Insight

February 5, 2026

CMS’ Third IRA Negotiation List: Selections, Signals, and Potential Savings

Executive Summary

- The Centers for Medicare and Medicaid Services (CMS) recently announced the third round of selected drugs for the Medicare Drug Price Negotiation Program, the implementation of Inflation Reduction Act (IRA)-authorized government price-setting for prescription drugs.

- This round – which will have an initial pay applicability year (IPAY) of 2028 – includes high spend, single source drugs in Part D and, for the first time, in Part B; this round represents 1.8 million beneficiaries and separately includes a renegotiation of a previously selected drug.

- While the IPAY 2028 process is just beginning, it is important to understand the selections that were made and the next steps in the negotiation process – and to remember that no data has yet been collected on the impact of the drug negotiation regime on Medicare expenditures or beneficiary costs and access.

Introduction

The Centers for Medicare and Medicaid Services (CMS) recently announced the 15 drugs selected for the third cycle of the Medicare Drug Price Negotiation Program (MDNP) under the Inflation Reduction Act (IRA), with the eventual negotiated prices – maximum fair prices (MFPs) – set to take effect January 1, 2028. For the first time, the selection pool for initial pay applicability year (IPAY) 2028 includes drugs payable under Part B alongside Part D drugs.

Through successive selection cycles, as the highest spend and highest utilized drugs have been picked, the impacted beneficiary population and the total Medicare spending on the available drugs has slowly shrunk. The selected drugs in this cohort represent approximately 1.8 million Medicare beneficiaries and Part B and Part D expenditures totaling roughly $27 billion. In another new front, CMS also identified the program’s first renegotiation. The IRA set three explicit criteria for the potential renegotiation of a drug, including changes to its monopoly status, changes in the approved indications, or sufficient enough time has passed that the initial Maximum Fair Price (MFP) could be renegotiated for substantial savings.

Although the IPAY 2028 process is just beginning and there are many iterations of input and negotiations to work through, it is important to understand the selections that were made and the next steps in the negotiation process. Even more importantly, there is a cautionary tale that should be remembered throughout the IRA drug negotiation process: no data has been collected as of yet on the impact of the drug negotiation regime on Medicare expenditures or beneficiary costs and access.

