Insight

May 13, 2025

Overhaul of IRA Energy Credits: House Proposal

Executive Summary

- The House Ways and Means Committee’s draft of its reconciliation legislation proposes a significant paring back of about 60 percent of the Inflation Reduction Act energy tax credits, which would raise about $515 billion in revenue from 2025–2034.

- The proposal would repeal some energy credits immediately, including all clean vehicle credits, the alternative fuel vehicle refueling property credit, all residential energy efficiency credits, and the clean hydrogen production credit, which would raise approximately $306 billion from 2025–2034.

- It would also add phaseouts and restrictions to several credits, including the clean electricity production and investment credits, the clean fuel production credit, carbon sequestration credit, nuclear power production credit, advanced manufacturing production credit, and the credit for certain energy property, which would raise about $210 billion from 2025–2034.

Introduction

The House Ways and Means Committee released a draft of its reconciliation legislation yesterday, which proposes a significant paring back of about 60 percent of the Inflation Reduction Act (IRA) energy credits, which would raise about $515 billion in revenue from 2025–2034, according to the Joint Committee on Taxation (JCT).

The committee’s proposal would repeal some energy credits immediately, including all clean vehicle credits, the alternative fuel vehicle refueling property credit, all residential energy efficiency credits, and the clean hydrogen production credit, which would raise approximately $306 billion from 2025–2034.

The bill would add phaseouts and restrictions to several credits, including the clean electricity production and investment credits, the clean fuel production credit, carbon sequestration credit, nuclear power production credit, advanced manufacturing production credit, and the credit for certain energy property, which would raise about $210 billion from 2025–2034.

The American Action Forum’s (AAF) previous analysis establishes an evaluation framework of simplicity, efficiency, and fiscal sustainability to examine all the IRA energy provisions. Detailed information on the descriptions and special features of all the IRA energy credits is included in the previous analysis.

This analysis provides a quick overview of what is included in the House proposal, the revenue it would raise, and compares the new proposed expiration date to what is included in current law.

