Insight

May 22, 2025

The State of Housing Finance

Executive Summary

- Evidence is mounting of a growing housing crisis in the United States, as shelter remains a key component of stubborn inflation.

- Congress and the administration must look toward lowering the barriers to new construction and wholesale reform of housing titans Fannie Mae and Freddie Mac.

- The Trump Administration risks exacerbating the housing crisis with its approach to tariffs, immigration, the potential sell-off of Fannie Mae and Freddie Mac, and widescale firings across the federal government.

Introduction

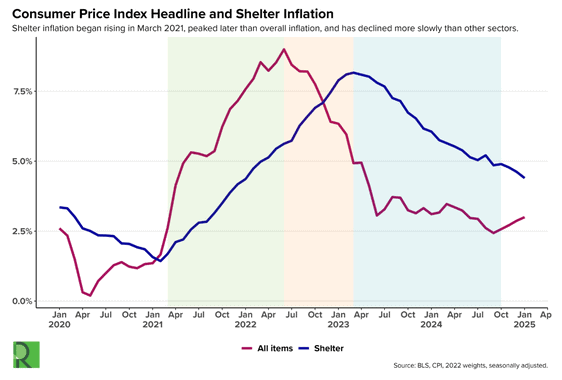

Post-pandemic inflation remains above the two-percent target set by the Federal Reserve. While other aspects of the basket of goods and services tracked by the Bureau of Labor Statistics have eased, shelter inflation remains high, accounting for 35 percent of the consumer price index, more than any other category. Shelter inflation has also behaved differently, peaking later than overall inflation and declining significantly more slowly.

This reflects the ongoing housing crisis in the United States, which faces a shortage of an estimated 4.5 million homes. Mortgage rates, rents, and homelessness are high, while housing affordability is low. High housing costs have a knock-on effect on the broader economy, with a significant impact on consumer spending. It is with these issues in mind that Congress and the administration must consider the hurdles and challenges of the housing finance sector. Yet it is becoming increasingly clear that since the 2007 financial crisis, the significant drivers of dysfunction in the housing market have been Congress and successive administrations themselves.

Tariffs and Immigration

The vast majority of economists believe that tariffs are a tax on consumers that will only raise prices and worsen inflation (although many of those economists expected greater impacts sooner). For housing finance, these impacts are or will be particularly felt in construction. The United States and most developed countries fundamentally have a housing supply problem – inventories are far lower than demand. Nothing will solve this problem short of a great deal more homes, which means Congress and the administration must look toward incentivizing construction by lowering costs and reducing regulatory barriers.

Instead, in March President Trump levied a 25-percent tariff on all goods coming out of Canada and Mexico. Nearly 25 percent of all softwood supply in the United States comes from Canada, making up 85 percent of all U.S. softwood lumber imports. Mexico is a significant exporter of gypsum, concrete, and other key construction cost drivers. In a now characteristic policy volte-face, Canadian lumber was subsequently specifically exempted from all tariffs once it became clear to the Trump Administration that without this lumber few new homes will be built in the United States. But this moment of sanity may be short-lived as timber and lumber remain “under investigation” by the administration for further tariffs. Equally, it is likely that the tariff environment and its impacts on inflation force the Fed’s hand, leading to rates that are higher for longer, making mortgage finance more expensive.

The other aspect of home construction under threat is the supply of labor. Construction depends heavily on immigrant labor, and low supply was already impacting the cost of construction for homebuilders. More than half of all immigrant construction labor live in just four states: California, Texas, Florida, and New York. A 2024 National Association of Home Builders study indicated that “immigrants account for 64% of plasterers and stucco masons, 52% of drywall installers, 48% of painters, and 47% of roofers. Additionally, 41% of all laborers and a third of all carpenters are foreign-born.” This combination of factors make construction especially vulnerable to a mass deportation scenario or the looming specter of Immigration and Customs Enforcement raids on construction sites.

An Unclear Path to GSE Reform

Any consideration of the state of housing finance continues to be dominated by Fannie Mae and Freddie Mac. In the wake of the 2008 financial collapse, the federal government created regulatory bodies to oversee aspects of the financial services industry, most notably the Federal Housing Finance Agency (FHFA) and the Consumer Financial Protection Bureau (CFPB). Congress passed the Housing and Economic Recovery Act of 2008 (HERA), and in so doing, created the FHFA as a brand-new supervisory agency to regulate the housing market. HERA was designed to prevent the collapse of mortgage giants and government sponsored enterprises (GSEs) Fannie Mae and Freddie Mac, but just six weeks after HERA was signed the FHFA made both wards of the state via conservatorship. Always intended to be a temporary fix, the GSEs remain – too useful a tool to address housing policy goals by deliberately flouting the risk standards applying to all other private mortgage providers. Over a decade later, the GSEs have abused their privileges and size to compete with the private sector, crowding out private capital by performing functions outside their charter.

