Insight

March 4, 2026

Trump Accounts Are Here: What to Know

Executive Summary

- The One Big Beautiful Bill Act created a new custodial-style individual retirement account for minors known as “Trump Accounts,” adding to the growing list of tax-advantaged savings vehicles to encourage savings for a child’s future.

- The legislation permits annual contributions up to $5,000 from multiple sources – each with distinct tax treatments – and provides a one-time $1,000 federal seed contribution for certain children born between 2025–2028.

- While well-intentioned, Trump Accounts simply add to the web of special-purpose accounts that not only add enormous complexity and costs to the tax code, but make it more challenging for individuals to optimize savings decisions; policymakers could instead look to simplify the tax code by consolidating the existing menu of savings vehicles via universal savings accounts.

Introduction

The One Big Beautiful Bill (OBBB) Act created a new custodial-style individual retirement account for minors known as “Trump Accounts,” adding to the growing list of tax-advantaged savings vehicles to encourage savings for a child’s future.

The OBBB permits annual contributions of up to $5,000 from multiple sources including family members, friends, employers, charitable organizations, and state governments, with varying tax treatments depending on the sources of funds. In addition, the federal government will also make a one-time $1,000 seed contribution for certain children born between 2025–2028.

While well-intentioned, Trump Accounts simply add to the web of special-purpose accounts that not only add enormous complexity and costs to the tax code*, but make it more challenging for individuals to optimize savings decisions. Policymakers could instead look to simplify the tax code by consolidating the existing menu of savings vehicles via universal savings accounts.

*This assessment of the tax treatment was made using the best information available at the time of publication. Notably, however, there are ongoing differences of interpretation with respect to the full tax implications of Trump Accounts. Expect Treasury to clarify tax treatment questions.

Trump Accounts

What are they?

A Trump Account is a custodial-style individual retirement account where the child owns the assets while an adult – typically a parent or guardian – acts on the child’s behalf until the beneficiary reaches age 18. Children under 18 with a Social Security number are eligible to open a Trump Account. Moreover, U.S. citizens born between January 1, 2025, and December 31, 2028, will receive a one-time $1,000 seed contribution under the U.S. Treasury’s pilot program. Those under 18 born outside of those dates are still eligible to open an account but will not receive the seed investment. Annual contributions of up to $5,000 may be made to these accounts, and this limit is indexed for inflation. There are exceptions to this contribution cap, however, including the government seed funds and contributions made from charities.

Qualified individuals can file Internal Revenue Service Form 4547 with a 2025 tax return or via an online portal to open the account. While registration is open, accounts will not be launched or accept contributions until July 2026.

Why were they created?

U.S. Treasury Secretary Scott Bessent described the Trump Accounts as “among the most significant policy innovations of modern times,” and a “merger of Wall Street and Main Street.” Secretary Bessent explained that the Trump Accounts expanded upon “baby bonds,” which were created to narrow the growing wealth gap – but are limited to investing in U.S. government bonds. Trump Accounts, however, allow for investing in equity markets, potentially generating greater returns.

How is the money invested?

The OBBB mandates that Trump Account funds be invested in low-cost mutual funds, or exchange-traded funds that track the returns of a qualified index and does not use leverage. A qualified index includes that Standard and Poor’s 500 stock market index, or any other index that is comprised of equity investments in primarily U.S. companies. The law also stipulates that these funds cannot have annual fees and expenses of more than 0.1 percent of the balance of the investment fund.

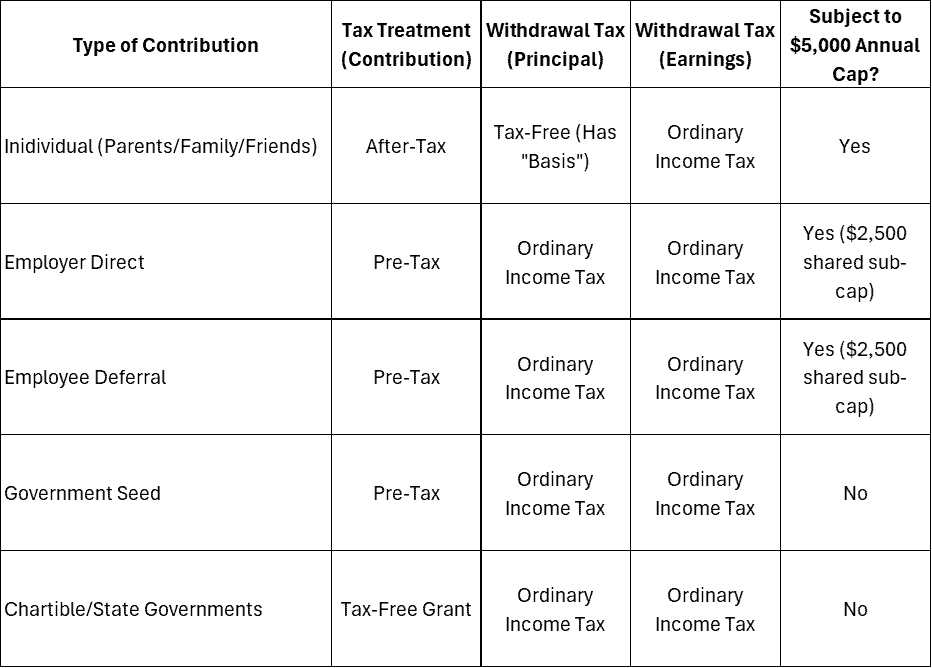

Who can contribute? How is it taxed?

