Insight

March 12, 2025

Primer: Can the President Impound Federal Spending?

Executive Summary

- Since beginning his second term, President Trump has signed a flurry of executive orders, some of which pause congressionally appropriated funding.

- Critics of these actions argue they are unconstitutional and go beyond the scope of the president’s impoundment authority.

- This primer provides an overview of the executive branch’s impoundment authority, which allows the president to withhold congressionally appropriated funds from their intended use; these impoundments are sorted into two categories: deferrals and rescissions.

Introduction

Since beginning his second term, President Trump has signed a flurry of executive orders, some of which pause congressionally appropriated funding. Critics argue his actions are unconstitutional and go beyond the scope of the president’s impoundment authority, which is the power of the president or the executive branch to withhold congressionally appropriated funds from their intended use. President Trump has previously argued the executive branch’s impoundment authority is long-recognized and undisputed, though Congress has acted in the past to limit this power, most significantly through the Congressional Budget and Impoundment Control Act of 1974 (ICA).

This primer provides an overview of the issue of the executive branch’s impoundment authority.

An Overview of Impoundment Authority

Article I of the U.S. Constitution gives Congress the authority to appropriate funds and impose taxes – otherwise known as “the power of the purse.” The executive branch, meanwhile, is responsible for spending the funds – through the Office of Management and Budget (OMB) – for the purposes Congress intended. As head of the executive branch, the president is theoretically in a position to circumvent Congress’ power of the purse and order agencies not to spend certain funds appropriated by Congress, but instead either defer spending the funds or rescind them altogether. This process is known as impoundment, and presidents have used their impoundment authority when Congress has appropriated funding for a purpose that is no longer needed.

The use of impoundment dates back to the early 1800s. In 1803, Congress appropriated $50,000 to build 15 gunboats in response to Spain’s refusal to allow the United States to access the Port of New Orleans. In response to the successful negotiation of the Louisiana Purchase, President Jefferson advised Congress that the appropriated funds for the gunboats remained unspent because the “favorable and peaceful turn of affairs on the Mississippi rendered an immediate execution of that law unnecessary.”

There were instances of presidential impoundment throughout the rest of the 19th and 20th centuries. For example, following the enactment of the Rivers and Harbors Act of 1876, which appropriated $75,000 to improve navigation on the Ohio and Mississippi Rivers, President Grant indicated he did not intend to spend the full amount because certain funding was geared toward private and local interests and not purely national interests. In the early 1940s, President Franklin Roosevelt annually impounded $1.6 to $95 million of funds that Congress had appropriated for various civilian and military efforts; between 1940 and 1943, he refused to spend over $500 million of public works funding. In 1949, President Truman impounded $735 million appropriated funds for Air Force groups, arguing the impoundment was needed to maintain a balance between national security and a sound economy. In 1956, President Eisenhower impounded $46 million of funds to increase Marine Corps personnel; in 1959, he impounded nearly $334 million that had been appropriated for various purposes. President Kennedy in 1961 impounded $180 million of the $380 million Congress had appropriated for the B-70 strategic bomber.

During the Vietnam War, President Johnson made broader use of presidential impoundment authority to defer billions of dollars of appropriated funds in an effort to cool inflationary pressures in the economy. The use of impoundment authority reached new heights during the Nixon Administration, with a chronic refusal to release congressionally appropriated funds for programs the president opposed. Specifically, President Nixon placed a moratorium on subsidized housing programs, suspended community development activities, and reduced disaster assistance.

In response to the heightened use of impoundment, Congress took steps to limit the executive branch’s impoundment authority via the ICA which codified Congress’ power of the purse. Title X of the law – Impoundment Control – established procedures to keep the president and other executive branch officials from unilaterally replacing Congress’ spending decisions with their own. The ICA limited impoundments by sorting them into two categories: deferrals and rescissions. It also established a fast-track process in Congress to disapprove a proposed deferral. For a proposed rescission, the ICA provided a different fast-track process for Congress to approve the proposed rescission.

An Overview of Deferrals

A deferral is a temporary delay in available funds. While the executive branch is required by law to spend congressionally appropriated funds, the president may set appropriated funds aside until later in a fiscal year (FY). The ICA allows deferrals under three circumstances: to provide for contingencies, to achieve budgetary savings made possible through improved operational efficiency, or as specified by law. Notably, the president cannot defer funds simply because he or she does not agree with Congress’ appropriations decisions.