Calendar Year 2026 Selected Drugs

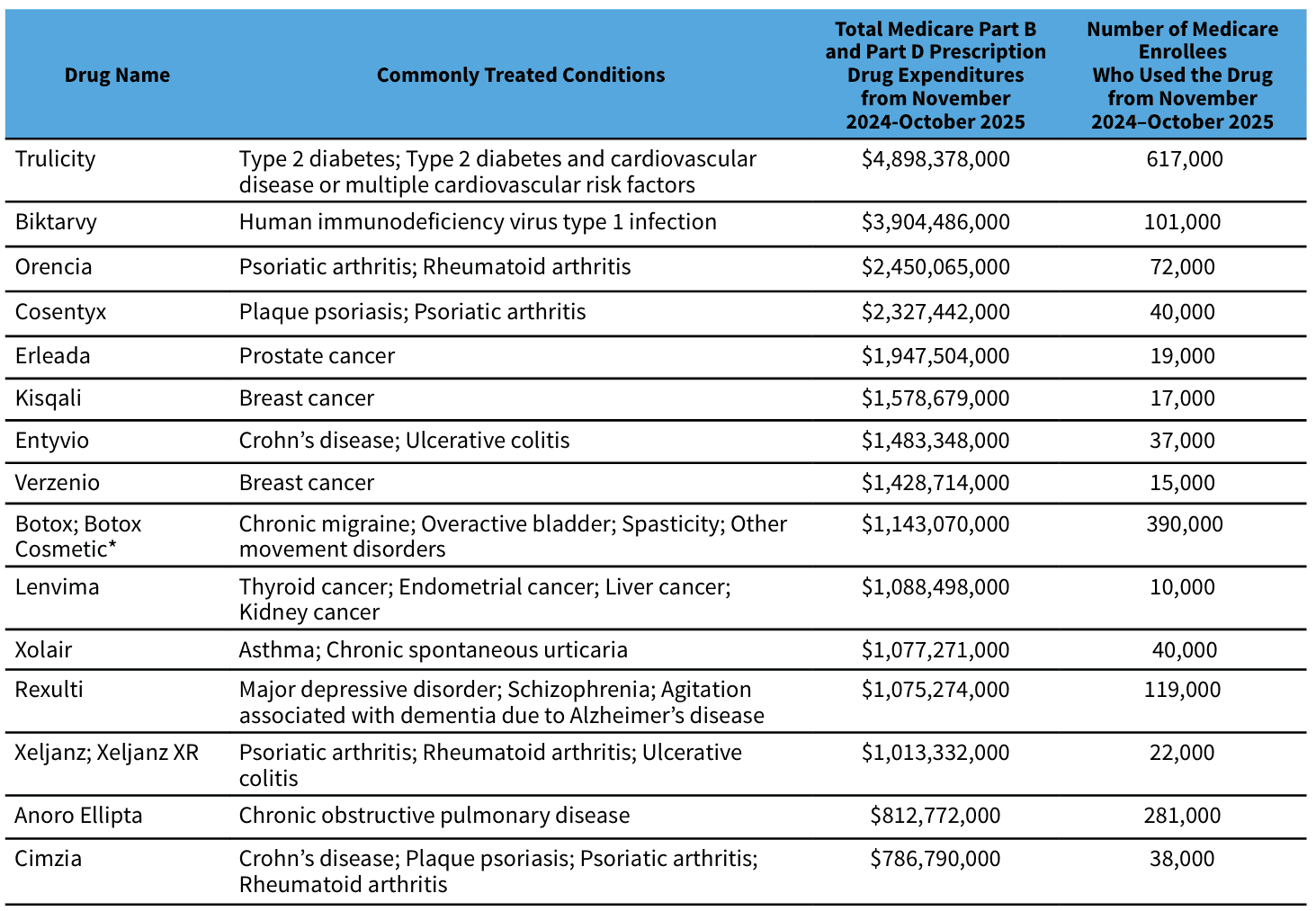

In the third negotiation cycle, the most notable change is that CMS is now including Part B–payable drugs into the selection framework. Below is the list of selected drugs, with aggregated Part B/Part D expenditures and beneficiary utilization numbers.

Source: Centers for Medicare and Medicaid Services

The composition of the selected drugs reflects a shift toward higher-cost specialty therapies, including several drugs used in oncology and immunology, alongside high-spend chronic therapies. CMS reported that about 1.8 million Medicare beneficiaries used the selected products in the measurement window and that total Part B and Part D expenditures for the cohort were roughly $27 billion (about 6 percent of combined Part B/Part D drug spending). The level of spending suggests a list that is not only large in aggregate dollars but also relatively concentrated among a handful of products at the top – an important feature when thinking about where negotiated savings would most likely accrue.

