Insight

June 25, 2019

Highlights from the Long-Term Budget Outlook 2019

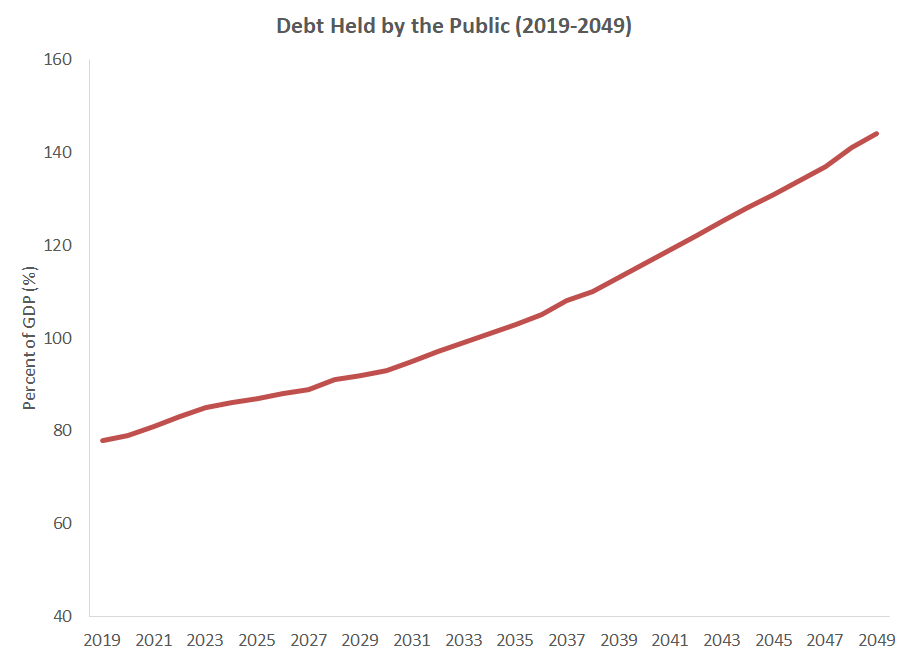

The Congressional Budget Office (CBO) released its updated Long-Term Budget Outlook and projected that the U.S. debt will nearly double as a share of the economy by 2049, rising from the current level of 78 percent to 144 percent of gross domestic product (GDP). This latest projection recapitulates the obvious consequence of long-observed demographic and economic trends paired with apathy from policymakers, as this year’s Long-Term Outlook is largely similar to last year’s projection. Fundamentally, the basic problem remains – federal commitments to health and retirement programs and the interest owed on a growing portfolio of debt outstrip current and historical levels of taxation.