To defer funds, the president must first send Congress a special message with the proposed deferrals. The message must include: the amount of budget authority (BA) to be deferred; the specific accounts where the BA resides; the amount of time during which the BA is to be deferred; an explanation of why the BA should be deferred; the estimated fiscal and economic impacts of the deferral; and the impact on the programs and functions that would be affected. Upon sending this information to Congress, the funds may be deferred without further congressional action. OMB effects presidential deferrals through the apportionment process. A deferral cannot last longer than the FY in which the President’s special message is transmitted to Congress.

During his first term, President Trump was accused by Congress of violating the ICA by withholding $214 million of security assistance funding to Ukraine. While President Trump did not utilize impoundment to withhold these funds (he did not transit a special message to Congress outlining his proposal), he relied on apportionment – which would have slowly disbursed the funds on a schedule – to carry out what was essentially a deferral on congressionally appropriated funding. The Trump Administration eventually released its hold on the funds.

An Overview of Rescissions

A rescission is a permanent cancellation of designated BA. While the executive branch is required by law to spend congressionally appropriated funds, the president may temporarily delay the spending of BA that he or she views as unworthwhile, while asking Congress to cut the spending altogether. Congress can pass a rescissions package with a simple majority in the Senate, instead of the 60-vote supermajority needed to overcome a filibuster. The presidential rescission process was last used in 2021 during the first Trump Administration to rescind some COVID-19 relief funding. The rescissions process for the executive branch is different than when Congress initiates its own rescission measures, typically within appropriations legislation to offset other spending increases.

To rescind funds, the president must first send Congress a special message with the proposed rescissions. The message must include: the amount of BA to be rescinded; the specific accounts where the BA resides; the projects and functions that would be affected; an explanation of why the BA should be rescinded; and the estimated fiscal and economic impacts of the rescission and the impact on the programs and functions that would be affected.

The funds identified in the special message may be temporarily reserved or withheld from being spent. The special message starts a 45-day clock (minus days both the House and Senate are in recess for more than three days or Congress adjourns sine die). If Congress does not complete work on legislation that rescinds all or part of the amounts proposed, the funds must be made available to spend.

Once Congress receives the president’s special message, it is referred to the House and Senate Appropriations Committees. The committees have 25 days to either approve, disapprove, or amend the president’s request. If they do not act within this timeframe, the measure is subject to discharge from the committees and can go to the full House and Senate for consideration. Once the full chambers have the rescission measures – either through the committee process or discharge – they can act on it. Debate on the measure is limited to two hours in the House. In the Senate, it is limited to 10 hours, thus debate in the Senate is not subject to the cloture requirement of 60 votes to stop debate.

If the rescissions measure passes both the House and Senate, the BA is rescinded. If, however, either of the Appropriations Committees or the full House or Senate disapproves the measure, or the 45-day clock runs out, the process stops, and the president must spend the money and cannot propose to rescind it again.

