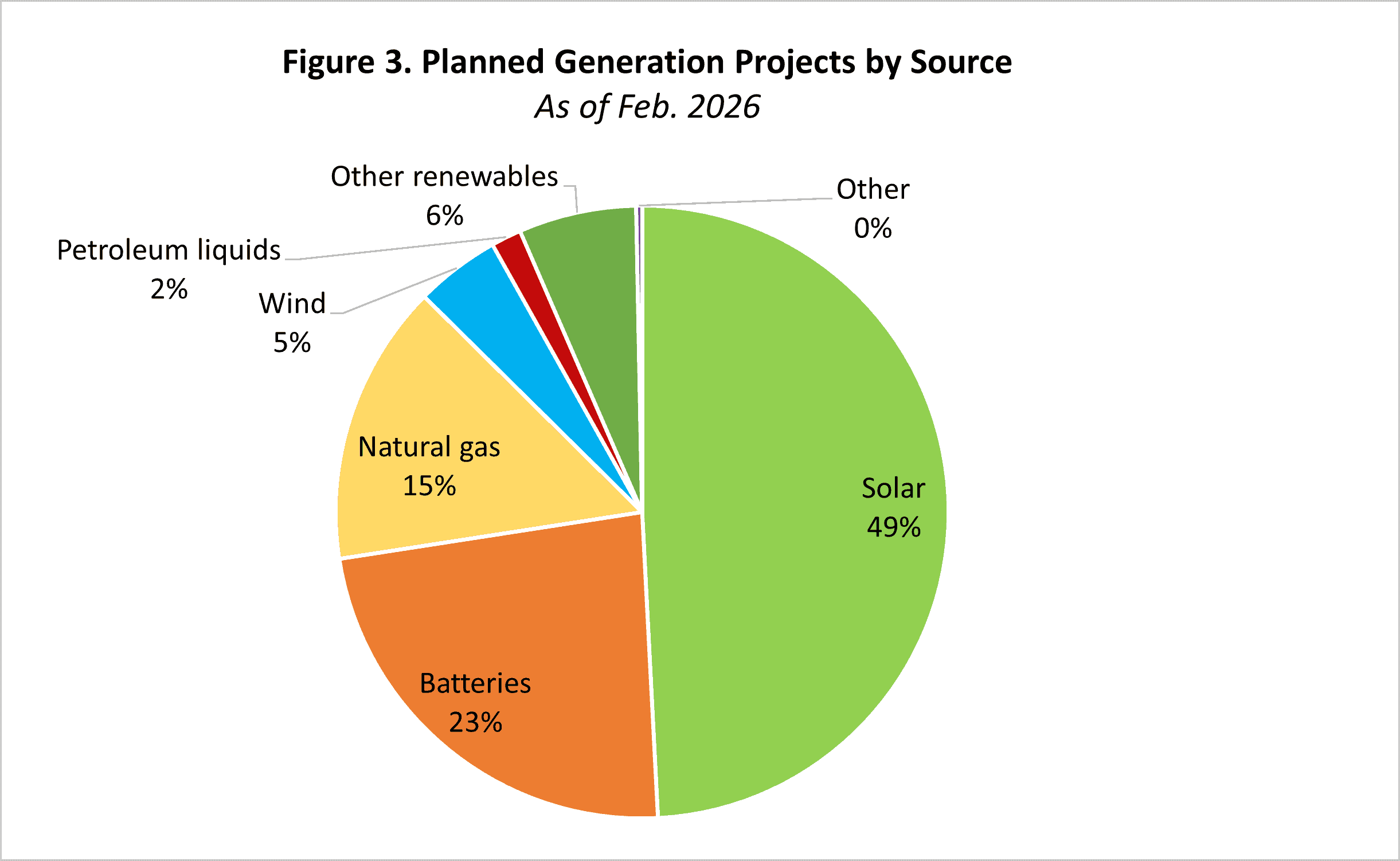

Changes in mix of energy projects

To focus on the effects of the surge in AI data centers, this analysis captures the months leading up to the release of ChatGPT in late 2022 and onward. The Energy Information Administration’s (EIA) Preliminary Monthly Electric Generator Inventory publishes lists of planned power generating units with at least 1 MW of capacity on a monthly basis since 2015.

