Insight

February 19, 2025

The Inflation Reduction Act and Medicare

Executive Summary

While the Inflation Reduction Act (IRA) is primarily viewed as a major expansion of clean energy subsidies, it also had enormous implications for Medicare, especially Parts B and D, and broader federal health policy. This paper surveys recent American Action Forum research on the IRA and Medicare, emphasizing:

- The IRA is advertised as helping every senior; in fact, only a minority of seniors gets direct assistance, and all the budgetary savings are diverted to clean energy subsidies.

- The IRA drug “negotiation” process cannot match market incentives for price reductions, sets a dangerous precedent for using taxes to implement economy-wide price-fixing, and hampers innovation incentives for drugs and biologics.

- The implementation of the Part D redesign was bungled, threatening higher premiums, dramatic formulary changes, and fewer Part D plans; the subsequent bailout by a demonstration program undercuts the original intent.

The IRA is a dramatically failed Medicare policy. Its few positive reforms should be retained while the vast majority is transformed to restore the integrity of the original Part D program design.

Introduction

The Inflation Reduction Act (IRA) is most commonly associated with Biden Administration climate policy; in particular, a dramatic and expensive array of subsidies to clean energy investment and production. Yet it also contained several key policies toward Medicare drugs. The first are so-called “inflation taxes” that require drug manufacturers to remit the excess of drug price increases over general inflation to the federal treasury. The second are so-called drug “negotiations” over the Medicare price of selected prescription drugs. Finally, there is a redesign of the basic Part D drug benefit that places more of the cost of the benefit on manufacturers and, especially, drug plans.

These changes in the law have dramatic impacts on Parts B and D in Medicare. The American Action Forum (AAF) has done extensive research into the implications of the IRA for Medicare. This paper summarizes these efforts.

As a general matter, the IRA was a step in the wrong direction for Medicare policy. Yet in light of the few beneficial reforms, a strategy of targeted legislation is more desirable than a simple repeal.

Who Benefits From the IRA?

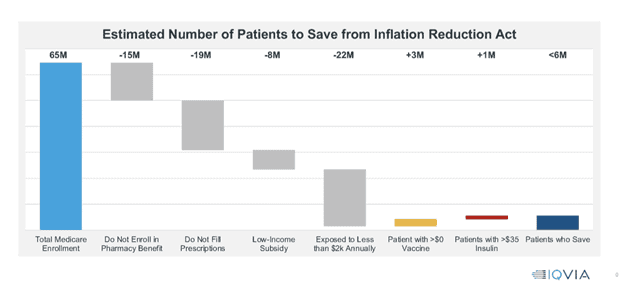

The IRA was sold as reducing drug costs for seniors. This is far from the case. To begin, the chart below displays those directly benefiting from the reform. At present, there are 65 million individuals enrolled in Medicare, but 15 million of those are not enrolled in the pharmacy benefit, meaning they cannot benefit from the IRA’s drug cost-saving provisions.

Another 19 million beneficiaries have no prescriptions to fill and will also not benefit. Similarly, 8 million are enrolled in the low-income subsidy population, which is already protected from out-of-pocket costs and will not benefit from the IRA. Finally, 22 million seniors enrolled in Medicare have prescription drug expenses and are exposed to out-of-pocket costs but have annual spending that falls below $2,000 and will not benefit from the hard cap on catastrophic drug costs. The small remainder will benefit from the redesign of the Part D benefit.

There are two other ways to save from the IRA. The IRA made vaccinations free, which produces savings for about 3 million beneficiaries, and it placed a $35 monthly limit on insulin expenses. The latter proposition helps another 1 million seniors.

But the bottom line is striking. Of the 65 million Medicare beneficiaries, only 5.6 million are benefited by the IRA.