Analysis

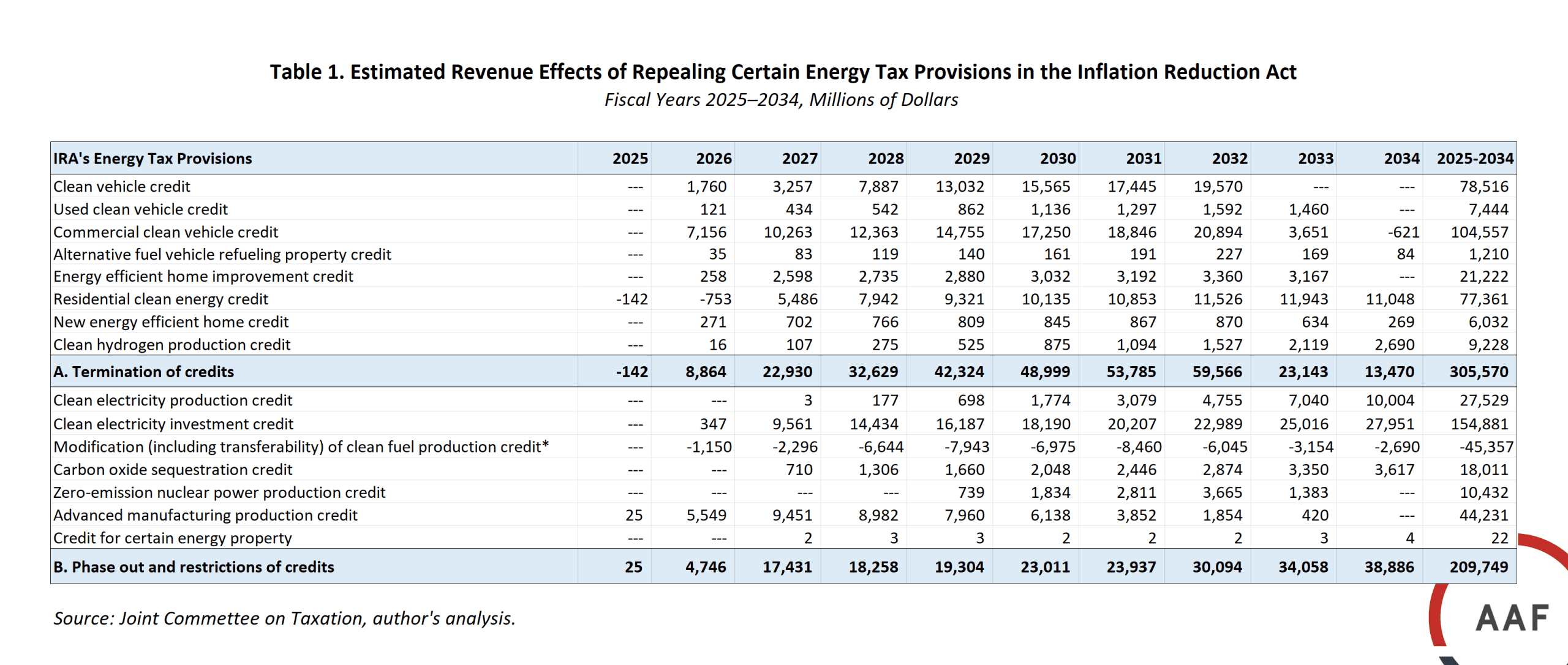

The Ways and Means Committee proposes a significant paring down of the IRA energy credits, which would raise about $515 billion in revenue from 2025–2034 according to the Joint Committee on Taxation (JCT). This accounts for about 60 percent of the revenue raised through a total repeal of all the IRA energy provisions at about $852 billion.

As shown in Table 1, the proposal would terminate several energy credits including all the clean vehicle credits (new, used, and commercial credits), the alternative fuel vehicle refueling property credit, all residential energy efficiency credits, and the clean hydrogen production credit. JCT estimates that eliminating these credits would raise approximately $306 billion from 2025–2034.

Most of these credits would be repealed immediately, effective after December 31, 2025, which is at least seven years earlier than the expiration date for most credits in current law, on December 31, 2032. (Table 2) The used clean vehicle credit and the new energy efficient home credit would be repealed after December 31, 2026.

The Ways and Means bill also proposes adding phaseouts and restrictions to some other energy credits to make them much less generous. These credits include the clean electricity production and investment credits, clean fuel production credit, carbon sequestration credit, the nuclear power production credit, advanced manufacturing production credit, and credit for certain energy property. JCT estimates that shrinking these credits would raise about $210 billion from 2025–2034 (Table 1).

There are two major ways the Ways and Means bill proposes to reduce the cost of the credits: phasing out transferability and adding restrictions related to foreign entities of concern (Table 2). Transferability is an efficiency-enhancing feature that allows energy developers with little or no tax liability to sell their credits to investors directly for cash, allowing more taxpayers to access energy credits. The proposal would retain the transferability feature for two more years and repeal it after 2027.

Additionally, the legislation would add significant restrictions related to foreign entities of concern to limit taxpayers’ access to energy credits. For example, taxpayers who are considered foreign entities of concern (FEOC), or engage in economic activities with FEOC, would not be eligible to claim the credits.

The Ways and Means bill would mostly shrink the energy credits, except for the clean fuel production credit. It would extend the credit from December 31, 2027, to December 31, 2031. It would also retain the transferability feature until the end of 2027 and require the fuel feedstock to be produced in the United States, Mexico, or Canada (Table 2). JCT estimates that modifying the clean fuel production credit would cost $45 billion from 2025–2034 (Table 1).

The Ways and Means proposal seems to be balancing between cost saving and maintaining some investment incentives for certain clean energy technologies. AAF’s previous analysis establishes an evaluation framework of simplicity, efficiency, and fiscal sustainability to examine all the IRA energy provisions. The analysis concludes that the clean vehicle credits are complex, inefficient, and costly. The committee proposes repealing all the clean vehicle credits after 2025 for used and commercial ones, and after 2026 for new ones, which would raise close to $200 billion from 2025–2034.