Figures 2 and 3 depict the numbers of projects of planned utility-scale electric generating capacity additions by energy source at two points in time: December 2022 and February 2026 (the most recent data). Note that the timeframe of the planned projects varies widely, as it includes projects that are expected to come online in February 2026, or as far out as 2039.

From December 2022 to February 2026, the composition of planned generation projects has shifted away from renewable sources and toward natural gas. Within the span of just over three years, the share of planned natural gas projects has increased by 6 percent, while the share of renewable energy projects (solar, wind, and other renewables) declined by 11 percent.

Solar projects continue to represent the largest share of planned capacity additions, indicating that the broader trend towards renewable energy is still underway. This is most likely driven by the Biden-era clean energy tax credits in the Inflation Reduction Act. The most recent planned projects suggest a growing role for fossil fuels in the near-term as the AI boom progresses. This likely reflects the repeal of these clean energy credits in the One Big Beautiful Bill and soaring demand from AI data centers.

Source: Energy Information Administration

Source: Energy Information Administration

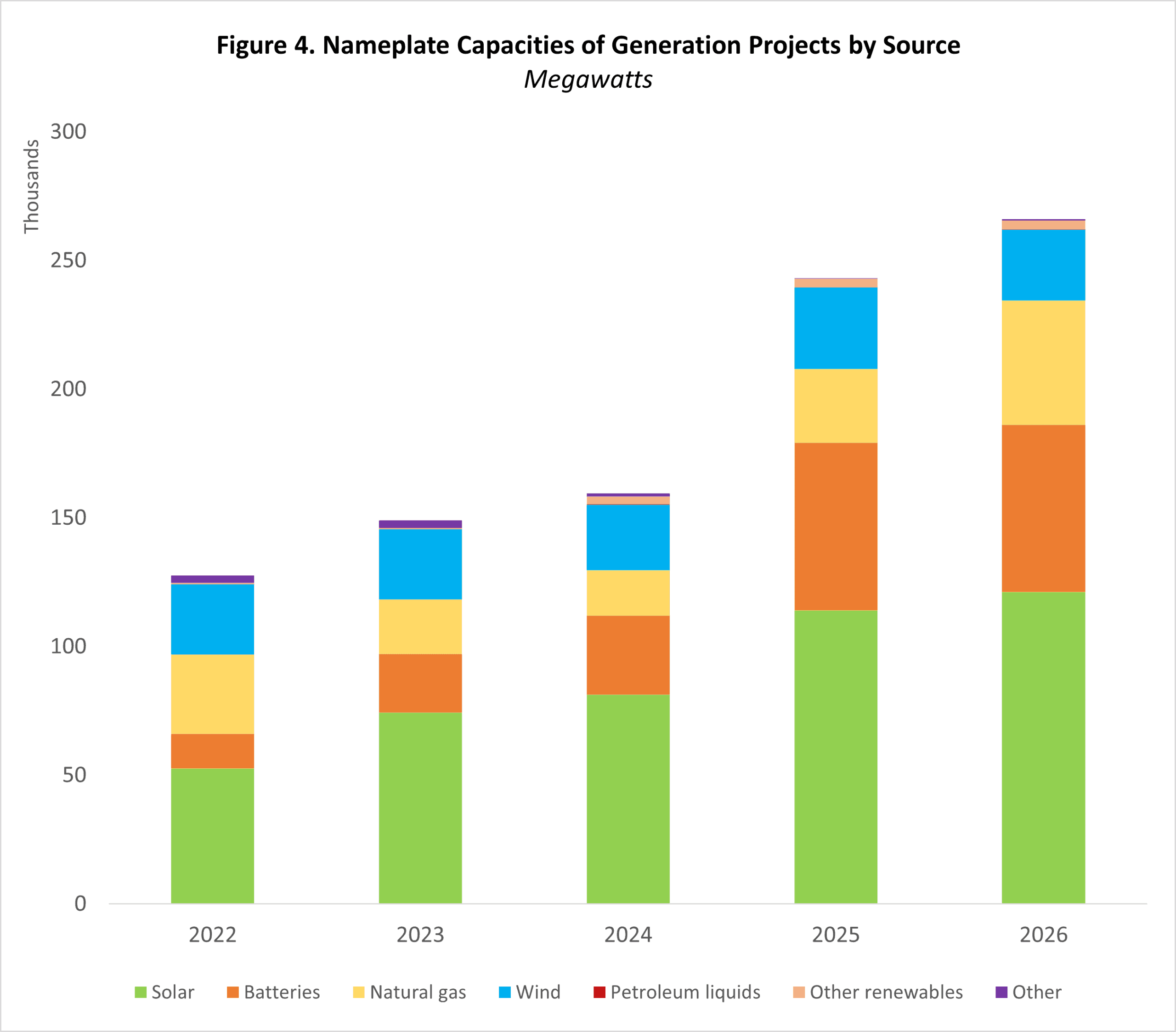

Changes in energy capacity mix

Figure 4 shows the breakdown of nameplate capacities of planned generation projects by energy source as of January of each year since 2022. Overall, between 2022–2026, there was an 89 percent increase in planned renewable project capacity (solar, wind, other renewables) and 46 percent increase in non-renewable capacity (natural gas, petroleum, other).