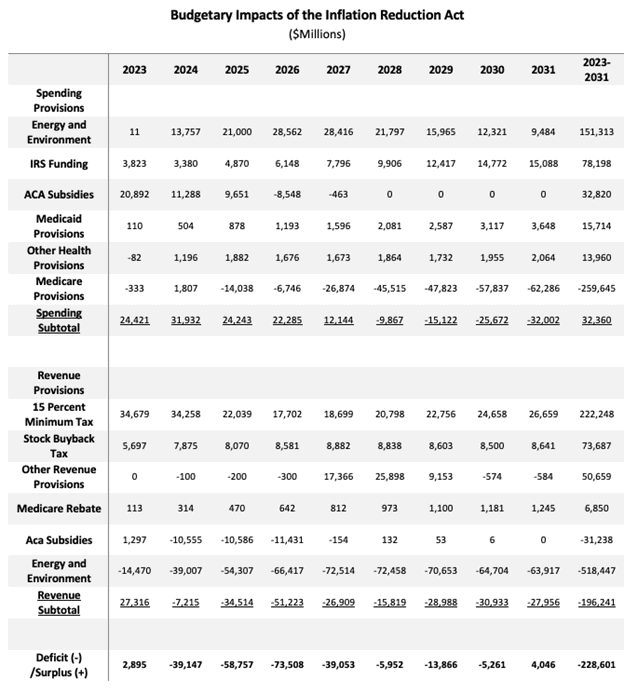

Looking from a broader perspective, as noted above the IRA contains two key drug provisions that will reduce federal outlays: the inflation taxes (100 percent of any increase in the price of a drug above the general rate of inflation must be returned to the federal government) and the drug price “negotiation” in which the Department of Health and Human Services (HHS) secretary sets the maximum fair price on selected drugs each year. Together, these (and other) provisions were originally estimated to amount to the $260 billion in savings over the budget window.

Yet the other major feature of the IRA is the law’s large amount of spending on energy and the environment, as well as tax credits for clean energy. There is $670 billion in spending and new tax credits, of which only $182 billion is offset elsewhere in the IRA. That leaves $488 billion in energy spending and credits that consume all the Medicare savings of $266 billion.

In sum, few seniors benefit directly, and any broad budgetary savings are taken from Medicare to finance energy subsidies.

Inflation Penalty

Under the IRA, single-source Part B drugs and all Part D drugs excluding certain low-spend drugs will be subject to a penalty if the drug’s price increases faster than inflation. This penalty will take the form of a rebate to Medicare on all units sold in Parts B and D at an amount over the allowed price increase.

Medicare Maximum Fair Price Process

The IRA includes language that requires Medicare to set prices (known as the maximum fair price, or MFP) for select drugs, a process the legislation calls “negotiation.” Drugs will be initially selected in 2023 and the prices set will be applied beginning in 2026. Drugs eligible for selection are defined as those among the 50 single-source drugs with the highest total expenditures in either Part B or Part D and are at least seven years past their Food and Drug Administration approval date.

The IRA sets up a process for developing an MFP. Manufacturers that do not comply with the price-setting process, including not engaging in the process or agreeing to an MFP, will be charged an increasingly large excise tax ultimately reaching 95 percent. Note that the 95 percent rate is rate applied to the tax-inclusive price. The effective rate of tax on the price received by the seller is therefore 1900 percent. This means, for example, that the manufacturer would pay $190 in taxes on a sale that yields $10, for a total retail price of $200.

Perverse Incentives in Selecting Drugs

The process begins with the selection of the first 10 drugs, which were selected from the 50 with the greatest Medicare Part D spending by September 1, 2023. Leading the list was Eliquis, an anticoagulant that treats blood clots. What was even more interesting is that coming in at number three is another blood thinner, Xarelto. (Further down is a third, Pradaxa.) Both of these entered the “negotiation” regime, but neither was particularly expensive when the drugs were selected when measured by cost per dose ($8.50 and $16.40, respectively), cost per claim ($739 and $809), or cost per beneficiary ($4,023 and $4,153). The league-leaders in those categories came in at $42,825, $304,487, and $1.6 million.

These aren’t the high-priced poster children of drug negotiation. These are simply widely prescribed modern therapies. They also compete head-to-head for market share among seniors, not just by price but also by paying rebates for preferred placement on drug plans’ formularies, i.e., a tier having little or no cost-sharing for the beneficiaries.

What happens when the Centers for Medicare and Medicaid Services (CMS), in charge of setting the MFP, starts price-fixing? Suppose that the MFP is set at the old “net price” – the price after paying rebates. If so, the plans get this low price automatically but have no particular incentive for formulary placement. Moreover, the IRA implementation rules specify only that the plan must keep the drug on the formulary, with no mention of the tier on which the drug must be placed. In this scenario, it could easily be the case that the manufacturers are unscathed, the plans are better off, and the only loser is the beneficiaries who now have greater out-of-pocket costs and less access to the therapies.

