Insight

June 14, 2021

Household Implications of the Biden Administration’s Clean Energy Agenda

Introduction

The Biden Administration has declared climate policy to be its top priority. On Earth Day, the Biden Administration notified the United Nations about how it intends to reduce greenhouse gas emissions in the United States, which was necessary following the United States’ re-joining of the Paris Agreement on climate change. This so-called Nationally Determined Contribution (NDC) set an economy-wide target of reducing greenhouse gas emissions by 50-52 percent from 2005 levels by 2030.

Achieving this goal will require a massive change in U.S. energy sources, moving away from carbon-intensive sources such as coal, oil, and natural gas and toward greater use of wind, solar, geothermal, hydroelectric, and (potentially) nuclear power. Such an enormous change will not happen easily or cheaply. While the administration’s policy presumes that there are benefits to reduced greenhouse gas emissions, it is important that policymakers and the public understand such benefits will be accompanied by significant costs.

This short presentation outlines the macroeconomic, sectoral, and distributional costs of transitioning to a so-called green energy portfolio. I begin by walking through the basic economic forces in play as a result of such a policy, briefly review the lessons of the 1970s and early 1980s disruptions in oil markets, and then turn to a forward look at the electricity sector.

A Stylized Adjustment Scenario

Broadly speaking, one can think of the production and consumption in the economy as built upon energy, with carbon-based and non-carbon-based sectors. The basic idea is to restrict the use of carbon-based fuels, which one can think of as a decline is the supply of such fuels.

The immediate impact is to make the now-scarce supply of carbon fuels more valuable, with prices rising as users scramble to be successful in acquiring the limited supply. In the extreme, firms cannot substitute between fuels so overall energy supply is restricted. At the same time, production costs have risen. This combination will result in less production and higher prices. In the aggregate, a sudden, unexpected restriction in carbon fuel supplies is a supply shock that generates inflation and unemployment. Households will suffer a similar set of shocks as they are forced to spend more on energy, devote a higher fraction of their spendable income on energy, and cut back on saving to finance the increased energy costs.

The magnitude and impacts will be smaller the further out these shifts are anticipated and as more advance notice is provided.

Over time, firms and households will adapt to substituting non-carbon fuels for carbon fuels. Since non-carbon fuels are relatively scarce, the new demand will also drive up their price; energy as a whole is less available and more expensive.

These short-run impacts set off dynamics of adjustment. With carbon fuels being steadily restricted, the return to investment is minimal or zero; capital flees the carbon sector, new investment vanishes, and the value of existing supplies plummets. The mirror image of these impacts occurs on the non-carbon sector. The existing supplies generate higher prices; they will be much more valued by investors. There is ample reward to new capacity, and capital will flow into non-carbon fuels.

Notice that the asset markets will have winners (holders of non-carbon fuels) and losers (holders of carbon fuels). Over time, employment will contract in the carbon fuels sector and expand in the non-carbon fuels sector, generating labor market winners and losers as well. Since the well-being of regional economies, municipal governments, and non-profits will depend on those sectors, there will be an uneven distribution of boom and bust across the country.

Ultimately, the economy will return to full employment, with a much larger non-carbon sector, larger non-carbon capital stocks, and non-carbon employment. The costs of adjustment, however, can be significant. They will involve capital investment, relocation costs, employment training, and other costs of a sustained period. The more rapidly the green portfolio is implemented, the larger will be the disruptive costs.

Looking Back: Lessons from the 1970s

The decade of the 1970s and early 1980 offer some insights into the dynamics outlined above. In 1973, the 12 countries that made up the Organization of Petroleum Exporting Countries (OPEC) stopped selling oil to the United States. Later in the decade, oil production fell sharply in 1979 following the Iranian Revolution and again in 1980 because of the Iran-Iraq war.