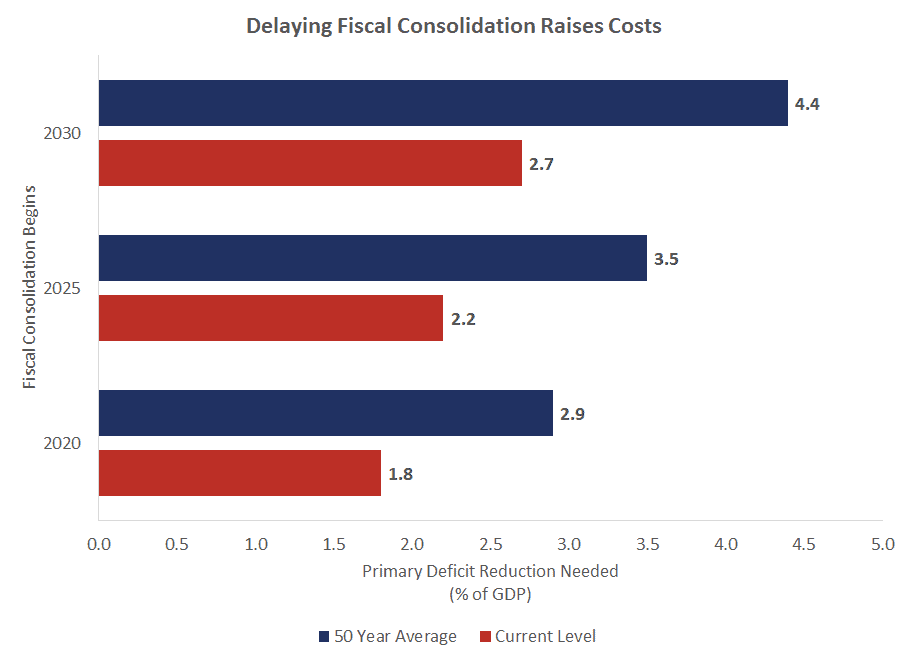

This year’s debt projection is incrementally smaller than last year’s, driven in part by reduced projected discretionary spending for disaster funding. This reduction is essentially a mechanical difference, and given that disasters are necessarily unpredictable, it should hardly be considered an improvement in the deficit outlook. The key difference between this year’s projection and last year’s is the passage of time. Another year has passed, and policymakers have not signaled any appetite for addressing this challenge. But inaction is not costless – as figure 3 demonstrates, the longer policymakers wait to slow and reverse the nation’s debt accumulation, the larger and more painful the tax increases or spending reductions (or combination of both) needed to accomplish this consolidation become. Already, the amount of fiscal consolidation needed simply to stabilize the nation’s historically high debt level at 78 percent of GDP is staggering. Simply keeping the debt at 78 percent of GDP by 2049 would require lawmakers to enact 1.8 percent of GDP in annual deficit reduction, which would be $380 billion in 2019. In contrast, Congress recently failed to pass a spending reduction of $1.1 billion.[1]

Figure 1

According to CBO’s Long-Term Outlook, projected debt in the hands of the public will reach 144 percent of GDP by 2049. This figure is somewhat down from last year’s projection, but that was in part animated by how CBO projects disaster spending, as noted above. Over the medium term, projected deficits are higher than were projected prior to the enactment of recent fiscal policies (e.g. the Tax Cuts and Jobs Act, the Bipartisan Budget Act of 2018) but over the longer term, the debt outlook remains driven by demography (which hasn’t changed since the last Long Term Budget Outlook), the nation’s major entitlement programs (which are also unchanged), and growing interest on the nation’s expanding debt portfolio.

Figure 2

Today’s Long-Term Outlook reaffirms a trend in the nation’s finances: Debt service costs are crowding out other federal expenditures, and in 2045 these costs will exceed all other discretionary programs – defense, education, infrastructure – combined.

Figure 3

CBO has also been calculating what is essentially the cost of delaying needed fiscal consolidation. To hold debt held by the public as a share of GDP to current levels (78 percent of GDP) in 2049 would require an annual reduction (relative to CBO projections) in the primary deficit (a revenue increase, spending decrease, or both excluding net interest) of 1.8 percent if begun next year, which amounts to $380 billion in 2019. Achieving the same level of debt in 2049 would require a much larger fiscal consolidation if delayed until 2025, or 2030. The same story holds true if the United States were to return its 2049 debt level to the 50-year historic norm of 42 percent of GDP. It would require annual savings of 3.5 percent if begun in 2025, but 4.4 percent if begun in 2030. In both instances, achieving the necessary deficit reduction to achieve fairly modest debt targets in 2049 would be difficult if begun now, but would be about 50 percent more painful if delayed for 10 years.

The current federal budget trajectory promises higher debt and, consequently, reduced public and private investment. This spending growth reflects growing federal transfer programs and borrowing needs financed by a lower standard of living for future generations. Absent reform, these trends are becoming increasingly intractable and will require more significant fiscal consolidations to address.

[1] https://www.americanactionforum.org/insight/the-house-dabbled-in-governing-the-senate-took-a-pass/