The committee’s proposal for overhauling the IRA energy credits is far from what final legislation would look like. But it gives investors and energy developers an important starting point for which energy tax credits lawmakers are considering modifying.

Table 2. Proposed Repeal of IRA Energy Credits by the House Ways and Means Committee

| IRA Energy Credits | House Ways and Means Committee Proposal | Current Law Expiration Date | |

| Summary | Proposed Expiration Date | ||

| Clean vehicle credit | Limits the number of covered vehicles sold per manufacturer to 200,000 from 2009–2026 | December 31, 2026 | December 31, 2032 |

| Used clean vehicle credit | Repeals the credit immediately | December 31, 2025 | December 31, 2032 |

| Commercial clean vehicle credit | Repeals the credit immediately, except for vehicles acquired before May 12, 2025, and used before January 1, 2033 | December 31, 2025 | December 31, 2032 |

| Alternative fuel vehicle refueling property credit | Repeals the credit immediately | December 31, 2025 | December 31, 2032 |

| Energy efficient home improvement credit | Repeals the credit immediately | December 31, 2025 | December 31, 2032 |

| Residential clean energy credit | Repeals the credit immediately | December 31, 2025 | December 31, 2034 |

| New energy efficient home credit | Repeals the credit except for the construction of qualified homes began before May 12, 2025 | December 31, 2026 | December 31, 2032 |

| Clean hydrogen production credit | Repeals the credit immediately | December 31, 2025 | Qualified facilities constructed before December 31, 2032 (credits available for the first 10 years of service) |

| Clean electricity production credit | · Brings forward the phaseout dates and eliminates the emissions reduction target

· Keeps the transferability feature for two years after enactment before complete elimination · Adds restrictions related to foreign entities |

The phaseout will begin in 2029 at 20 percent and reach 100 percent after December 31, 2031 | Will begin to phase out after the later of 2032, or when the United States meets the electricity sector’s emissions reduction goal |

| Clean electricity investment credit | · Brings forward the phaseout dates and eliminates the emissions reduction target

· Keeps the transferability feature for two years after enactment before complete elimination · Adds limits to access to credit by specified foreign entities · Modifies the low-income communities bonus credit |

The phaseout will begin in 2029 at 20 percent and reach 100 percent after December 31, 2031 | Will begin to phase out after the later of 2032, or when the United States meets the electricity sector’s emissions reduction goal |

| Modification (including removing transferability) of clean fuel production credit

(Note: This is the only credit the bill would expand.) |

· Extends the expiration date

· Keeps the transferability feature until December 31, 2027 · Requires feedstock used to produce the qualified fuel to come from the United States, Mexico, or Canada · Adds restrictions related to foreign entities |

December 31, 2031 | Fuels sold after December 31, 2027 |

| Carbon oxide sequestration credit | · Keeps the transferability feature for two years after enactment before complete elimination

· Adds restrictions related to foreign entities |

No proposed changes | Construction of the equipment must start by the end of 2032 (a 12-year credit available after a facility is in service) |

| Zero-emission nuclear power production credit | · Adds a phaseout schedule starting from 2029

· Keeps the transferability feature for two years after enactment before complete elimination |

The phaseout will begin in 2029 at 20 percent and reach 100 percent by 2032 | December 31, 2032 |

| Advanced manufacturing production credit | · Keeps the transferability feature until December 31, 2027, before complete elimination

· Adds restrictions related to foreign entities |

· Wind energy components sold after December 31, 2027, are not qualified

· The credit for all other qualified products, including critical minerals, expires after December 31, 2031 |

The credit for critical minerals is permanent; starts to phase out in 2030 with a reduction of 25 percent annually over four years |

| Credit for certain energy property | Keeps the transferability feature for two years after enactment before complete elimination | Brings forward the phaseout of the investment credit for geothermal heat pump property to December 31, 2031 | Placed in service before January 1, 2025, except for geothermal heat pump property, which must be in service by 2035 |

Source: Joint Committee on Taxation, Evaluating the IRA’s Clean Energy Tax Provisions, author’s analysis.