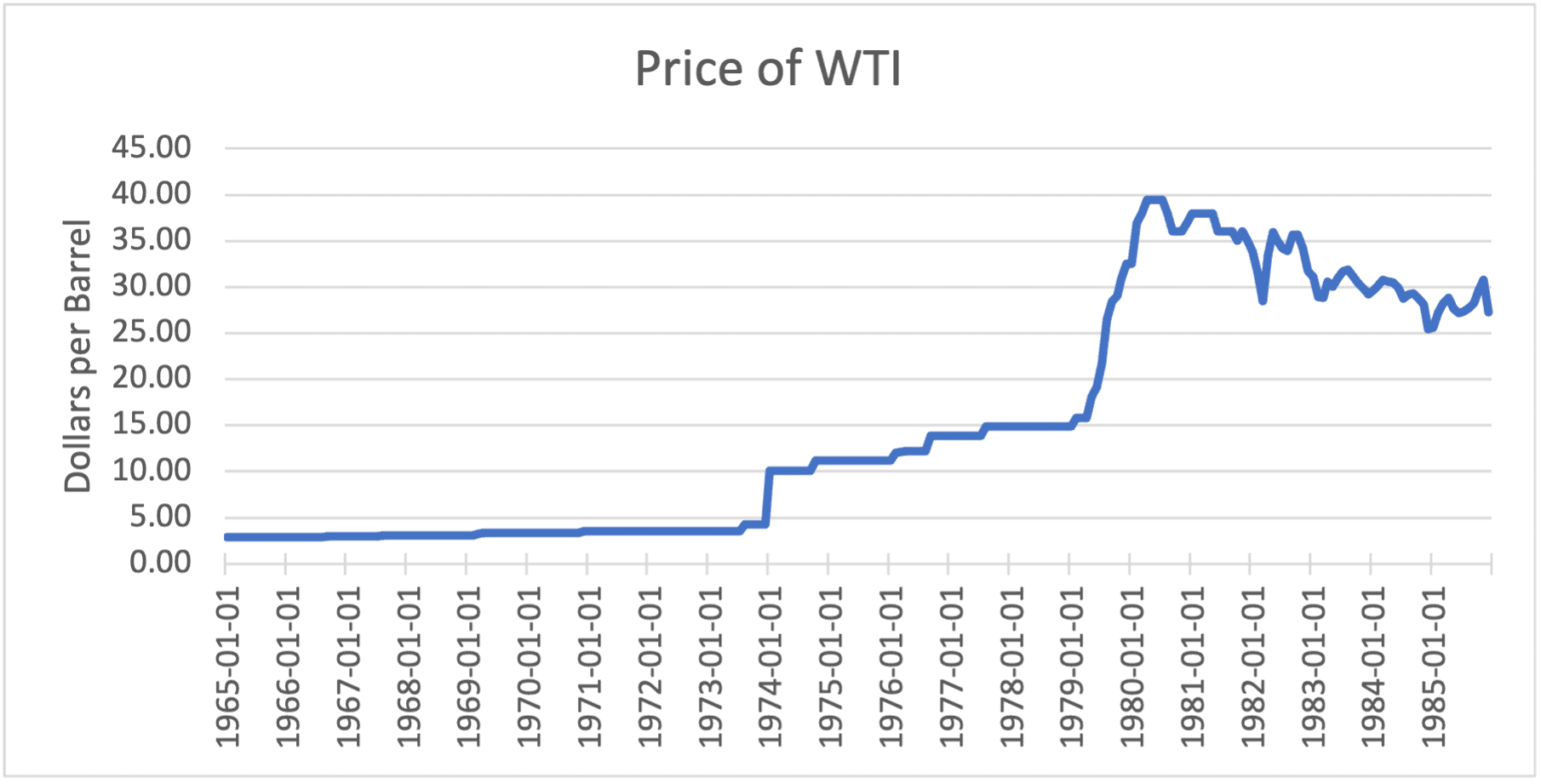

This is precisely the kind of supply restriction the United States would face under the Biden Administration’s policies. These disruptions were also unanticipated and substantial, and so display the extremes of the forces outlined above. To begin, the chart below shows the price of West Texas Intermediate (WTI), monthly from 1965 to 1985. As one can see, the period up to 1973 has stable prices under $5 a barrel. With the embargo, prices more than doubled, never returned to their former levels, and drifted upward to roughly $15 by 1979. With the arrival of the second disruption, oil prices spiked to $40, and remained elevated for years thereafter.