Notably, as a share of total planned capacity, natural gas fell from 24.1 percent in 2022 to 11.1 percent in 2024, but bounced back to 18.1 percent in 2026. Solar energy accounted for the largest share of planned new generation from 2022–2026, peaking at 51 percent in 2024 and dropping slightly to 45.6 percent in 2026 (as a greater number of non-renewable projects were planned). Wind energy, on the other hand, has been consistently decreasing in share of total capacity from 21.4 percent in 2022 to 10.3 percent in 2026.

Source: Energy Information Administration

Note: The data show the breakdown of nameplate capacities of planned generation projects by energy source as of January of each year.

Comparing the changes in planned capacity by source from year to year reveals additional insights on the shifting priorities. From 2022–2023, there was an overall 27 percent increase in planned additions to renewable project capacity and a 29 percent decrease in planned non-renewable capacity additions, reflecting the broader decarbonization trends depicted in Figure 2.

Meanwhile, from 2025–2026, there was a net 71 percent increase in non-renewable capacity additions, compared to only a 2 percent increase in planned capacity additions from renewable projects, with both figures accounting for projects entering the inventory and exiting upon cancelation or completion.

The stark difference in the planned capacity additions from the period preceding the launch of AI in 2022 to present day suggests a shift in near-term capacity planning. This is consistent with the EIA’s reports projecting that higher electricity demand from data centers would primarily be met through natural gas-fired power plants.

Interconnection Challenges

The planned projects in the EIA’s Preliminary Monthly Electric Generator Inventory are not guaranteed to reach completion, as they only reflect the current expectations of developers. The interconnection step, which is where the power plants must gain approval to connect to transmission networks, creates a bottleneck for new energy projects in the development process.