The “Pill Penalty”

The IRA permits CMS to start the MFP process for small molecule drugs at seven years with those prices going into effect at nine years after they come to market. For large molecule drugs, or biologics, the IRA sets these timelines at 11 years, with those prices going into effect 13 years post market entry. This discrepancy is called the “pill penalty.”

Notice that there are fewer years in which to recoup the investment in a small molecule pharmaceutical, which is a clear disincentive to innovate. Schulthess et al. show that the impact on small molecule research is dramatically larger than large molecule research – one manifestation of the pill penalty.

More generally, critics of the IRA have been concerned with the impact of the IRA MFP regime on the incentives to innovate. For the authors of the IRA, any pill penalty construct is effectively a self-defeating feature. Shortening recovery times appears to save budget dollars, but eventually private innovation will dry up and any potential budget savings will dissipate.

Evidence to Date

In August, CMS announced the MFPs for the first 10 drugs to enter the “negotiation” regime under the IRA. This small sample of data is the first genuine head-to-head comparison of what reliance on private negotiation – the original raison d’etre of the Medicare Part D program – yields versus government intervention into prices. The results speak poorly for the IRA.

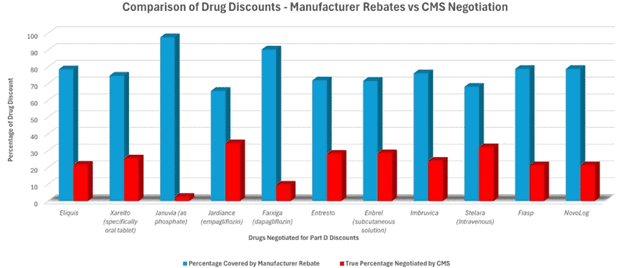

The graph below compares the discount from list price negotiated in the private sector (blue bars) compared with the additional discount (red bars) achieved by IRA to set MFPs (data comes from HHS). There are two basic takeaways:

- Despite being armed with enormous artillery (confiscatory taxes, the possibility of banning sales of all a company’s drugs in Medicare, negotiations conducted in secret with no public scrutiny, etc.), the IRA didn’t accomplish much.

- Or perhaps the IRA accomplished all that it could. Put differently, perhaps it is very expensive to invent, develop, test, and market drugs – so expensive that there was little left to extract from the manufacturers.

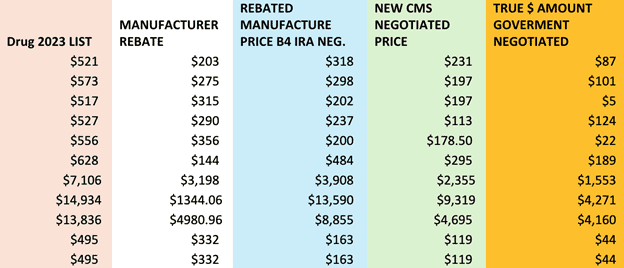

It turned out that the savings were a lot smaller than advertised (see chart below). The White House was comparing the MFP to the list price (pink), which is a clear overstatement because private negotiations have already yielded rebates (white) that lower the net price (blue) prior to the IRA regime (orange). The right comparison is net price versus list price for the private sector and MFP versus net price for the IRA. On that front, the median manufacture rebate was about $315 versus the median IRA reduction of $101.

As explained in a Health Affairs study on list versus net prices, “It has been abundantly clear for some time that the list price of a drug greatly differs from the net price, which incorporates discounts and rebates, and that the use of list price leads to misleading results.”

A better route for Part D would be to junk the negotiation regime and focus on gradually instituting the Part D redesign that was intended to return the program to its private-sector roots.

Price Fixing

As noted above, the MFP regime contains an excise tax that is 95 percent of the manufacturer’s sales prices. When the tax is expressed as a percentage of the revenue the manufacturer receives from the sale, the effective rate is 1,900 percent. This means, for example, that the manufacturer would pay $190 in taxes on a sale that yields $10, for a total retail price of $200.