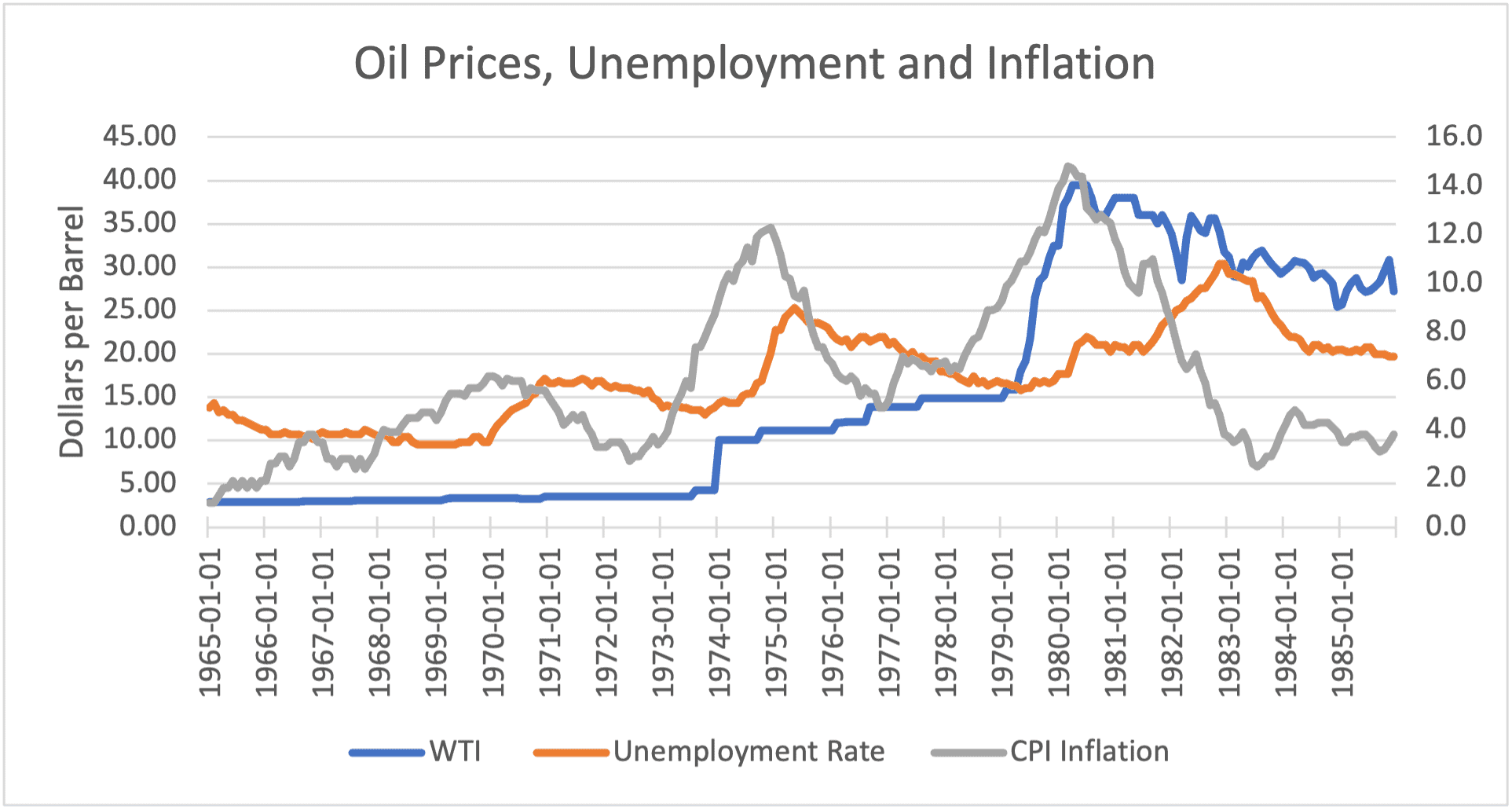

These oil price spikes had a substantial macroeconomic impact. As displayed in the next chart, the sharp movements in oil prices in the early 1970s and 1980s were the prelude to sharp increases in unemployment and consumer price inflation.