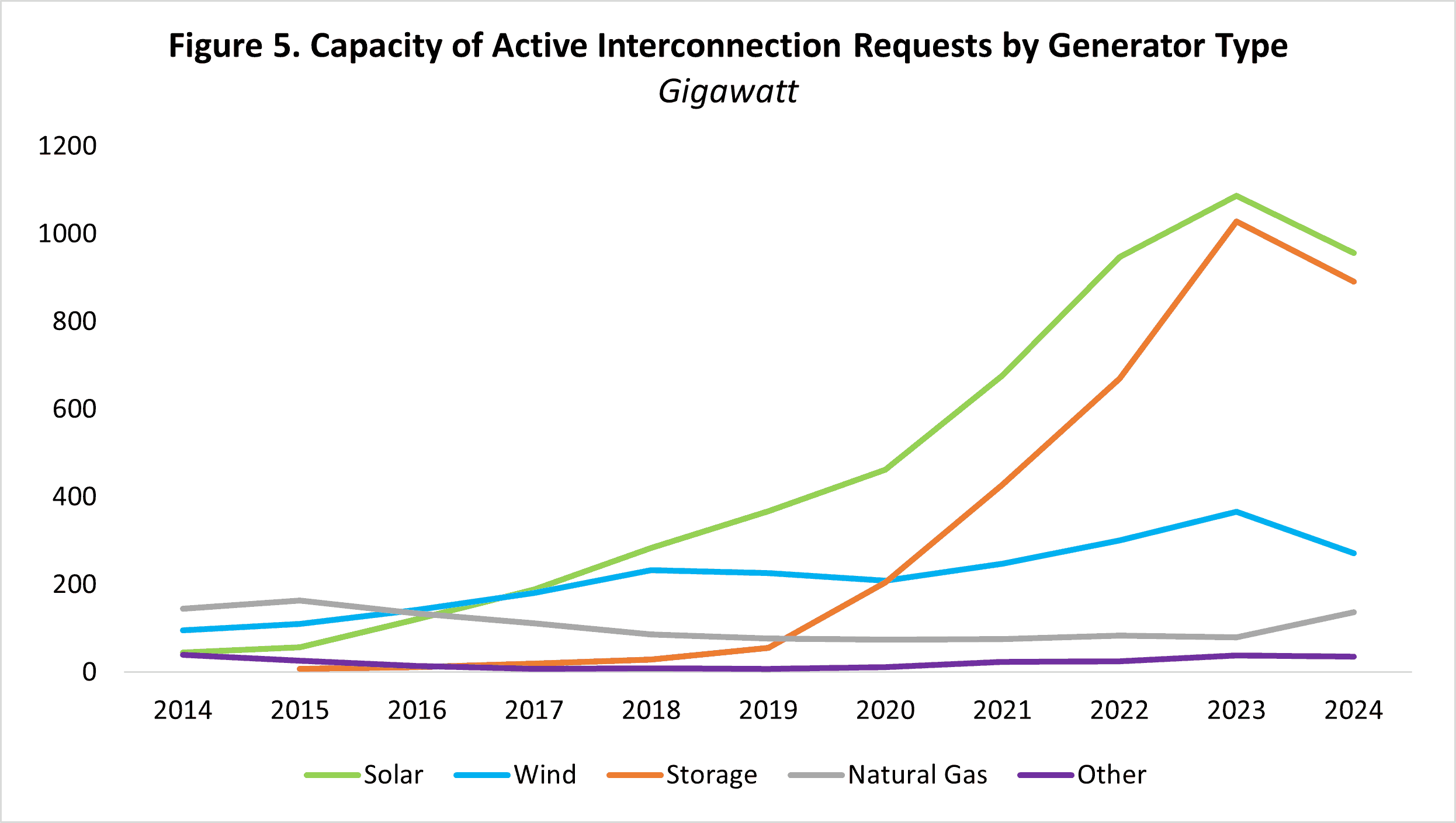

Figure 5 shows the total capacities of projects active in the interconnection queue over time by source. Solar and storage projects dominate requests, while natural gas projects only account for a small share of capacity in the interconnection pipeline.

Source: Lawrence Berkeley National Laboratory

There are several reasons why there are many more solar and storage projects in the interconnection pipeline than natural gas projects. As discussed above, solar and battery projects dominate the planned capacity in terms of both the number of projects and total planned capacity.

Additionally, natural gas projects face fewer barriers to reach operation. Between 2000–2018, solar projects faced a low completion rate of 14 percent, trailing significantly behind the 32 percent success rate of natural gas facilities. In response to mounting interconnection volumes, grid operators have introduced fast-track queues that seem to have prioritized gas-fired projects over other energy sources.