There are two significant implications of this. First, if a company was ever subjected to the tax, it would be passed along to purchasers in the form of a higher price. (Note that the Internal Revenue Service draws the same conclusion.) Indeed, it would be a much higher price – $200 versus $10 in the example above. Second, in its analysis of the IRA, the Congressional Budget Office (CBO) projected that the excise tax would raise no revenue. Given the magnitudes involved, this can only imply that CBO does not expect it to ever be used. Unlike other taxes, the excise tax has no revenue function and exists only to support the price controls.

Though disguised as voluntarily determined pricing, the MFP process is opaque, and the corresponding threat of its punitive excise tax reveals the damaging nature of its price controls, as was demonstrated during the first year of the MFP process. Lawmakers, whose fondness for price controls is in many cases long-standing, may view the “negotiation” of MFPs as a promising approach to impose price controls in many other markets.

Part D Benefit Redesign

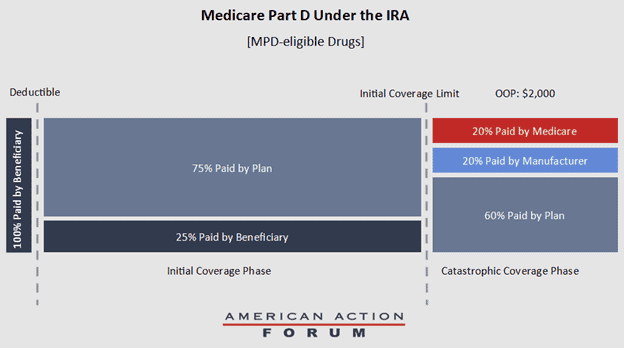

Beginning this year, the basic Medicare Part D benefit will undergo a substantial redesign with the introduction of a lowered out-of-pocket maximum for beneficiaries and the elimination of the coverage gap. Specifically, beneficiaries will not pay more than $2,000 out-of-pocket in a given year on Part D drugs.

The IRA establishes the Manufacturer Discount Program (MDP), which would require a 10-percent discount on the Part D negotiated price for a beneficiary in the initial coverage phase, and a 20-percent discount for beneficiaries in the catastrophic phase. Drugs eligible for this discount include all Part D drugs except those subject to the price-setting requirements mentioned above. If a beneficiary in the initial coverage phase is dispensed a drug subject to the price-setting requirements, Medicare must provide the plan with a subsidy equal to 10 percent of the drug’s MFP.

Medicare would reduce its reinsurance payments to 20 percent in the catastrophic phase for Part D drugs eligible for the MDP, and 40 percent for drugs not eligible for the MDP. These changes mean that, in the catastrophic phase, plan sponsors will be responsible for 60 percent of the costs, as opposed to the current level of 15 percent and, for MPD-eligible drugs, manufacturers will be responsible for 20 percent of the costs and Medicare will be responsible for the final 20 percent (see figure below).

Part D Benefit Under the IRA for MPD-eligible Drugs

Additional changes to Part D include: Limiting copays for insulin to $35 a month for beneficiaries, allowing beneficiaries to choose to pay out-of-pocket costs on a monthly basis subject to a cap, known as “smoothing”; expanding low-income-subsidy-eligible (LIS) beneficiaries from those below 135 percent of the federal poverty level (FPL) to those below 150 percent of the FPL starting in 2024; and covering all vaccines recommended by the Advisory Committee on Immunization Practices with no cost sharing to beneficiaries.

As a result of the IRA and its sweeping changes to Medicare Part D, stand-alone drug plans and Medicare Advantage (MA) prescription drug plans will face substantial new costs for both seniors’ catastrophic drug expenses and the LIS population. The actions that plans may take in response would likely have significant impacts on Medicare beneficiaries.

AAF estimates that in the absence of a behavioral response by plans to compensate for these costs, the IRA’s provisions will increase the costs of Part D plans by roughly $48 billion per year. This is a dramatic increase as the combined profits of Part D plans are about $4.6 billion annually.

According to KFF, the typical Medicare beneficiary could choose among 54 plans in 2022 – 23 stand-alone plans and 31 MA-PD plans. These plans are popular with seniors: According to polling from Medicare Today, 88 percent of beneficiaries said they were satisfied with their Part D plan and 86 percent said their plan provided good value. In short, the Part D program is functioning well for beneficiaries. Despite this, the IRA provisions require significant changes to those plans.