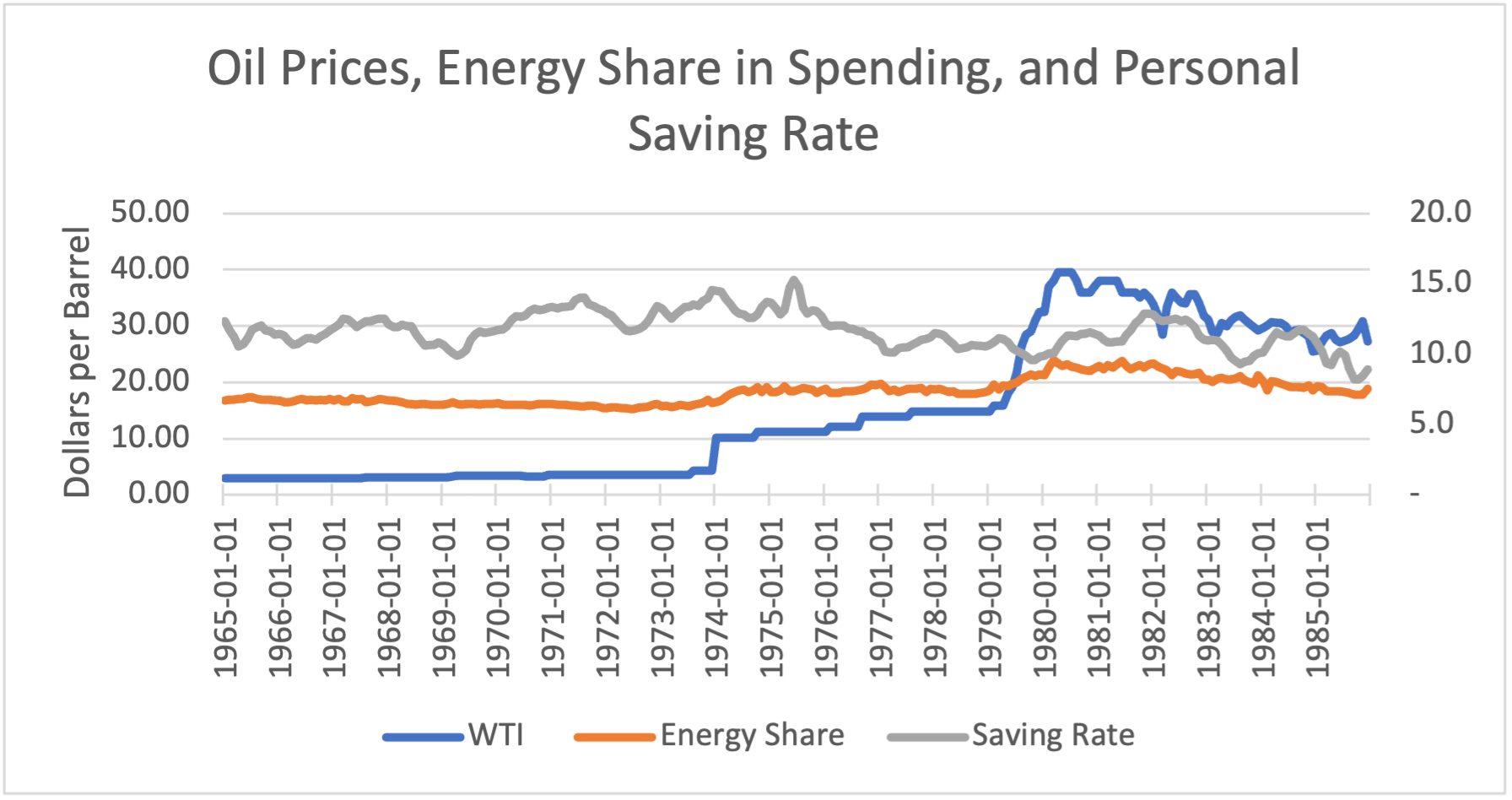

At the household level, the impact was to increase the share of overall spending that was devoted to energy. In addition, the increase in energy costs was in part absorbed by a decline in personal saving.

In short, the abrupt rise in oil prices is a cautionary tale for moving too quickly to curtail carbon sources of energy without the ability of firms and households to easily substitute non-carbon sources and without adequate capacity in the non-carbon sector.

Looking Forward: A Case Study of Electricity Generation

As noted at the outset, the Biden Administration’s NDC submission to the United Nations climate agreement calls for a sharp reduction in carbon emissions. In particular, it calls for all carbon emissions to be removed from electricity generation by 2035. The Democratic leadership of the House Energy and Commerce Committee has introduced the CLEAN Future Act, which includes the same goal and thus serves as a model for the administration’s potential intentions moving forward. My colleague Ewelina Czapla developed two scenarios – one where all fossil fuel generation is eliminated and another where carbon capture technology is applied to natural gas combined-cycle facilities – for meeting this goal.

The analysis finds that meeting the administration’s NDC goal requires approximately $2 trillion of investment in capital and operations and maintenance costs, an unprecedented amount that would result in an additional $90 per month cost for electricity consumers. (Note that in 2019, the average monthly bill in the United States was between $75 and $168 depending on the state.) This sum is probably an understatement of the costs, as it does not fully incorporate the costs associated with creating a truly national transmission grid responsive to non-dispatchable resources.

This is the nature of the adjustment costs noted above. It would be necessary to increase investment in generation by 300 percent in the coming 14 years and potentially increase utility costs by $1,075 per year by 2035.

Thank you and I look forward to your questions.