Using Past Negotiation Results to Estimate Potential Savings

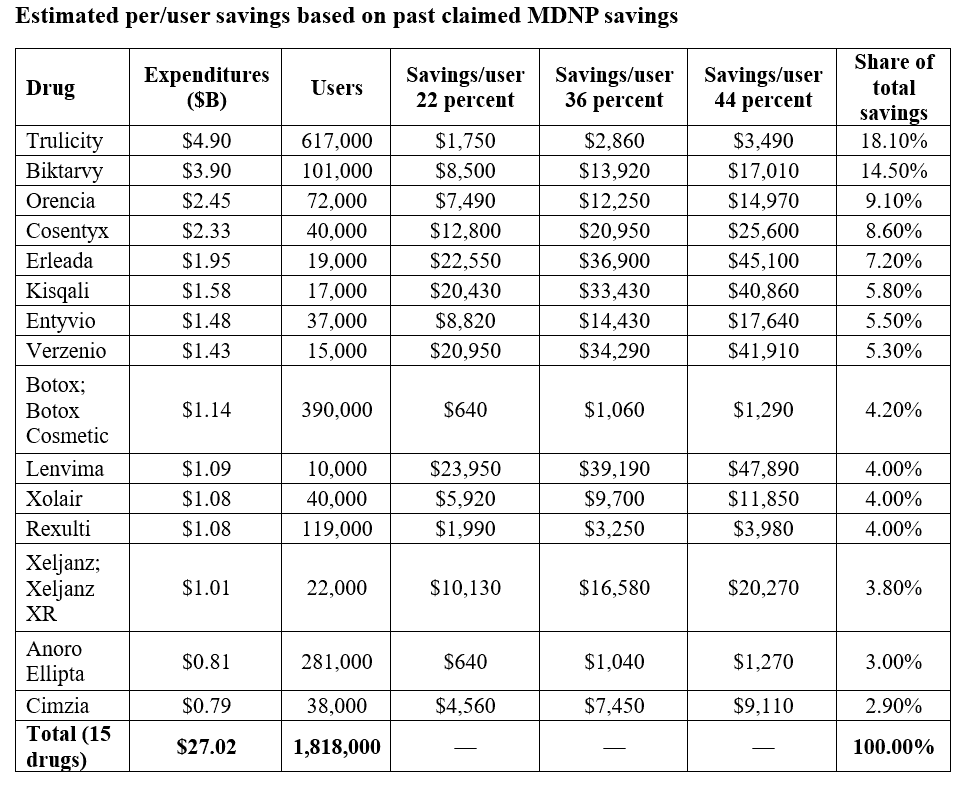

To understand the potential impacts of negotiations on selected drugs, past savings rates were used to as a starting point for a third-cycle savings range:

- First cycle (IPAY 2026; 10 Part D drugs): CMS estimated that if the MFPs had been in effect in 2023, Medicare would have saved $6 billion in net covered prescription drug costs, representing 22 percent lower net spending across those drugs.

- Second cycle (IPAY 2027; 15 Part D drugs): CMS stated that if those MFPs had been in effect in 2024, they would have saved $8.5 billion in net covered drug costs inclusive of Coverage Gap Discount Program spending – about 36 percent lower net spending in aggregate. (CMS has also described this cycle as $12 billion in net savings under a different net savings convention.)

A reasonable, CMS-anchored estimate is therefore to apply a 22–44 percent net savings rate to the third-cycle cohort’s $27 billion baseline expenditures.

Resulting annualized savings range:

- Low (22 percent): $5.9 billion

- Mid (36 percent): $9.7 billion

- High (44 percent): $11.9 billion

Source: CMS and author’s calculations

Source: CMS and author’s calculations

Renegotiation

Under the MDNP’s renegotiation framework (which begins for IPAY 2028), CMS must look back to drugs that were already negotiated for 2026 or 2027 to determine whether any of them should be renegotiated in line with the criteria listed in the IRA. In IPAY 2028, the only drug that qualifies for renegotiation is Tradjenta.

CMS starts with the set of previously selected drugs for which the agency has not determined that a generic or biosimilar is both approved or licensed and marketed, focusing renegotiation attention on products that remain functionally single source in the market. Next, CMS identifies which of those drugs are “renegotiation-eligible” based on whether: (a) the drug’s monopoly status has changed to long monopoly since the original negotiation, (b) the drug has received a new indication, or (c) there has been a material change in one of the statutory negotiation factors used in the original negotiation.

If these criteria are met, CMS indicates that all drugs eligible due to a change in monopoly status will be selected for renegotiation. Drugs that are eligible because of a new indication or material change are selected when CMS believes renegotiation is likely to produce a significant change in the MFP. Such a change is defined in guidance as a renegotiated MFP that is likely to be at least 15 percent different from the current MFP and likely to impact the Medicare program – evaluated through a holistic review of the available information and circumstances.

