Insight

March 30, 2020

Housing Provisions in the Coronavirus Aid, Relief, and Economic Security (CARES) Act

Executive Summary

- The Coronavirus Aid, Relief, and Economic Security (CARES) Act is a $2 trillion stimulus package with significant implications across housing and nearly all other aspects of the economy.

- Those with mortgages backed by federal loans can request six months of mortgage forbearance; tenants of homes that receive this forbearance can neither be evicted nor charged fees or penalties for the nonpayment of rent.

- The CARES Act appropriates to the Department of Housing and Urban Development (HUD) $5 billion in additional funding for Community Development Block Grants (CDBG) as well as additional funds for housing programs designed to support vulnerable communities.

Context

In the face of the economic and social disruption caused by the coronavirus, Congress has passed three pieces of legislation aimed at combatting the virus and its impact. It initially passed two significant response packages to address health-sector needs and support American families. On March 26, the “Phase 3” stimulus package, the Coronavirus Aid, Relief, and Economic Security (CARES) Act, was signed into law. With an estimated $2 trillion price tag, the third package is the largest and perhaps most significant stimulus package in American history.

This piece summarizes the implications of the CARES Act specifically for housing.

Division A – Keeping Workers Paid And Employed, Health Care System Enhancements, And Economic Stabilization

Title IV – Economic Stabilization and Assistance to Severely Distressed Sectors of the United States Economy

The primary focus of Title IV is that it authorizes the Treasury to make $500 billion in loans directly to businesses impacted by the coronavirus (for analysis of the implications of the CARES Act for financial services, see here). Also included in the Title, however, are a number of seemingly disparate sections with a much wider focus, ranging from reforming the governance of Federal Reserve meetings to making it easier for banks to restructure troubled debt. This Title has three sections with implications for the housing market.

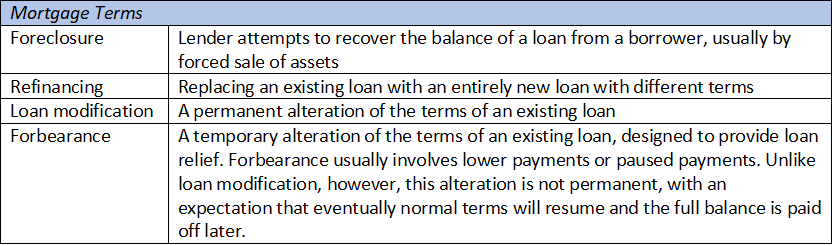

Section 4022. Foreclosure Moratorium And Consumer Right To Request Forbearance

Single-family homes that are backed by a federal mortgage loan may request forbearance of up to a year.

For the purposes of this section, “single-family” means homes designed for one to four families, and a “federally backed mortgage loan” is a loan insured by a federal agency, most obviously the Federal Housing Administration (FHA) or the Department of Veterans Affairs. Any borrower experiencing direct or indirect financial hardship relating to the coronavirus is able to request 180 days forbearance, regardless of delinquency status. This period can be extended another 180 days at the request of the borrower. During this period of forbearance, no fees or interest will be applied to the borrower.

In addition, servicers of federally backed mortgage loans cannot initiate foreclosure proceedings or foreclosure-related evictions for at least 60 days beginning March 18, 2020. This restriction does not apply to vacant or abandoned properties.

Section 4023. Forbearance Of Residential Mortgage Loan Payments For Multifamily Properties With Federally Backed Loans

Under this section, the forbearance options available to single-family borrowers are extended to borrowers in multifamily properties, for example apartment buildings. This forbearance, however, has additional requirements; borrowers must be current on their payments and not evict a tenant or charge late fees or other penalties to tenants during the period of forgiveness. Multifamily forbearance will also cease on either the end of the national emergency or December 31, 2020, whichever comes sooner.

Section 4024. Temporary Moratorium On Eviction Filings

For 120 days from the enactment of the Act (March 27, 2020), lessors of all properties backed by federal mortgage loans can neither evict tenants nor charge fees or penalties for the nonpayment of rent.

Division B – Emergency Appropriations for Coronavirus Health Response and Agency Operations

Title XII, Department of Housing and Urban Development

Division B sets out additional agency appropriations to enhance agency preparedness in the face of the threats raised by the coronavirus. These sums include additional funds to the Department of Housing and Urban Development (HUD).

Under the CARES Act, states will receive an additional $5 billion in funding to be made available to the Community Development Block Grant (CDBG) program. The CDBG program is one of the longest running examples of HUD assistance and provides funding to community-development activities with a view to the provision of affordable housing. Block grants can be distinguished from categorical grants in that they are less specific and afford states far more discretion in usage.

The CARES Act also provides for $4 billion in additional funding for homeless assistance grants, $1.25 billion for tenant-based rental assistance, and $685 million for public housing in addition to funding other programs designed to provide housing assistance to the elderly, people with disabilities, and people with AIDS.

This Title also appropriates $35 million to HUD, which will remain available until September 30, 2020, for coronavirus expenses and HUD salaries, and a further $15 million for the Office of Public and Indian Housing and the Office of Community Planning and Development.

Conclusions

The CARES Act has two key implications for housing. First, it provides significant relief to holders of mortgages backed by federal loans in the form of six months forbearance and immunity from eviction or fees relating to late rent payments. Absent from the CARES Act is consideration of the loan servicers themselves, who stand to suffer a six-month income shortfall of their entire federal loan portfolio. It must be assumed that this industry would seek for assistance under Titles I and IV of the CARES Act, with coronavirus relief via the Small Business Administration (SBA) or the Treasury. Second, although increased funding to the CDBG program will be welcomed, particularly by states who have broad latitude as to how to they employ this funding, operationally it will remain a challenge to distribute this assistance nationally and with any speed.