Premium Increases

One response to the IRA’s higher liability for plans would be for plans to simply adjust their bids to account for their higher liability, resulting in an increase in federal subsidies but also an increase in premiums. The law provides that, as of the beginning of last year, the average premium increase must be limited to 6 percent over the previous year. This, in fact, became evident in fall 2024 as plans announced new premiums. The administration responded with a demonstration project called the Premium Stabilization Demonstration, which provided cash to ameliorate the premium pressures. Nevertheless, there is still upward pressure on premiums.

Negotiation with Manufacturers

The original insight embedded in the Part D design was that plans would have an incentive to bargain with manufacturers for lower drug prices. The IRA provisions sharpen this incentive substantially. One can anticipate that collectively Part D plans will seek to reduce their acquisition costs considerably. Their ability to be successful is unclear. Notice, however, that if plans are successful in pushing these costs onto manufacturers, it would entail less disruption of the existing plan offerings. Unfortunately, it would also mean a bigger impact on manufacturers’ drug development.

New Plan Offerings

MA has seen a dramatic rise as a popular platform for delivering medical services to seniors, with a majority of beneficiaries likely to be covered by MA in the next few years. As a result, the number of stand-alone Part D plans declined from 1,198 in 2012 (one-third of plans) to 1,006 in 2022 (under 20 percent of plans). At the margin, the IRA provisions may contribute to this trend. Because the profit margins are better in the MA setting than in the stand-alone plans, insurers may react to the cost pressures by focusing their offerings in MA.

Changes in Formularies

The next logical possibility is that plans – or new plan offerings – will rely on formularies that are adjusted to reduce likely drug spending. While plans do have some mandatory formulary coverage requirements in Part D, such as at least two drugs per class and all or substantially all drugs in the six protected classes, plan formularies today typically exceed the minimum requirement of two drugs per class. In an effort to minimize drug spending, plans could opt to reduce the number of medicines covered, resulting in more narrow formularies.

Utilization Management

A final avenue for plans to respond to the IRA is to control spending on unnecessary prescriptions or unnecessarily expensive prescriptions through tools such as prior authorization or step therapy. The main question is the extent to which insurers import their commercial market cost-control protocols into the management of their Part D book of business. It seems unlikely, for example, that Part D would transform to look like the commercial market as the minimum requirements for formularies and the potential for both political and regulatory pressure are much greater in Part D.

Nevertheless, the financial incentives for plans to increase their management of utilization are strong and clear. It is worth monitoring the response of plans over time.

Evidence Thus Far

The IRA made no provision to phase in or otherwise manage the return of strong cost-saving pressures. The increased responsibility to cover the cost of the benefit inevitably forced the plans to stay in business by scrambling to raise premiums. AAF found that premiums rose by 21 percent from 2023 to 2024. With the arrival of full premium pressures, the question becomes: “How much might Part D premiums jump in response to a 179-percent increase in bid amount compared to last year?”

Under the threat of electoral backlash, the CMS announced a “Premium Stabilization Demonstration,” which would funnel approximately $7.2 billion to insurers, reducing the need to raise premiums and keeping the plans in business. Just like that, the market incentives disappeared, and Part D was pushed back to being a borrow-and-spend entitlement program.

The near-term threat has seemingly been neutralized, but the real evil is the three-year nature of the “Stabilization Demonstration.” It removes any incentive for the plans to change their business models to accommodate the new pressures on premiums and costs.

Conclusions

The IRA is a dramatically failed Medicare policy. Its few positive reforms should be retained while the vast majority is transformed to restore the integrity of the original Part D program design. While the IRA is advertised as helping every senior, in fact, only a minority gets direct assistance, and all the budgetary savings are diverted to clean energy subsidies.

In addition, the IRA drug “negotiation” process cannot match market incentives for price reductions, is a dangerous precedent for economy-wide price-fixing, and hampers innovation incentives for drugs and biologics. Finally, the implementation of the Part D redesign was bungled; threatened higher premiums, dramatic formulary changes, and fewer Part D plans; and the subsequent bailout by a demonstration program undercuts the original intent.