Why the Third Cycle Could Land Above – or Below – Historical Levels

A few policy mechanics will determine where actual results fall inside (or outside) the above estimated savings. The inclusion of Part B changes the topline savings that CMS may be able to claim in this round. Part B drugs are reimbursed off average sale price-based methodologies and interact with provider “buy-and-bill” incentives. Adding Part B expands the addressable spend, but it also introduces new behavioral channels (site-of-care shifts, alternative selection, utilization management) that can dampen or amplify savings relative to Part D-only rounds.

The net vs. gross price also matters more for specialty drugs. The first cycle’s 22 percent-savings rate is explicitly measured against net spending (after rebates/fees). Specialty biologics can have very different rebate profiles than high-volume retail drugs, so you should expect meaningful dispersion around any single “average” savings rate.

Forthcoming Timelines for the IPAY 2028 Cycle

At this juncture, the basic timeline has become routine for interested stakeholders. The next milestones are set in statute:

- February 28, 2026: Deadline for participating drug companies for the third cycle of negotiations to sign agreements to participate in the negotiation program.

- March 1, 2026: Deadline for participating drug companies to submit manufacturer-specific data to CMS for consideration in the negotiation of an MFP.

- April 2026: CMS will host patient-focused and clinical-focused public engagement sessions.

- June 1, 2026: Deadline for CMS to send an initial offer of an MFP for a selected drug with a concise justification to each drug company participating in the Negotiation Program.

One key difference, however, is having reached IPAY2026, where concrete data will begin to show both CMS and industry the impact of MFP on sales, and may inform the level of savings that each side may be comfortable with accepting.

A Continued Cautionary Tale

Although the drug selection process for the MDNP is a predictable policy baseline at this point, it is worth pausing to consider a basic reality in the program’s implementation. As mentioned above, the health care sector is only at the very beginning of observing what the first negotiated prices do in practice. Basic utilization and spending metrics rely on data that are not instantaneous – claims and encounter-level analyses typically lag – and early-month snapshots are vulnerable to noise, seasonality, and one-time operational adjustments that do not represent steady-state effects.

The initial tranche – 10 Part D drugs with MFPs published in August 2024 – only became effective at the pharmacy counter on January 1, 2026, meaning there has been, at most, a single month of post-effectuation experience as of early February 2026. In that context, most of what is “known” today is still prospective: CMS has provided negotiated prices and counterfactual estimates of what those prices would have done if applied earlier, rather than documented, claims-based results from 2026.

Those numbers are informative for magnitude, but they are not the same as observing realized savings after implementation, because realized savings require measurement of what flows through the Part D payment system. It also requires understanding how Part D plans operationalize the new pricing environment – through formulary placement, tiering, prior authorization, preferred pharmacy networks, and bidding assumptions – and how pharmacies, pharmacy benefit managers, and manufacturers adjust contracting behavior in response.

Utilization impacts are similarly not simple to measure: lower prices can improve affordability and persistence for some patients, but plans may also re-optimize benefit design and steering in ways that shift volume within a therapeutic class, and prescribers may respond to changing relative prices by switching some patients to alternatives. Each of these channels can move total spending even when unit prices fall. Quality outcomes are even further behind the calendar: If a policy goal is better adherence and fewer downstream complications, that requires months (often years) of follow-up and careful attribution, especially because drug utilization and outcomes are influenced by multiple concurrent factors.

Conclusion

CMS’s latest announcement on the MDNP is notable not only for the products themselves – several of which are among Medicare’s highest-spend therapies in oncology, immunology, HIV, and cardiometabolic disease – but also because this is the first cycle in which both Part D and Part B drugs are included. Applying historical percentages to the third-cycle cohort’s reported spending base yields an illustrative range of several billion dollars per year in potential savings, while continuing to be threatened by the central uncertainties of beneficiary behavior and drug demand that will determine where actual results land.