Insight

April 9, 2018

Highlights of the CBO’s Budget and Economic Outlook

Today, the Congressional Budget Office (CBO) released its Budget and Economic Outlook: 2018-2028, which provides Congress with a 10-year budgetary yardstick to evaluate the costs of potential legislation. Underpinning the budgetary projections is CBO’s economic forecast for the next decade, which incorporates the assumed economic effects of legislation enacted since CBO’s last update, specifically the Tax Cuts and Jobs Act (TCJA) and the Consolidated Appropriations Act of 2018.

By the Numbers

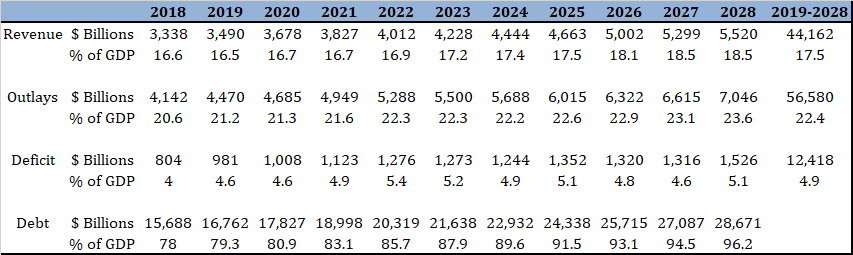

Taxes: By the end of the 10-year budget window, tax revenues will amount to 18.5 percent of GDP. Tax revenues will average 17.5 percent of GDP over the next 10 years, which is down compared to CBO’s June update, but is above the 17.4 percent historical average. This decline is no surprise given the enactment of the Tax Cuts and Jobs Act (TCJA) in the intervening months. This change reflects the net effect of substantial estimated reductions in tax collection (nearly $1.7 trillion) due to policy changes, and a significant increase in tax collections (about $1 trillion) due to higher projected economic growth. Tax collection averaged 18 percent of GDP over the 2018-2027 period in last year’s estimate. It is important to note that a significant contributor to the substantial uptick in revenue collection in the last three years of the budget window stems from the sunsetting of significant elements of the TCJA in 2025.

Spending: By the end of the budget window, CBO estimates that overall spending will amount to 23.6 percent of GDP, amounting to $56.6 trillion over the period 2019-2028. Entitlement, or mandatory, spending will continue to grow as a share of the federal budget, comprising 64 percent of federal expenditures in 2028, up from 28 percent in 1968.

Deficits: Projected budgets deficits will grow substantially over the budget window, reaching over $1 trillion in 2020, two years sooner than projected by CBO last June. The deficit will average 4.9 percent of GDP over the 2019-2028 period, exceeding average economic growth over the same period by nearly a percentage point. Accordingly, debt accumulation will continue to grow as a share of the U.S. economy over the next 10 years.

Interest Payments: Interest payments on the debt will reach $915 billion in 2028. This figure reflects a more than tripling of debt service costs of $263 billion in FY2017. By 2025, interest payments on the debt will be the federal government’s third largest spending program – exceeding defense spending, Medicaid, and the Disability Insurance component of Social Security.

Debt Held by the Public: Borrowing from the public is projected to increase as a share of the economy under current law, reaching 96.2 percent of GDP in 2028. Only in 1945 and 1946 has the debt held by the public been higher.

Economic Projections

CBO’s economic outlook is in many ways unchanged from its June 2017 update because the major inputs to long-term growth – the labor force and productivity – are to a large degree fundamentally unchanged in CBO’s outlook. Instead, CBO projects faster growth in the near term, stemming from recently enacted legislation, with slower growth in the medium term, before settling to roughly the same long-term growth projection of 1.8 percent in the last 10 years of the current budget window. For comparison, the table above includes the economic projections assumed in the President’s Budget, released by the Office of Management and Budget (OMB) in February.