The tax rules governing Trump Accounts are complex. The rules change based on from whom and how contributions are made.

Contributions from individuals – parents, guardians, and family – are made on an after-tax basis. This means that upon withdrawal, only the earnings are subject to income tax.

Trump Accounts also permit employer contributions and employee deferrals. An employer may contribute up to $2,500 per year, per employee. In other words, if an employee has multiple children, the employer contribution can be split across multiple Trump Accounts. These contributions are excluded from the employee’s income and are made on a pre-tax basis. Employer contributions are subject to the annual $5,000 limit. When funds are withdrawn, the full value of the contribution and earnings will be taxed. An employee – which could be a parent, guardian, or other family member – directing a portion of their salary to a Trump Account also does this on a pre-tax basis, making contributions and gains taxable upon withdrawal. Deferring a portion of salary to these accounts is dependent upon the employer offering a Trump Account contribution program. The combined employer-employee contribution has a sub-cap of $2,500 per employee.

The federal government’s one-time $1,000 seed contribution is excluded from the annual $5,000 limit and will be taxed upon withdrawal. States, local governments, and 501(c)(3) charities can also contribute. Similarly, these contributions do not count toward annual limits and are taxable when they are withdrawn. There has already been uptake from philanthropists, including a multi-billion-dollar https://www.cnbc.com/2025/12/17/ray-dalio-trump-child-savings-accounts.htmlpledge from Dell Technologies founder Michael Delland Bridgewater Associates founder Ray Dalio.

Each source of contribution has a different tax treatment when the funds are withdrawn. The tax complexity will require maintaining accurate records of the source of funds and associated cost basis that is likely to create significant compliance costs. Table 1 summarizes the tax treatment of contributions going in, withdrawals of principal and earnings, and whether the contribution is subject to the annual $5,000 cap.

Table 1. Tax Treatments of Trump Accounts

Withdrawals

Money generally cannot be withdrawn until the child turns 18. After 18, the account functions like a traditional Individual Retirement Account, meaning withdrawals are taxed at ordinary income. The funds are subject to a 10-percent penalty if withdrawn before the age of 59 ½, however, unless the withdrawn funds’ use meets an exception including, but not limited to, education expenses, first-time home purchases, or starting a business.

Existing Accounts

A Trump Account is seemingly a compliment to other accounts that are designed to save for a child’s future. Existing accounts include 529 plans (for education and administered by states), custodial Roth and traditional Individual Retirement Accounts (unlike the Trump Accounts, these require earned income to contribute), Uniform Gifts to Minors Act, Uniform Transfers to Minors Act, and brokerage accounts. This list continues to expand when children become working adults and gain access to employer-sponsored plans, including traditional and Roth 401(k)s, health spending accounts, and flex savings accounts.

Each of these accounts has its own qualifications, tax treatments, and income requirements (and, sometimes, limits).

Universal Savings Accounts

The existing tax code governing the various types of savings accounts is a complex labyrinth of rules, exemptions to those rules, and income requirements and limits.

Rather than adding another account and, therefore, increasing tax complexity, Congress could pivot to reduce the burden.

Senator Ted Cruz (R-TX) and Representative Diana Harshbarger (R-TN) have introduced the Universal Savings Account Act, a bill that would allow Americans to “save without the restrictions and penalties associated with traditional tax advantaged accounts.” The bill allows for an initial contribution limit of $10,000, which increases by $500 every year until it reaches the $25,000 cap. This plan is structured like a Roth Individual Retirement Account where the contributions are made with after-tax dollars, and the distributions will be tax free. Additionally, this proposed account has no contribution limits based on income or limiting factors for when funds can be withdrawn or how they are used.

A traditional Individual Retirement Account-style universal savings account, where contributions are made on a pre-tax basis and all the distributions are subject to income tax, is also a possibility.

Both the Roth and traditional type of universal savings account would undoubtedly provide relief to Americans attempting to navigate an increasingly complex tax system.

Conclusion

The One Big Beautiful Bill Act added Trump Accounts, a new custodial-style individual retirement account for minors to a growing list of vehicles to encourage saving for a child’s future. While well-intentioned, the Trump Accounts add to the tax complexity and likely increased compliance burden for families. A simpler universal savings account could achieve similar pro-savings goals while reducing complexity.