The first Trump Administration saw the most significant steps taken in over a decade to reform, replace, or raze the GSEs under FHFA Director Mark Calabria. Director Calabria’s approach in some ways preserved this uneasy dichotomy by simultaneously reducing the risk posed by the GSEs to the broader market and the chances of a second government bailout, while failing to empower private industry and seemingly preserving the GSEs as the prime actors in this space. Still, that the GSEs were slightly less likely to cause another financial collapse is to be valued, and this was more than any previous administration had managed to accomplish.

Hopes that these activities would continue into the second Trump Administration have withered. Instead, the focus seems to be on the enormous cash cow (about $250 billion) the GSEs represent. Selling the government stake in the GSEs seems to be the goal; potentially funding an extension of the previous administration’s tax cuts. More recently, Treasury Secretary Scott Bessent floated the idea of transferring the government’s stake in the GSEs to a newly created sovereign wealth fund that would “invest” in bitcoin.

Even setting aside the host of policy issues these proposals create, this would represent possibly the worst outcome for the housing finance market. Keeping the GSEs as wards of the state until the next financial crisis is untenable but privatizing them in whatever form without enacting the necessary reforms required is somehow worse. The GSEs have spent a decade using taxpayer funds to invade nearly every aspect of the housing market, providing services that actively invite risk and destabilize markets. In their current form the GSEs are too big to fail; in the event of a crisis, the federal government would have to bail them out, again. That implicit guarantee creates moral hazard, and hamstrings private industry from ever competing on an even footing and offering appropriate products at risk-based prices. Prior to releasing the GSEs from conservatorship, policymakers must achieve comprehensive reform that prevents the GSEs from needing another government rescue and establishes the necessary guardrails to enable private industry to compete on a more level playing field.

DOGE and Program Cuts

Only three days into his term, FHFA Director Bill Pulte invited scrutiny for firing over half of the boards of GSEs Fannie Mae and Freddie Mac and installing himself as chair. Representative Maxine Waters, senior Democrat on the House Financial Services Committee, referred to the move as indicative of the “growing politicization” of the agency, and noted that the move was likely to undermine the FHFA’s mission and lead to both uncertainty in the mortgage markets and higher mortgage rates. Waters also requested Director Pulte clarify his relationship with the DOGE team and the degree of DOGE incursion at the FHFA.

Even if this degree of alarm is unwarranted, industry watchers should be concerned about the significant loss of institutional knowledge at a time of market uneasiness. A more optimistic observer might ask why both Fannie and Freddie are necessary given the similarity of their portfolios and view this as a step toward integration.

Representative Waters also noted Pulte’s “overhaul” of fair lending entities required by statute including the Office for Women and Minority Inclusion as part of Director Pulte’s intent to reduce the scope of multiple minority homeownership initiatives and environment programs. Over 100 Fannie employees were fired for alleged “unethical conduct,” and the FHFA itself has reduced its headcount by a quarter.

President Trump made homelessness a key part of his re-election platform, framing the issue as a Democratic weakness in light of record numbers of people living on the streets. Trump’s only policy implementation to date – slashing the funding of the Department of Housing and Urban Development by 40 percent – is likely to exacerbate rather than solve the problem, particularly given the DOGE mass firings at the U.S. Interagency Council on Homelessness. Combined, these initiatives remove any possibility of a federal response to the issues raised by homelessness; depriving the existing homeless population of emergency assistance is not a solution to the problems of homelessness (let alone the complex underlying causes).

Other Biden-era COVID countermeasures are ending or unlikely to be extended. The Emergency Housing Voucher program was created in 2021 to assist vulnerable populations in the background of the pandemic. Five-billion dollars went towards a new voucher system in what was an extension of the Section 8 program. Although initially expected to run through 2030, program administrators warn that funds will run out in late 2025 or 2026, potentially leaving up to 60,000 people without rental assistance.

The path forward is no less clear on continuing programs and current initiatives. In early January the FHFA announced the retirement of its “tri-merge” credit model (pulling credit reports from three major credit reporting agencies) to a “bi-merge” model. Despite significant concern about the rationale behind the change for a time at least there was clarity, however unpopular. Now however the implementation timeline of the roll-out of the new model is unknown and has undergone multiple delays. In this, as well as every other aspect of the housing finances landscape, a lack of transparency at best increases pricing for consumers and worst injects yet more risk into a system that bears some of the hallmarks of the 2008 financial crisis.

Conclusions

That the shelter aspect of inflation refuses to budge should be sounding alarm bells across Congress and the administration. The unaffordability of housing is poised to be the single most important policy issue facing governments for the next decade. Now is the time for policymakers to lower the barriers to new construction and thoughtfully reform and reduce the role played by the GSEs in housing finance. Policy solutions are necessarily complex, nuanced, and will take time. Destabilizing tariffs, a crackdown on immigration, selling the GSEs and firing vast swathes of the federal government tasked with housing risk turning a housing crisis into a financial crisis.