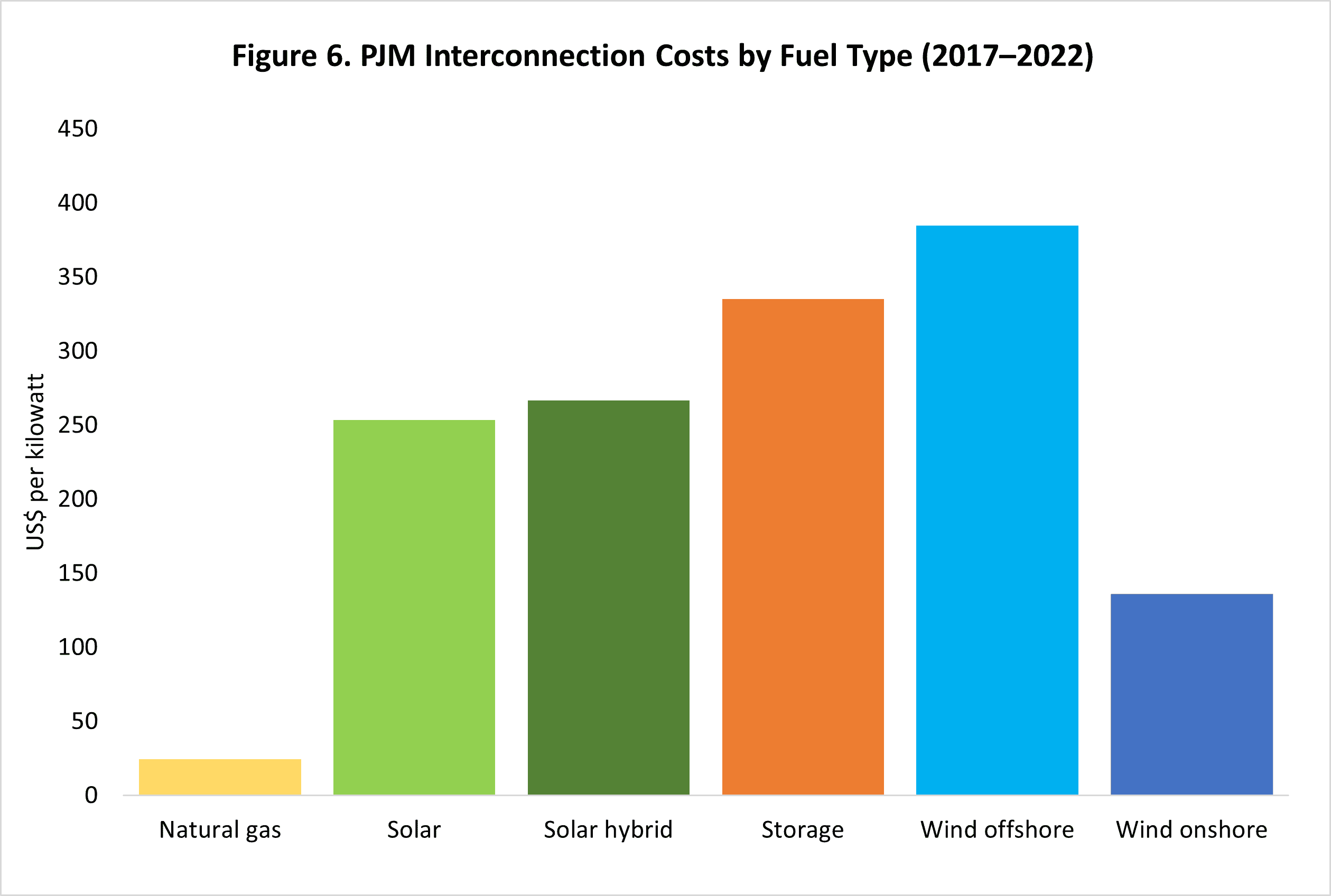

Notably, renewable energy tends to be more expensive than natural gas to connect to the grid. Figure 6 shows interconnection costs—the cost to connect projects to the transmission grid— of all projects between 2017–2022 in the PJM territory (the largest regional transmission operator in the country).

The chart reveals that the total interconnection cost for a natural gas project averaged around $24/kW from 2017–2022, compared to $253/kW for solar and $335/kW for offshore wind. The significant cost difference is driven by geographic or technological limitations. Notably, solar and wind projects are often located in more remote areas. Because these renewable projects are more dispersed and geographically distant from areas with existing infrastructure, they require new substations and long-distance transmission lines to be built to bring the renewable energy to the grid.

Source: Lawrence Berkeley National Laboratory

Often, the high cost of interconnecting to the grid forces projects to withdraw from the queue. A recent study revealed that 80 percent of all requests are ultimately withdrawn while in the interconnection queue. These interconnection obstacles help explain why capacity addition plans seem to be favoring resources such as natural gas over renewable sources.

Looking Forward

As the AI boom continues to drive tremendous power demand, natural gas will likely play an increasingly important role in electricity generation. Unless the economic barriers of connecting renewable energy to the grid are addressed, growing electricity needs of AI data centers will likely be met by a fossil-fuel-heavy energy mix, potentially stalling progress toward long-term decarbonization targets.