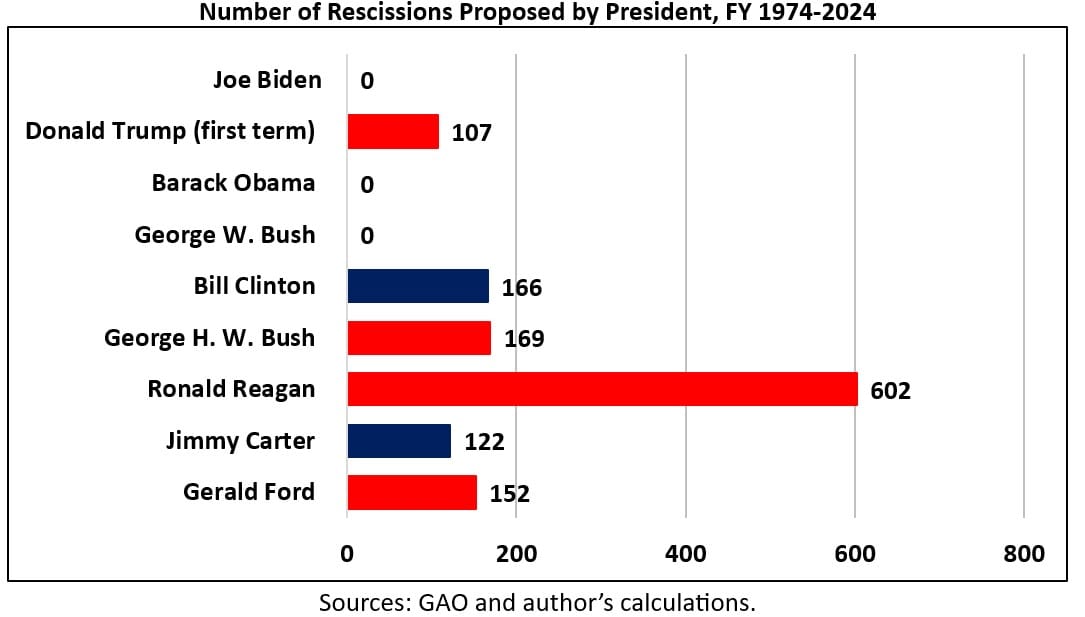

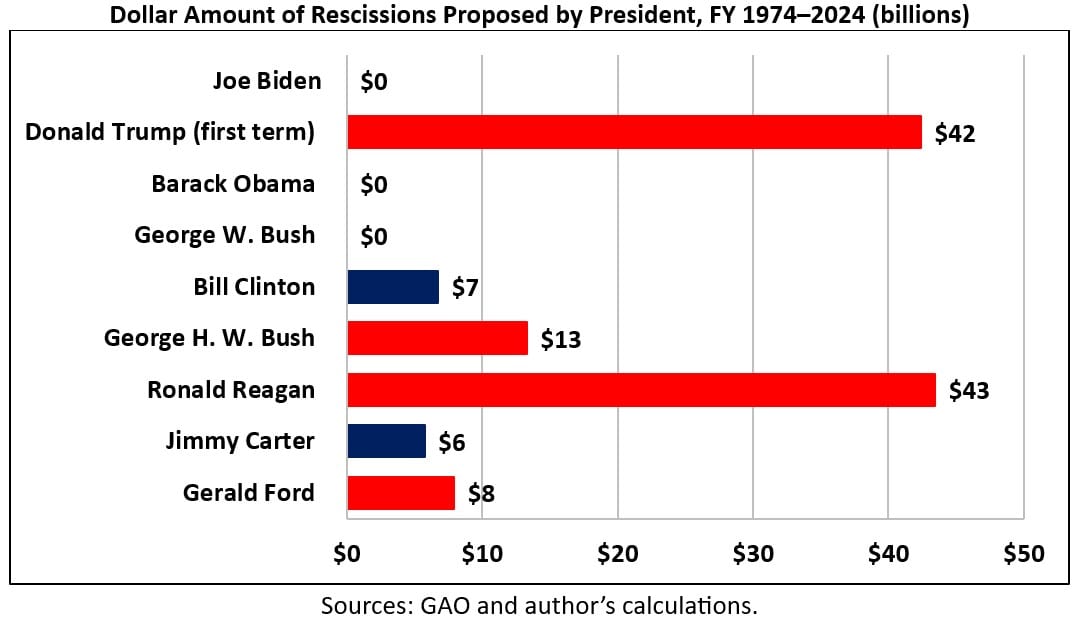

According to the Government Accountability Office (GAO), between FY 1974 and FY 2024, presidents proposed 1,318 rescissions totaling over $119 billion. During their time in office, Presidents George W. Bush, Barack Obama, and Joe Biden did not submit any rescissions proposals to Congress.

During his first term, President Trump sent two rescission proposals to Congress. On May 8, 2018, President Trump sent a special message to Congress proposing $15.3 billion of rescissions from 38 appropriations accounts. He updated and revised his initial request on June 5, 2018, with a supplemental special message to Congress that ended his previous message by proposing $14.8 billion of rescissions from 34 appropriations accounts. The package failed to secure passage in Congress.

On January 14, 2021 – just a week before ending his first term – President Trump sent a special message to Congress proposing $27.4 billion of rescissions from 73 appropriations accounts. The proposal primarily targeted funding in the Consolidated Appropriations Act, 2021 that combined COVID-19 relief with ordinary appropriations. By submitting the request just before leaving office, President Trump triggered a temporary hold on the funds and triggered a 45-day clock for Congress to address the rescissions request or for President Biden to rescind the request. President Biden rescinded the request on January 31, 2021.

Impoundment During President Trump’s Second Term

President Trump greatly utilized presidential impoundment authority during his first term in office and is doing so again during his second. On January 20 he signed an executive order that froze all foreign assistance funding for 90 days and ordered a review of all U.S. development work abroad. Another executive order signed that day froze the disbursement of all appropriated funding from the Inflation Reduction Act and the Infrastructure Investment and Jobs Act, while an additional executive order froze federal funding for sanctuary cities. Additionally, a January 27 OMB memo to all heads of executive branch departments and agencies paused agency grant, loan, and other financial assistance programs. These executive actions were all met with swift criticism and legal action. Though it is difficult to place an exact figure on the amount of funding that, if any, will ultimately be impounded through these actions, the number is likely to exceed the amount President Trump sought to impound during his first term.